PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066662

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066662

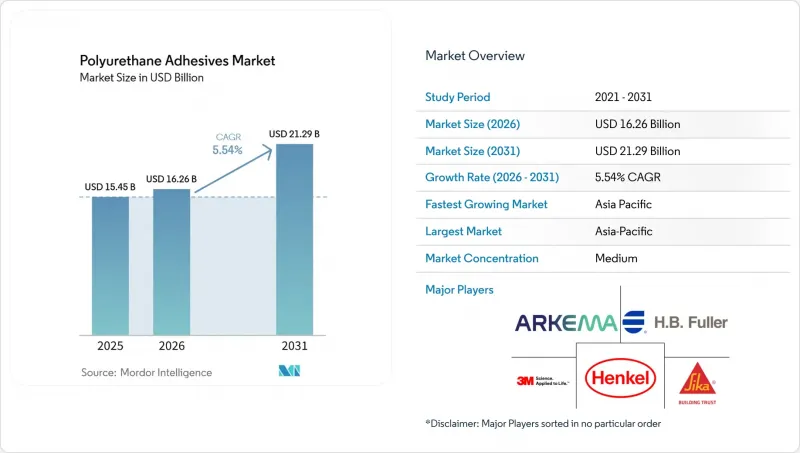

Polyurethane Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the polyurethane adhesives market size is expected to increase from USD 15.45 billion in 2025 to USD 16.26 billion in 2026 and reach USD 21.29 billion by 2031, growing at a CAGR of 5.54% over 2026-2031.

This report is Segmented by Technology (Hot Melt, Reactive, Solvent-Borne, and More), End User Industry (Aerospace, Automotive, Building and Construction, Footwear and Leather, Healthcare, Packaging, Woodworking and Joinery, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Polyurethane Adhesives Market Trends and Insights

Construction Boom in Emerging Asia-Pacific Economies

India's stepped-up capital expenditure under the National Infrastructure Pipeline is stimulating demand for curtain walls, flooring, and prefab interiors bonded with structural polyurethane adhesives. In China, construction applications already represent a major share of adhesive output value, and growth is pivoting toward battery modules, photovoltaic arrays, and aerospace assemblies that favor low-VOC, fast-cure grades. Suppliers that can certify low residual monomer content and lifecycle durability are gaining preferred-vendor status on large public tenders. The scale of regional infrastructure programs offers procurement leverage that rewards high-volume, sustainability-aligned chemistries. As projects emphasize net-zero targets, polyurethane formulations compatible with automated spraying and panel lamination are displacing solvent-borne epoxies.

Light-Weighting Trend Across Automotive and Aerospace Original Equipment Manufacturers

Automakers are replacing welded reinforcements with adhesive-bonded multi-material joints to enhance fuel economy and crash energy absorption. Polyurethane systems supply vibration damping and gap-filling flexibility, complementing rigid epoxy structures in electric-vehicle battery packs. In aerospace, Hexcel's Modipur injection polyurethane allows complex composite components to cure at low temperatures and short cycles, broadening high-volume applications. OEM examples such as BMW i3/i8 and Airbus A350 underscore the requirement for adhesives that preserve fiber integrity in carbon composites. The resulting demand shift favors polyurethanes tuned for elongation, thermal cycling, and chemical resistance. Long-term contracts reward suppliers offering validated data for multi-substrate compatibility and fatigue life.

Volatility in Methylene Diphenyl Diisocyanate and Toluene Diisocyanate Raw-Material Prices

Weak downstream demand kept isocyanate operating rates moderate in 2025, and price recovery in 2026 hinges more on outages or consolidation than on volume growth. European producers face margin pressure from elevated energy costs and cheaper Asian imports, while the United States-China tariff suspensions have stabilized logistics without boosting demand. Adhesive formulators struggle to pass through cost swings, compressing margins and accelerating the search for ultra-low-monomer or isocyanate-free alternatives. This dynamic nudges converters toward aliphatic solvent-free polyurethane or hybrid chemistries that insulate them from raw-material volatility.

Other drivers and restraints analyzed in the detailed report include:

- Shift From Solvent-Borne to Reactive and Eco-Friendly Chemistries

- Emergence of Modular Off-Site Construction Processes

- Stringent VOC and Isocyanate-Exposure Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reactive systems accounted for a 32.21% share of the polyurethane adhesives market in 2025, reflecting their solvent-free nature, moisture-curing profile, and proven performance on laminates, composites, and multi-layer films. Within this cohort, ultra-low-monomer variants are increasing line speeds and shortening cure windows, thereby expanding the polyurethane adhesives market size for high-throughput flexible packaging lines. UV-cured grades, projected to advance at a 7.12% CAGR between 2026 and 2031, attract medical-device and electronics assemblers that need clear bonds and minimal thermal stress.

Short-wave UV initiators now deliver full cure in under five seconds, enabling inline quality checks and reducing work-in-process inventory. Water-borne polyurethane dispersions are also gaining share in footwear stations that target lower VOC profiles and safer work environments. As converters retrofit lines for precision metering and robot-controlled bead placement, the polyurethane adhesives market records higher pull-through for hybrid chemistries tailored to automated dispensing. Suppliers offering data on rheology drift, nozzle clog resistance, and post-cure green strength solidify preferred-supplier status, expanding the polyurethane adhesives market size within midsize converters upgrading equipment.

Geography Analysis

Asia-Pacific held 45.20% of the market in 2025 and is forecast to grow at 7.34% through 2026 to 2031. Infrastructure investments in the region are fueling sustained demand for panel, flooring, and module assemblies. In response, domestic leaders are expanding design capacities to meet increasing regional needs in flexible packaging, solar modules, and new-energy vehicles. Additionally, as urban retrofits surge in Indonesia and Thailand, there's an increasing demand for low-VOC facade and interior bonding systems, further amplifying opportunities in the polyurethane adhesives market.

North America and Europe show solid replacement demand for smart structural adhesives in modular housing, automated automotive lines, and aerospace composites. Sika's expansion in Sealy, Texas, and Henkel's AI-enabled battery-adhesive platform illustrate regional commitment to high-viscosity and specialty grades that shorten development cycles. Stricter REACH and California AQMD limits steer orders toward water-borne and reactive hybrids, enlarging the polyurethane adhesives market size for compliance-ready chemistries.

South America, the Middle-East, and Africa benefit from Sika's new mortar and admixture plants in Brazil and Morocco. Public housing programs and renewable-energy parks in Brazil and Morocco favor durable, weather-resistant bond lines, extending polyurethane adhesives market penetration into climates with high UV exposure and thermal cycling. Although per-capita consumption trails developed regions, steady infrastructure pipelines promise double-digit volume gains for suppliers that localize technical support and stocking points.

- 3M

- Arkema

- Ashland Global Holdings Inc.

- Avery Dennison Corp.

- Beijing Comens New Materials

- Dow Inc.

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian New Materials

- Huntsman International LLC

- Jowat SE

- Kangda New Materials Group

- MAPEI S.p.A.

- NANPAO Resins Chemical Group

- Parker Hannifin (Lord Corp.)

- Permabond LLC

- Pidilite Industries Ltd.

- Sika AG

- Soudal Holding N.V.

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction boom in emerging Asia-Pacific economies

- 4.2.2 Light-weighting trend across automotive and aerospace OEMs

- 4.2.3 Shift from solvent-borne to reactive, eco-friendly chemistries

- 4.2.4 Emergence of modular off-site construction processes

- 4.2.5 Rapid adoption of AI-controlled dispensing robots on assembly lines

- 4.3 Market Restraints

- 4.3.1 Volatility in MDI/TDI raw-material prices

- 4.3.2 Stringent VOC and isocyanate-exposure regulations, esp. in EU and US

- 4.3.3 Growing competition from silane-modified polyether (SMP) systems

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Competitive Rivalry

- 4.7 End-User Trends

- 4.7.1 Aerospace

- 4.7.2 Automotive

- 4.7.3 Building and Construction

- 4.7.4 Footwear and Leather

- 4.7.5 Packaging

- 4.7.6 Woodworking and Joinery

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Hot Melt

- 5.1.2 Reactive

- 5.1.3 Solvent-borne

- 5.1.4 UV Cured

- 5.1.5 Water-borne

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Footwear and Leather

- 5.2.5 Healthcare

- 5.2.6 Packaging

- 5.2.7 Woodworking and Joinery

- 5.2.8 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 Indonesia

- 5.3.1.6 Thailand

- 5.3.1.7 Malaysia

- 5.3.1.8 Singapore

- 5.3.1.9 Australia

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 United Kingdom

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland Global Holdings Inc.

- 6.4.4 Avery Dennison Corp.

- 6.4.5 Beijing Comens New Materials

- 6.4.6 Dow Inc.

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Hubei Huitian New Materials

- 6.4.10 Huntsman International LLC

- 6.4.11 Jowat SE

- 6.4.12 Kangda New Materials Group

- 6.4.13 MAPEI S.p.A.

- 6.4.14 NANPAO Resins Chemical Group

- 6.4.15 Parker Hannifin (Lord Corp.)

- 6.4.16 Permabond LLC

- 6.4.17 Pidilite Industries Ltd.

- 6.4.18 Sika AG

- 6.4.19 Soudal Holding N.V.

- 6.4.20 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment