PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066660

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066660

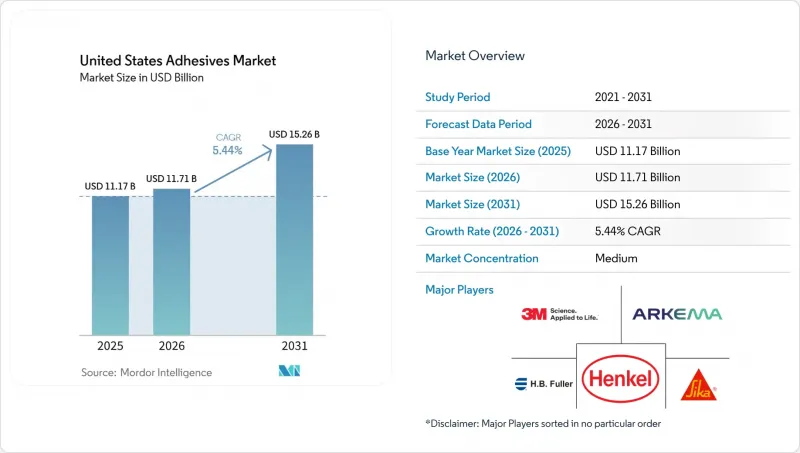

United States Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states adhesives market size is expected to increase from USD 11.17 billion in 2025 to USD 11.71 billion in 2026 and reach USD 15.26 billion by 2031, growing at a CAGR of 5.44% over 2026-2031.

This report is Segmented by Resin (Acrylic, Cyanoacrylate, Epoxy, Polyurethane, Silicone, VAE/EVA, and More), Technology (Hot-Melt, Reactive, Solvent-Borne, UV Cured, and Water-Borne), and End-User Industry (Aerospace, Automotive, Building and Construction, Footwear and Leather, Healthcare, Packaging, Woodworking and Joinery, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Adhesives Market Trends and Insights

Surge in Lightweighting Demand in Automotive Manufacturing

Automotive original equipment manufacturers (OEMs) now specify epoxy and polyurethane structural adhesives that can shave 10%-15% from body-in-white mass, translating directly into longer electric vehicle range and compliance with the latest Corporate Average Fuel Economy (CAFE) targets. General Motors' Ultium platform deploys thermally conductive epoxy lines below 0.3 Watts per meter-Kelvin (W/(m*K)) to curb cell-to-cell heat propagation, while maintaining electrical isolation over 3 kilovolts. The lengthy 18-24 month qualification window for new chemistries shields incumbents but opens niches for silicone specialists able to pair dielectric strength with electromagnetically dissipative additives that protect 800-volt architectures. Regional Tier-1 suppliers in Michigan and Ohio have already booked multi-year contracts for gap-filler silicones rated to 200°C, signaling a sustained pull through 2029.

Continued Growth in E-Commerce Boosting Packaging Adhesives

With e-commerce accounting for a significant share of United States retail sales, corrugators demand hot-melt and water-borne adhesives that cure fast without sacrificing green strength at speeds topping 300 meters per minute. Amazon's pledge to replace plastic air pillows with paper filler has driven uptake of starch- and vinyl-acetate-ethylene (VAE) emulsions compatible with mono-material recycling streams. These VAE systems command 20%-25% price premiums but ensure polyethylene reclaim purity. Meanwhile, carton producers are thinning board calipers to 180 g/m2, forcing rheology upgrades so adhesive lay-down remains consistent despite reduced substrate porosity. Logistics hubs in Texas and Pennsylvania report double-shift plant utilization to meet peak fulfillment seasons, underscoring the secular momentum behind packaging grades.

Petro-Feedstock Price Volatility

Early 2026 propylene prices dipped from mid-2024 peaks but remain highly sensitive to Gulf Coast cracker outages and geopolitical events . Contract structures seldom hedge quarterly swings, exposing converters to margin squeezes before downstream price adjustments can take effect. Although bio-attributed resins offer a diversification hedge, they import exposure to crop-price cycles and renewable-credit markets, offsetting some stability gains. Adhesive buyers, therefore, demand flexible-formulation clauses allowing filler substitutions, complicating inventory planning and formulation consistency.

Other drivers and restraints analyzed in the detailed report include:

- Rising U.S. Residential Construction and Housing Starts

- Adoption of Hybrid Bonding for Mass-Timber Construction

- Stringent VOC Emission Limits on Solvent-Borne Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylics retained 28.85% of 2025 revenue, but commoditization pressures margins, especially in pressure-sensitive tapes. Epoxies remain indispensable for aerospace primary structures, commanding premium prices for Tg values exceeding 180°C. Polyurethanes dominate flexible packaging and panel lamination, prized for impact resilience, whereas cyanoacrylates serve niche rapid-bonding roles in electronics and surgical closures. VAE/EVA copolymers supply cost-effective hot-melts in packaging, though limited heat resistance curtails automotive uptake. Specialty phenolic, polyimide, and anaerobic resins occupy small but lucrative segments demanding extreme chemical or thermal stability. Silicone grades are forecast to grow at a 6.45% CAGR from 2026 to 2031, on the back of high-temperature electric vehicle (EV) drivetrains and wearable-healthcare use cases. Battery-pack designers specify gap-filler silicones that withstand 150-200°C without embrittlement, delivering dielectric insulation above 3 kilovolts while dissipating heat. Medical device firms value silicone pressure-sensitives for 14-day glucose-monitor adhesion, ensuring International Organization for Standardization (ISO) 10993 biocompatibility.

List of Companies Covered in this Report:

- 3M

- Arkema

- Ashland Global Holdings

- Avery Dennison Corporation

- BASF SE

- Dow

- Dymax Corporation

- Franklin International

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.

- Jowat SE

- MAPEI S.p.A.

- Momentive Performance Materials

- Parker Hannifin (LORD)

- Permabond LLC

- PPG Industries

- Royal Adhesives & Sealants

- RPM International Inc.

- Sika AG

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in lightweighting demand in automotive manufacturing

- 4.2.2 Continued growth in e-commerce boosting packaging adhesives

- 4.2.3 Rising U.S. residential construction and housing starts

- 4.2.4 Adoption of hybrid bonding for mass-timber construction

- 4.2.5 Federal "Buy Clean" incentives for low-VOC bio-based chemistries

- 4.3 Market Restraints

- 4.3.1 Petro-feedstock price volatility

- 4.3.2 Stringent VOC emission limits on solvent-borne systems

- 4.3.3 Skilled-labor shortage for precision adhesive application

- 4.4 Value Chain Analysis

- 4.5 Distribution Channel Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 By Technology

- 5.2.1 Hot-Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV-Cured

- 5.2.5 Water-borne

- 5.3 By End-User Industry

- 5.3.1 Aerospace

- 5.3.2 Automotive

- 5.3.3 Building and Construction

- 5.3.4 Footwear and Leather

- 5.3.5 Healthcare

- 5.3.6 Packaging

- 5.3.7 Woodworking and Joinery

- 5.3.8 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland Global Holdings

- 6.4.4 Avery Dennison Corporation

- 6.4.5 BASF SE

- 6.4.6 Dow

- 6.4.7 Dymax Corporation

- 6.4.8 Franklin International

- 6.4.9 H.B. Fuller Company

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Huntsman International LLC

- 6.4.12 Illinois Tool Works Inc.

- 6.4.13 Jowat SE

- 6.4.14 MAPEI S.p.A.

- 6.4.15 Momentive Performance Materials

- 6.4.16 Parker Hannifin (LORD)

- 6.4.17 Permabond LLC

- 6.4.18 PPG Industries

- 6.4.19 Royal Adhesives & Sealants

- 6.4.20 RPM International Inc.

- 6.4.21 Sika AG

- 6.4.22 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment