PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066658

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066658

United Kingdom Road Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

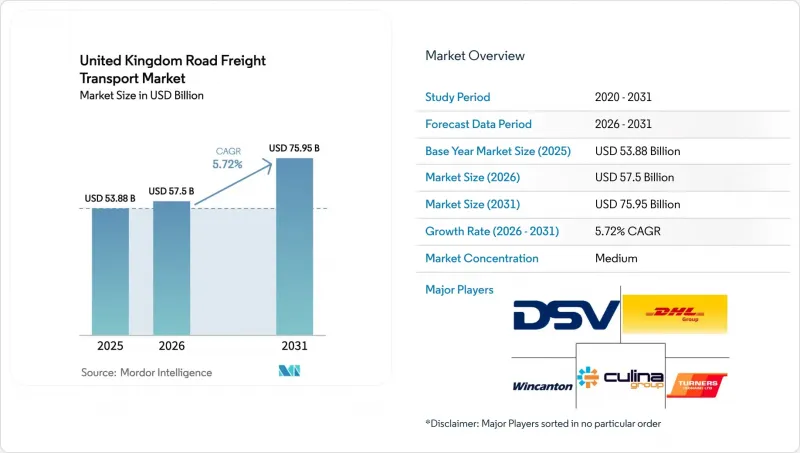

According to Mordor Intelligence, the united kingdom road freight transport market size is projected to be USD 53.88 billion in 2025, USD 57.5 billion in 2026, and reach USD 75.95 billion by 2031, growing at a CAGR of 5.72% from 2026 to 2031.

This report is Segmented by End-User (Agriculture, Fishing & Forestry, and More), by Destination (Domestic, International), by Truckload (FTL, LTL), by Containerization (Containerized, Non-Containerized), by Distance (Long Haul, Short Haul), by Goods (Fluid, Solid), by Temperature (Non-Temperature, Temperature Controlled). The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Road Freight Transport Market Trends and Insights

Digital Border & Customs Modernization Speeds Cross-Border Cycles

GVMS and BTOM consolidate declarations into a single digital file processed pre-arrival, allowing 87% of consignments to clear without inspection and cutting crossing times at Dover from 47 minutes to 28 minutes during 2024-2025. The link with the EU's ICS2 permits advance risk analysis that lowered rejection rates 34%. Temperature-controlled shippers benefit most, avoiding spoilage formerly caused by multi-hour queues. Faster borders also strengthen the United Kingdom road freight transport market by drawing volumes away from air freight on short European lanes. Operators report 6-8% asset-turn increases as tractors previously idling at ports re-enter revenue runs more quickly. Digital declarations further enable smaller haulers to offer international services, broadening competitive intensity inside the United Kingdom road freight transport market.

Infrastructure Mega-Projects Swell Construction Freight

HS2 Phase One alone consumes 18 million tons of aggregates and 1.2 million tons of steel through 2028, while the Lower Thames Crossing adds 3 million tons of deliveries through 2030. Government infrastructure budgets average USD 141 billion annually to 2027, ensuring multi-year contract visibility. These projects anchor predictable payloads that encourage fleet renewal into specialized walking-floor and low-loader trailers, raising capital efficiency. Long-haul segments of the United Kingdom road freight transport market capture the bulk of material flows as rail paths remain capacity-constrained. Construction volumes also cushion carriers against retail slowdowns, producing counter-cyclical revenue stability.

Shortage of Secure Overnight HGV Parking Meeting EU 561/2006 Rest Rules

Only 11,000 compliant spaces exist for 520,000 HGVs, forcing 68% of drivers into unlawful lay-bys where fines and operator-license sanctions loom. Hotspots on the M1, M6, and A1 experience 4:1 demand-supply gaps that add 8-12% detours for parking searches, trimming driver hours. Re-routing lowers fleet productivity, inflates fuel spend, and erodes service reliability inside the United Kingdom road freight transport market.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Pharma Biomanufacturing Clusters Drives Temperature-Controlled Demand

- 60-Tons Road-Train Pilot Boosts Trunk-Route Productivity

- Logistics-Real-Estate Scarcity Drives Warehouse Rents Above 12% CAGR.

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

By end user, manufacturing retained 40.65% of the United Kingdom road freight transport market share in 2025, while wholesale and retail trade is forecast to post the fastest 2.90% CAGR through 2031. Manufacturing remained the leading segment, supported by automotive production in the Midlands and the expansion of biopharma clusters, while wholesale and retail growth is being driven by omnichannel models that require more frequent, lower-volume shipments.

Temperature-controlled logistics for advanced therapies continue to support premium services and strengthen pharmaceutical demand. At the same time, infrastructure projects such as HS2 and the Lower Thames Crossing are boosting the movement of construction materials, while post-Brexit shifts toward domestic sourcing in agriculture and ongoing North Sea decommissioning sustain specialized freight demand. Emerging data center developments along the London-Dublin corridor are also creating opportunities for high-value, time-sensitive transport, encouraging fleets to expand service capabilities.

By destination, international movements delivered a 3.10% CAGR outlook, outperforming domestic freight despite holding only 34.43% of 2025 volumes after digital border reforms significantly reduced border delays. Domestic haulage continued to dominate the market, supported by dense population centers and the country's geographic structure, while improving border efficiency and Freeport incentives are encouraging more businesses to participate in cross-border trade.

Domestic operations are also benefiting from productivity gains on key motorway corridors, helping offset ongoing driver shortages. However, regulatory constraints such as cabotage limits and added compliance complexities in Northern Ireland are weighing on cross-Channel margins. In response, some shippers are increasingly adopting unaccompanied trailer solutions via ferry to improve flexibility and reduce scheduling risks.

By truckload, Full-truck-load services accounted for 83.36% of the United Kingdom road freight transport market size in 2025, while Less-than-truckload is forecast to post the fastest 2.93% CAGR through 2031. Full-truck-load activity continues to dominate, supported by large-scale retail replenishment, automotive just-in-sequence supply chains, and construction logistics, with higher payload efficiencies further strengthening its cost advantage on longer routes.

Less-than-truckload is expanding due to the rise in e-commerce returns and increasing shipment fragmentation driven by circular economy practices. The adoption of digital freight platforms is improving backhaul matching and reducing empty miles, helping narrow cost differences with full loads. However, while hybrid FTL-LTL fleet strategies offer better asset utilization, they require advanced planning capabilities that many mid-sized operators are still developing.

List of Companies Covered in this Report:

- A.P. Moller-Maersk

- Culina Group

- DACHSER

- DFDS

- DHL Group

- DSV A/S

- Girteka

- Gist Ltd

- Gregory Distribution Ltd

- GXO Logistics (Wincanton PLC)

- Howard Tenens

- Hoyer GmbH

- Kinaxia Logistics Ltd

- Marshalls Logistics

- Nordic Transport Group A/S

- Palletways

- Turners (Soham) Ltd

- United Parcel Service of America, Inc. (UPS)

- W H Malcolm Ltd

- XPO, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 GDP Distribution by Economic Activity

- 4.3 GDP Growth by Economic Activity

- 4.4 Economic Performance and Profile

- 4.4.1 Trends in E-Commerce Industry

- 4.4.2 Trends in Manufacturing Industry

- 4.5 Transport and Storage Sector GDP

- 4.6 Logistics Performance

- 4.7 Length of Roads

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Pricing Trends

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Road Freight Tonnage Trends

- 4.15 Road Freight Pricing Trends

- 4.16 Modal Share

- 4.17 Inflation

- 4.18 Regulatory Framework

- 4.19 Value Chain and Distribution Channel Analysis

- 4.20 Market Drivers

- 4.20.1 Digital border & customs modernisation (GVMS, BTOM) speeds cross-border cycles

- 4.20.2 Infrastructure mega-projects (HS2, Lower Thames Crossing) swell construction freight

- 4.20.3 Rise of pharma biomanufacturing clusters driving temperature-controlled demand

- 4.20.4 60-tons road-train pilot boosts trunk-route productivity

- 4.20.5 Corporate Scope-3 mandates shifting volumes to certified low-carbon carriers

- 4.20.6 Circular-economy & product-returns laws expanding reverse-logistics flows

- 4.21 Market Restraints

- 4.21.1 Shortage of secure overnight HGV parking meeting EU 561/2006 rest rules

- 4.21.2 Logistics-real-estate scarcity; warehouse rents >12 % CAGR in Golden Triangle

- 4.21.3 Post-Brexit cabotage limits & visa caps curbing peak-season capacity

- 4.21.4 Parts & tyre supply disruptions prolonging HGV downtime

- 4.22 Technology Innovations in the Market

- 4.23 Porter's Five Forces Analysis

- 4.23.1 Threat of New Entrants

- 4.23.2 Bargaining Power of Buyers

- 4.23.3 Bargaining Power of Suppliers

- 4.23.4 Threat of Substitutes

- 4.23.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 Truckload Specification

- 5.3.1 Full-Truck-Load (FTL)

- 5.3.2 Less than-Truck-Load (LTL)

- 5.4 Containerization

- 5.4.1 Containerized

- 5.4.2 Non-Containerized

- 5.5 Distance

- 5.5.1 Long Haul

- 5.5.2 Short Haul

- 5.6 Goods Configuration

- 5.6.1 Fluid Goods

- 5.6.2 Solid Goods

- 5.7 Temperature Control

- 5.7.1 Non-Temperature Controlled

- 5.7.2 Temperature Controlled

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 A.P. Moller-Maersk

- 6.4.2 Culina Group

- 6.4.3 DACHSER

- 6.4.4 DFDS

- 6.4.5 DHL Group

- 6.4.6 DSV A/S

- 6.4.7 Girteka

- 6.4.8 Gist Ltd

- 6.4.9 Gregory Distribution Ltd

- 6.4.10 GXO Logistics (Wincanton PLC)

- 6.4.11 Howard Tenens

- 6.4.12 Hoyer GmbH

- 6.4.13 Kinaxia Logistics Ltd

- 6.4.14 Marshalls Logistics

- 6.4.15 Nordic Transport Group A/S

- 6.4.16 Palletways

- 6.4.17 Turners (Soham) Ltd

- 6.4.18 United Parcel Service of America, Inc. (UPS)

- 6.4.19 W H Malcolm Ltd

- 6.4.20 XPO, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment