PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066657

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066657

Spain Road Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

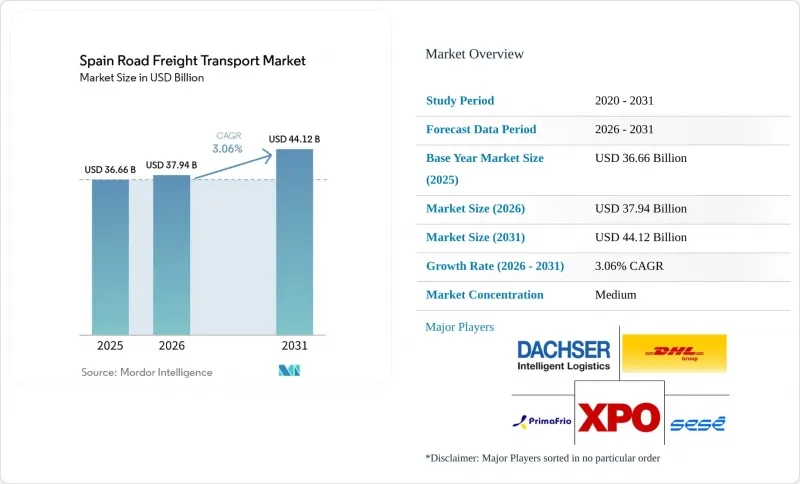

According to Mordor Intelligence, the spain road freight transport market size was valued at USD 36.66 billion in 2025 and is projected to reach USD 37.94 billion in 2026 to USD 44.12 billion by 2031, at a 3.06% CAGR during the forecast period (2026-2031).

High domestic modal share above 95%, annual road-borne freight volumes near 1.5 billion Tons, and the country's dual role as Mediterranean production hub and Atlantic gateway continue to anchor the Spain road freight transport market. This report is Segmented by End User Industry (Agriculture, and More), by Destination (Domestic, and More), by Truckload Specification (FTL, and More), by Containerization (Containerized, and More), by Distance (Long Haul, and More), by Goods Configuration (Fluid Goods, and More), by Temperature Control (Temperature Controlled, and More). The Market Forecasts are Provided in Terms of Value (USD).

Spain Road Freight Transport Market Trends and Insights

Cold-Chain Boom from Vaccine and Premium Food Exports

Pharmaceutical exports worth EUR 18.4 billion (USD 21.64 billion) in 2024 required 2-8 °C integrity, expanding premium-rate demand for GDP-compliant carriers equipped with real-time monitoring. Simultaneously, EUR 62 billion (USD 72.93 billion) in high-value food exports such as organic citrus and Iberian pork hinge on unbroken refrigeration, generating year-round utilization that mitigates seasonality. Specialized fleets adopt blockchain-enabled traceability and insulated swap bodies to capture margin uplift. Veterinary border inspections under EU 2017/625 add transit dwell but reinforce the value of compliance-certified providers. Operators like Primafrio leverage proprietary telematics to win contracts from pharmaceutical manufacturers that shun general freight networks.

Digital Freight Marketplaces Streamline Backhauls

Platform adoption lowered empty running from 28% in 2020 to 22% in 2024, saving EUR 180 million (USD 211.73 million) in fuel and improving carrier asset utilization by 12-18%. Real-time capacity visibility enables partial-load booking within two-hour windows and demand forecasting 24-48 hours ahead. Smaller fleets gain direct access to shipper volumes, but broker margins compress as transparency rises. Integration of customs, ADR, and driver credentials into booking workflows cuts paperwork friction, accelerating cross-border uptake. Youthful logistics managers favor app-based procurement, pushing digital transactions up 35% year-over-year in 2024.

EU Mobility Package Cabotage and Rest-Time Compliance Burden

The 2024 rules cap non-resident carriers at three cabotage trips in seven days and enforce four-day cooling-off periods, lifting operator costs 8-12%. Mandatory home return every four weeks reduces productive driving by 15-20% on Northern Europe runs, compelling relay systems or extra drivers. Smart tachographs enable remote enforcement, removing gray zones. Wage alignment with host countries inflates Spanish carrier labor cost up to 30% in France or Germany. Fleets deploy driver-swap hubs near borders to protect truck utilization, but handovers introduce scheduling risk.

Other drivers and restraints analyzed in the detailed report include:

- Low-Emission Fleet Incentives and Scrappage Schemes

- Iberian Land-Bridge Demand Post-Brexit Rerouting

- Rail-Freight Subsidy Shift Under Mercancias 30 Program

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing contributed 37.51% of Spain road freight transport market share in 2025, underpinned by 2.45 million vehicle outputs and robust pharmaceutical exports. Consistent component flows between Catalonia, Aragon, and Basque plants and ports sustain high-volume lanes. Wholesale and retail trade, scaling at a 3.52% CAGR, mirrors omnichannel fulfillment patterns that depend on frequent multi-stop rounds, stimulating less-than-truck-load uptake. Construction freight rides EUR 70 billion (USD 82.34 billion) EU-funded projects through 2026 before tapering. Agriculture's seasonal peaks in citrus and vegetable exports intensify refrigerated capacity requirements.

Evolving models blur boundaries as manufacturers adopt direct-to-consumer strategies needing retail-style distribution, while large retailers move into light assembly. This hybridization compels carriers to offer flexible service menus. The Spain road freight transport market for manufacturing and retail combined is projected to widen further as nearshoring trends spark incremental component shipments. Diverse sectoral demand smooths volume volatility and underpins steady fleet utilization.

Domestic shipments dominated with 64.07% of the Spain road freight transport market size in 2025 backed by the nation's 47 million consumers and inter-regional specializations. High-density corridors connect Catalonia's factories, Andalusia's farms, and Madrid's consumption hub, supporting predictable backhauls. Urban low-emission zones force adaptation in Madrid and Barcelona, catalyzing electric urban fleets.

International freight expands faster at 3.60% CAGR as Iberian land-bridge routes grow and Morocco traffic via Operation Marhaba sets new records. The EU Mobility Package complicates compliance but levels the playing field against low-wage competitors. Pending Gibraltar Strait tunnel studies hint at transformative future links to North Africa, yet impacts remain post-2035.

Full-truck-load maintained 83.07% market share owing to large batch exports of autos, produce, and construction material. Dedicated routes optimize driver hours and reduce handling damage. Savings accrue from consistent round-trip planning anchored by production calendars.

Less-than-truck-load's 3.43% CAGR traces back to e-commerce parcelization and the Spain road freight transport industry pivot to hub-and-spoke. Digital marketplaces raise load factors toward 90%, closing the historical efficiency gap. Operators invest in automated cross-docks near Madrid and Valencia to speed nightly sort cycles.

List of Companies Covered in this Report:

- A.P. Moller-Maersk

- DACHSER

- Almar Iberia Logistics

- Alonso Group (Transportes Alonso Salcedo)

- CMA CGM Group (CEVA Logistics)

- DHL Group

- DSV A/S

- FM Logistic

- Girteka

- Grupo Sese

- International Distributions Services (GLS)

- JSV Logistics

- La Poste Group (Seur Geopost)

- Marcotran

- Primafrio

- Rhenus Group

- Rohlig Logistics

- Transfesa Logistics

- Trucksters

- XPO, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 GDP Distribution by Economic Activity

- 4.3 GDP Growth by Economic Activity

- 4.4 Economic Performance and Profile

- 4.4.1 Trends in E-Commerce Industry

- 4.4.2 Trends in Manufacturing Industry

- 4.5 Transport and Storage Sector GDP

- 4.6 Logistics Performance

- 4.7 Length of Roads

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Pricing Trends

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Road Freight Tonnage Trends

- 4.15 Road Freight Pricing Trends

- 4.16 Modal Share

- 4.17 Inflation

- 4.18 Regulatory Framework

- 4.19 Value Chain and Distribution Channel Analysis

- 4.20 Market Drivers

- 4.20.1 Cold-Chain Boom from Vaccine and Premium Food Exports

- 4.20.2 Digital Freight Marketplaces Streamline Backhauls

- 4.20.3 Low-Emission Fleet Incentives and Scrappage Schemes

- 4.20.4 Iberian Land-Bridge Demand Post-Brexit Rerouting

- 4.20.5 Wind-Farm Component Super-Load Projects

- 4.20.6 32-m Mega-Truck Regulations Enhance Corridor Capacity

- 4.21 Market Restraints

- 4.21.1 EU Mobility Package Cabotage and Rest-Time Compliance Burden

- 4.21.2 Rail-Freight Subsidy Shift under Mercancias 30 Program

- 4.21.3 Flood-Related Insurance Premium Escalation on Mediterranean Routes

- 4.21.4 Container-Port Automation Delays Causing Landside Congestion

- 4.22 Technology Innovations in the Market

- 4.23 Porter's Five Forces Analysis

- 4.23.1 Threat of New Entrants

- 4.23.2 Bargaining Power of Buyers

- 4.23.3 Bargaining Power of Suppliers

- 4.23.4 Threat of Substitutes

- 4.23.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 By Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 By Truckload Specification

- 5.3.1 Full-Truck-Load (FTL)

- 5.3.2 Less than-Truck-Load (LTL)

- 5.4 By Containerization

- 5.4.1 Containerized

- 5.4.2 Non-Containerized

- 5.5 By Distance

- 5.5.1 Long Haul

- 5.5.2 Short Haul

- 5.6 By Goods Configuration

- 5.6.1 Fluid Goods

- 5.6.2 Solid Goods

- 5.7 By Temperature Control

- 5.7.1 Non-Temperature Controlled

- 5.7.2 Temperature Controlled

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 A.P. Moller-Maersk

- 6.4.2 DACHSER

- 6.4.3 Almar Iberia Logistics

- 6.4.4 Alonso Group (Transportes Alonso Salcedo)

- 6.4.5 CMA CGM Group (CEVA Logistics)

- 6.4.6 DHL Group

- 6.4.7 DSV A/S

- 6.4.8 FM Logistic

- 6.4.9 Girteka

- 6.4.10 Grupo Sese

- 6.4.11 International Distributions Services (GLS)

- 6.4.12 JSV Logistics

- 6.4.13 La Poste Group (Seur Geopost)

- 6.4.14 Marcotran

- 6.4.15 Primafrio

- 6.4.16 Rhenus Group

- 6.4.17 Rohlig Logistics

- 6.4.18 Transfesa Logistics

- 6.4.19 Trucksters

- 6.4.20 XPO, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment