PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066659

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066659

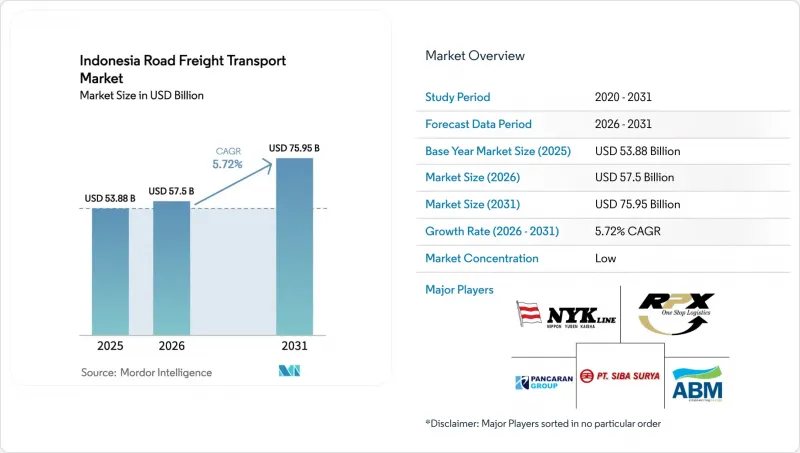

Indonesia Road Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the indonesia road freight transport market is expected to increase from USD 53.88 billion in 2025 to USD 57.50 billion in 2026 and reach USD 75.95 billion by 2031, growing at a CAGR of 5.72% over 2026-2031.

Rising adoption of the National Logistics Ecosystem (NLE) compresses door-to-port cycle times, while Euro-4 diesel standards improve fleet reliability, pushing carriers to modernize equipment. This report is Segmented by End-User (Agriculture, and More), by Destination (Domestic, International), by Truckload (FTL, LTL), by Containerization (Containerized, Non-Containerized), by Distance (Long Haul, Short Haul), by Good Configuration (Fluid, Solid), and by Temperature (Non-Temperature Controlled, Temperature Controlled). The Market Forecasts are Provided in Terms of Value (USD).

Indonesia Road Freight Transport Market Trends and Insights

National Logistics Ecosystem E-clearance Accelerating Door-to-Port Cycle Times

NLE integrates customs, port operators, and freight forwarders on one digital platform, shrinking documentation processing from three to five days to under 24 hours. Road carriers that previously absorbed idle-time costs now experience faster gate release, improving truck utilization and shortening order-to-cash cycles. Early adopters have reported 18-22% shorter door-to-port intervals. The platform's alignment with the ASEAN Customs Transit System improves predictability for cross-border trips and supports just-in-time manufacturing. Ongoing rollout to secondary ports will extend these gains beyond Java, fostering broader Indonesia road freight transport market growth.

Pharmaceutical Cold-chain Surge from Domestic Vaccine & Biologics Production

Bio Farma's annual output already exceeds 1 billion vaccine doses, and capacity is expected to rise to 1.5 billion by 2026 end. These volumes require Good Distribution Practice-compliant transport holding 2-8 °C and real-time monitoring. Kalbe Farma and Indofarma have added biologics lines, doubling demand for refrigerated trailers and data-logger systems. Strict BPOM oversight increases barriers for informal operators, favoring established fleets with validated processes. The cold-chain segment therefore outpaces the overall Indonesia road freight transport market.

Sharp Rise in Cargo-Theft Insurance Premiums Along Java-Sumatra Corridors

Insurance costs for high-value cargoes have surged 15-20% after an 18-22% uptick in theft incidents. Smaller carriers endure margin compression or shift risk onto shippers, reducing competitiveness. Added expenses for GPS devices, seals, and convoy escorts raise operating costs by another 3-5%. Law-enforcement coordination gaps across provinces enable organized crime to exploit rest-area vulnerabilities, encouraging shippers to mandate advanced security when tendering loads. Market consolidation thus accelerates in the Indonesia road freight transport market.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Euro-4 Diesel Transition Improving Fleet Reliability and Resale Values

- B40 Biodiesel Mandate Stabilizing Diesel Supply Costs for Long-Haul Carriers

- Persistent Port Gate-Out Congestion Post-Privatization Extending Dwell Times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wholesale and retail trade accounted for 34.24% of the Indonesia road freight transport market size in 2025, reflecting dense consumer demand across Java's tier-1 and tier-2 cities. This segment also exhibits the fastest 6.58% CAGR as convenience stores expand and pharmacy chains roll out health-and-wellness lines. Network designs now co-load consumer goods with biologics, intensifying route frequency and boosting vehicle utilization. Manufacturing sustains a steady baseline via automotive hubs in Karawang and electronics clusters in Batam, though exposure to global re-shoring remains a watch point.

Oil and gas, mining, and quarrying benefit from Sulawesi's nickel upswing and Kalimantan's coal exports, calling for specialized heavy-haul equipment. Construction freight aligns with ongoing National Strategic Projects, moving cement and steel on predictably scheduled runs. Agriculture and aquaculture adopt refrigerated logistics to capture export premiums for shrimp and mangosteen, while emerging verticals such as data-center construction generate episodic project loads. The overlapping flows collectively support diversified growth in the Indonesia road freight transport market.

Domestic moves still dominate with a 62.88% share in 2025 as shippers service 6,000 inhabited islands via road-ferry combinations. Toll-road build-out on Java and Sumatra cuts travel times by up to 20%, raising service reliability and underpinning inventory reduction strategies.

However, international volumes into Malaysia, Singapore, and Thailand are expanding faster at a 6.65% CAGR, assisted by NLE-to-ASEAN system interoperability that slashes border waits by roughly 50%. Sea Tollway sailings create predictable intermodal nodes, enhancing domestic route planning, whereas bonded logistics centers near Batam and Medan anchor international consolidation. The Kuala Lumpur-Singapore-Jakarta corridor now supports just-in-sequence deliveries for electronics and pharma, narrowing cost-of-service gaps with ocean freight. These complementary flows anchor resilient expansion for the Indonesia road freight transport market.

Full-truck-load retained 80.19% of Indonesia road freight transport market in 2025, driven by bulk palm oil, coal, and nickel ore consignments that naturally fill trailers. ODOL compliance pushes fleets toward multi-axle modular rigs that lift legal payload by up to 30%, enhancing FTL cost competitiveness.

Less-than-truck-load, meanwhile, grows at a brisk 6.41% CAGR as platforms such as Kargo Technologies and Deliveree aggregate SME volumes into optimized multi-drop routes. Algorithmic dispatch and dynamic pricing improve vehicle load factors, lowering per-unit freight for smaller shippers. Established FTL fleets respond by launching hybrid offerings that back-fill empty legs with on-demand LTL loads, blurring category lines. This dual evolution supports healthy diversification within the Indonesia road freight transport market.

List of Companies Covered in this Report:

- Bali Pro Cargo

- CJ Logistics Corporation

- DHL Group

- DSV

- Geodis

- JNE Express

- Ninja Express

- NYK Line

- NYK Line (Yusen Logistics Malaysia)

- Pancaran Group

- PT ABM Investama Tbk (PT Cipta Krida Bahari)

- PT Citrabati Logistik International

- PT Prima International Cargo

- PT Repex Wahana (RPX)

- PT Samudera Indonesia Tangguh

- PT Siba Surya

- PT.DMS Logistics Indonesia

- Rhenus Group

- Seacon Logistics

- Total Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 GDP Distribution by Economic Activity

- 4.3 GDP Growth by Economic Activity

- 4.4 Economic Performance and Profile

- 4.4.1 Trends in E-Commerce Industry

- 4.4.2 Trends in Manufacturing Industry

- 4.5 Transport and Storage Sector GDP

- 4.6 Logistics Performance

- 4.7 Length of Roads

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Pricing Trends

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Road Freight Tonnage Trends

- 4.15 Road Freight Pricing Trends

- 4.16 Modal Share

- 4.17 Inflation

- 4.18 Regulatory Framework

- 4.19 Value Chain and Distribution Channel Analysis

- 4.20 Market Drivers

- 4.20.1 National Logistics Ecosystem (NLE) e-clearance accelerating door-to-port cycle times

- 4.20.2 Pharmaceutical cold-chain surge from domestic vaccine & biologics production

- 4.20.3 Mandatory Euro-4 diesel transition improving fleet reliability and resale values

- 4.20.4 B40 biodiesel mandate stabilising diesel supply costs for long-haul carriers

- 4.20.5 Sulawesi nickel-to-battery corridor creating heavy inbound raw-material flows

- 4.20.6 ODOL phase-out law spurring demand for higher-capacity modular trucksets

- 4.21 Market Restraints

- 4.21.1 Sharp rise in cargo-theft insurance premiums along Java-Sumatra corridors

- 4.21.2 Persistent port gate-out congestion post-privatisation extending dwell times

- 4.21.3 Fragmented non-Jasa-Marga toll billing systems inflating en-route cost variance

- 4.21.4 Sparse LNG refuelling network delaying alternative-fuel truck adoption

- 4.22 Technology Innovations in the Market

- 4.23 Porter's Five Forces Analysis

- 4.23.1 Threat of New Entrants

- 4.23.2 Bargaining Power of Buyers

- 4.23.3 Bargaining Power of Suppliers

- 4.23.4 Threat of Substitutes

- 4.23.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 Truckload Specification

- 5.3.1 Full-Truck-Load (FTL)

- 5.3.2 Less than-Truck-Load (LTL)

- 5.4 Containerization

- 5.4.1 Containerized

- 5.4.2 Non-Containerized

- 5.5 Distance

- 5.5.1 Long Haul

- 5.5.2 Short Haul

- 5.6 Goods Configuration

- 5.6.1 Fluid Goods

- 5.6.2 Solid Goods

- 5.7 Temperature Control

- 5.7.1 Non-Temperature Controlled

- 5.7.2 Temperature Controlled

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Bali Pro Cargo

- 6.4.2 CJ Logistics Corporation

- 6.4.3 DHL Group

- 6.4.4 DSV

- 6.4.5 Geodis

- 6.4.6 JNE Express

- 6.4.7 Ninja Express

- 6.4.8 NYK Line

- 6.4.9 NYK Line (Yusen Logistics Malaysia)

- 6.4.10 Pancaran Group

- 6.4.11 PT ABM Investama Tbk (PT Cipta Krida Bahari)

- 6.4.12 PT Citrabati Logistik International

- 6.4.13 PT Prima International Cargo

- 6.4.14 PT Repex Wahana (RPX)

- 6.4.15 PT Samudera Indonesia Tangguh

- 6.4.16 PT Siba Surya

- 6.4.17 PT.DMS Logistics Indonesia

- 6.4.18 Rhenus Group

- 6.4.19 Seacon Logistics

- 6.4.20 Total Logistics

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment