PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066468

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066468

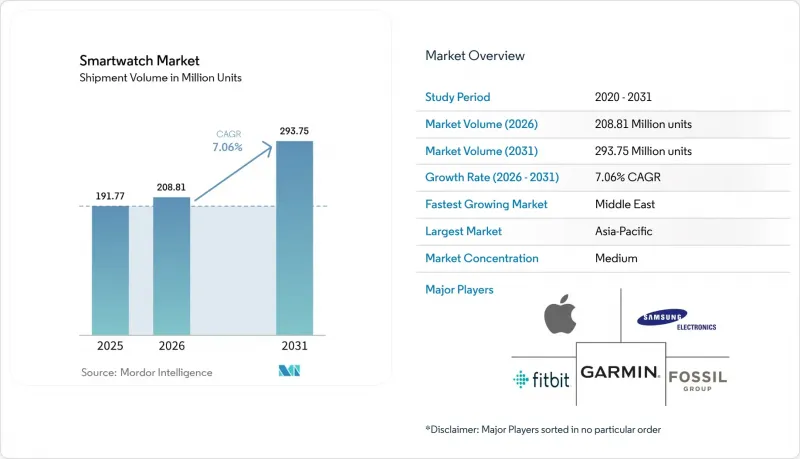

Smartwatch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the smartwatch market size in terms of shipment volume is projected to be 191.77 Million units in 2025, 277.49 Million units in 2026, and reach 293.75 Million units by 2031, registering a CAGR of 7.06% between 2026 to 2031.

This report is Segmented by Operating System (watchOS, Wear OS, Harmonyos, and More), Display Technology (AMOLED, Micro-LED, and TFT-LCD), Connectivity (Bluetooth-Only, Cellular 4G and LTE, and 5G-Enabled), Application (Fitness and Wellness, Medical and Chronic-Care, and More), and Geography (North America, South America, Europe, Asia Pacific, and More). The Market Forecasts are Provided in Terms of Volume (Units).

Global Smartwatch Market Trends and Insights

Rapid Feature-Rich Upgrades by Leading OEMs

Apple secured De Novo clearance for sleep-apnea screening on the Watch Series 10 in September 2024, followed by Samsung's clearance for the Galaxy Watch 7 within six months, reinforcing an upgrade cadence that keeps premium buyers on a two-year replacement cycle. Garmin and Huawei then broadened the spec race with dual-frequency GPS and +-2 bpm heart-rate precision, signaling that regulated health features now drive brand differentiation. Achieving medical-grade status adds engineering and compliance overhead that only companies with integrated silicon, algorithm, and legal teams can absorb, effectively raising entry barriers. The result is a smartwatch market in which top-tier OEMs maintain gross margins of 40% while budget brands rely on volume at razor-thin spreads. Continuous feature rollouts, therefore, lift overall ASPs even as shipments climb.

Convergence of Health Monitoring with Telemedicine Platforms

Garmin's October 2024 integration with Medixine enabled hospital clinicians in 200 European centers to stream continuous heart rate and oxygen saturation data directly into electronic medical records. Samsung opened its Health SDK in July 2024, securing partnerships with Teladoc and Amwell within four months. Masimo's sensor licensing now enables Wear OS OEMs to pursue 510(k) clearance without building pulse-oximetry IP from scratch. This deep health-cloud connectivity became commercially viable once the U.S. Centers for Medicare and Medicaid Services began reimbursing remote physiologic monitoring that relies on smartwatch data in January 2025. Platforms capable of HIPAA compliance, ISO 13485 audits, and multi-jurisdictional data residency requirements now convert raw sensor streams into billable services, driving attach-rate-driven revenue that exceeds hardware margins.

Data-Privacy Regulations Tightening Health-Data Flows

The European Union's GDPR treats heart-rate and sleep data as special-category information, requiring granular opt-in and human oversight for automated decisions. A forthcoming ePrivacy Regulation will introduce consent layers by data type in 2027, likely delaying feature rollouts until country-level approvals are obtained. China's Personal Information Protection Law bars cross-border transfers without adequacy assessments, complicating global cloud architectures for smartwatch vendors. California's CPRA prohibits insurers from adjusting premiums with biometric data unless members re-consent annually. Maintaining parallel compliance stacks raises costs and fragments user experiences, acting as a headwind on smartwatch market penetration in highly regulated regions.

Other drivers and restraints analyzed in the detailed report include:

- Growing Corporate Wellness and Insurance-Linked Incentive Programs

- Rising Smartwatch Adoption in Emerging Middle-Income Asia Pacific Cities

- Battery-Life Limitations Due to Continuous Sensing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The watchOS retained 29.12% smartwatch market share in 2025 thanks to Apple's vertically integrated hardware, software, and services stack that converts each device into a recurring Fitness+ subscription. HarmonyOS, however, is growing at a 8.01% CAGR as Huawei bundles smartwatches priced between CNY 800 (USD 110) and CNY 2,500 (USD 345) across China's 800 million-user smartphone base.

Wear OS remains fragmented across Snapdragon, Exynos, and MediaTek silicon, resulting in inconsistent battery life that hinders uptake, even after Fitbit's sensor IP infusion. Proprietary real-time operating systems from Garmin and Polar trade app stores for 14-day endurance, satisfying endurance athletes who value GPS precision over ecosystems. The FDA's March 2024 guidance now classifies algorithmic health upgrades as new medical device submissions, a rule that favors platforms capable of aligning software and hardware release cycles. In China, streamlined provincial approvals enable HarmonyOS to deploy Class II features more quickly than its foreign rivals, thereby maintaining its price-performance edge.

AMOLED commanded 68.46% of 2025 shipments as Samsung Display and BOE drove panel costs below USD 12, enabling always-on screens in watches priced under USD 150. The smartwatch market size for AMOLED models continues to widen even though supply chain bottlenecks can extend lead times to 12 weeks during flagship phone launches.

Micro-LED is projected to grow at a 9.21% CAGR through 2031, following PlayNitride's achievement of 99.99% mass-transfer yields, which have pushed production costs below USD 15 per square inch. Apple's prototype Watch Ultra with Micro-LED boasts 2,000-nit brightness and 30% lower power draw, enticing pilots and sailors who need daylight visibility. TFT-LCD now clings to sub-USD 50 kids' watches because price parity has eliminated its edge. Yet supply concentration in two Korean OLED giants elevates risk, forcing brands like Garmin to downgrade resolutions when allocations tighten.

Geography Analysis

The Asia Pacific region accounted for 39.36% of 2025 shipments, with China delivering 45.8 million units in the first nine months of 2024, as vendor subsidies and livestream commerce drove demand from lower-tier cities. India experienced a 30% contraction when ASPs declined, although the premium band above INR 20,000 still doubled, underscoring a two-speed market. Japan and South Korea are leveraging aging-society health budgets for elder-care pilots that involve placing smartwatches on at-risk seniors, channeling unit growth despite high smartphone saturation.

The Middle East is expected to record the fastest growth rate of 10.57% through 2031, as the United Arab Emirates links Dubai's 10X Health program to step-count incentives and Saudi Arabia dedicates SAR 2 billion to digital health hardware. Offline retail dominates sales, favoring vendors with mall kiosks that offer Arabic-language demos and instant warranty service. Turkey's 55% import surge illustrates pent-up demand once installment plans spread payments across 6-12 months.

North America's installed base surpassed 100 million units by mid-2025, meaning growth now depends on induced replacement cycles. WatchOS 11 dropped support for Series 4 and older, nudging five-year users to upgrade. Canada expands insurance coverage for glucose sensors that pair with smartwatches, enlarging the clinical addressable base. Europe's GDPR slows feature parity, evidenced by a six-month delay for Samsung's sleep-apnea detection rollout while legal agreements were finalized. Mexico's 21% growth rides e-commerce financing, though counterfeit imports account for up to 20% of units and erode brand trust.

- Apple Inc.

- Samsung Electronics Co. Ltd

- Garmin Ltd

- Fitbit (Google LLC)

- Fossil Group Inc.

- Huawei Technologies Co. Ltd

- Sony Corporation

- Xiaomi Corp.

- Oppo (Guangdong Oppo Mobile Telecommunications)

- Amazfit / Zepp Health Corp.

- Lenovo Group Ltd

- Mobvoi Inc.

- Polar Electro Oy

- Suunto Oy

- Withings SA

- Zepp Health Corp.

- Citizen Watch Co. Ltd

- Mobvoi Inc.

- Casio Computer Co. Ltd

- Noise (Imagine Marketing Pvt Ltd)

- Realme TechLife (Realme)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Feature-Rich Upgrades by Leading OEMs

- 4.2.2 Convergence of Health Monitoring with Telemedicine Platforms

- 4.2.3 Growing Corporate Wellness and Insurance-Linked Incentive Programs

- 4.2.4 Rising Smartwatch Adoption in Emerging Middle-Income Asia Pacific Cities

- 4.2.5 Low-Power AI Chips Enabling On-Device Analytics

- 4.2.6 Government-Funded Remote Elder Care Pilots

- 4.3 Market Restraints

- 4.3.1 Data-Privacy Regulations Tightening Health-Data Flows

- 4.3.2 Battery-Life Limitations Due to Continuous Sensing

- 4.3.3 Supply-Chain Fragility for Advanced OLED Panels

- 4.3.4 Plateauing Differentiation in Mid-Tier Price Band

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Operating System

- 5.1.1 WatchOS

- 5.1.2 Wear OS

- 5.1.3 HarmonyOS

- 5.1.4 Proprietary / RTOS

- 5.2 By Display Technology

- 5.2.1 AMOLED

- 5.2.2 Micro-LED

- 5.2.3 TFT-LCD

- 5.3 By Connectivity

- 5.3.1 Bluetooth-only

- 5.3.2 Cellular (4G/LTE)

- 5.3.3 5G-enabled

- 5.4 By Application

- 5.4.1 Fitness and Wellness

- 5.4.2 Medical and Chronic-care

- 5.4.3 Personal Assistance and Payments

- 5.4.4 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 New Zealand

- 5.5.4.7 Rest of Asia Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Partnerships

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Apple Inc.

- 6.4.2 Samsung Electronics Co. Ltd

- 6.4.3 Garmin Ltd

- 6.4.4 Fitbit (Google LLC)

- 6.4.5 Fossil Group Inc.

- 6.4.6 Huawei Technologies Co. Ltd

- 6.4.7 Sony Corporation

- 6.4.8 Xiaomi Corp.

- 6.4.9 Oppo (Guangdong Oppo Mobile Telecommunications)

- 6.4.10 Amazfit / Zepp Health Corp.

- 6.4.11 Lenovo Group Ltd

- 6.4.12 Mobvoi Inc.

- 6.4.13 Polar Electro Oy

- 6.4.14 Suunto Oy

- 6.4.15 Withings SA

- 6.4.16 Zepp Health Corp.

- 6.4.17 Citizen Watch Co. Ltd

- 6.4.18 Mobvoi Inc.

- 6.4.19 Casio Computer Co. Ltd

- 6.4.20 Noise (Imagine Marketing Pvt Ltd)

- 6.4.21 Realme TechLife (Realme)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment