PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066670

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066670

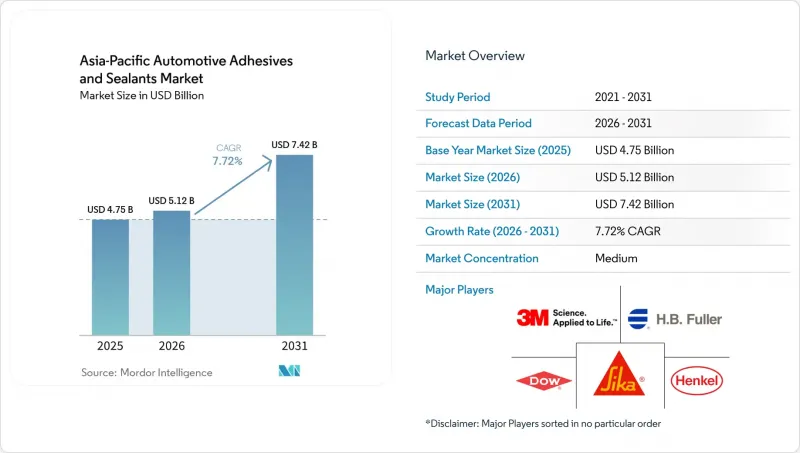

Asia-Pacific Automotive Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific automotive adhesives and Sealants Market size is projected to be USD 4.75 billion in 2025, USD 5.12 billion in 2026, and reach USD 7.42 billion by 2031, growing at a CAGR of 7.72% from 2026 to 2031.

This report is Segmented by Resin (Acrylic, Cyanoacrylate, Epoxy, Polyurethane, Silicone, VAE/EVA, Other Resins), Technology (Hot Melt, Reactive, Sealants, Solvent-Borne, and More), and Geography (Australia, China, India, Indonesia, Japan, Malaysia, Singapore, South Korea, Thailand, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Automotive Adhesives And Sealants Market Trends and Insights

OEM Preference for Multi-Material Body-in-White Designs

Automakers in the region are integrating steel, aluminum, magnesium, and carbon-fiber-reinforced polymers within single structures to reduce curb weight by 8-12%. This change has increased adhesive usage from approximately 15 kilograms to over 25 kilograms per vehicle. ArcelorMittal's multi-phase integration process for Chinese sedans combines ultra-high-strength steel with aluminum closures, a pairing unsuitable for resistance spot-welding due to the risk of galvanic corrosion. In 2025, Seres adopted magnesium die-cast subframes, specifying epoxy structural adhesives that achieve lap-shear strength exceeding 10 megapascals (MPa) without requiring surface pretreatment. Japanese tier-one suppliers report that silyl-modified-polymer sealants, which cure at ambient temperatures, reduce cycle times by eliminating the need for bake ovens. These advancements are embedding adhesives more deeply into high-volume platforms scheduled for launch between 2027 and 2030.

Weight-Reduction Mandates Under China VI and CAFE Norms

China's implementation of China VI B standards in January 2026 will reduce particulate matter thresholds by 30% and nitrogen oxide (NOx) limits by 50%, while real-driving-emissions testing will enhance enforcement. Additionally, original equipment manufacturers (OEMs) must achieve a fleet average of 3.3 liters per 100 kilometers (L/100 km) by 2030, driving the substitution of steel with adhesive-bonded aluminum and composites that eliminate the need for energy-intensive heat tunnels. Hyundai and Kia are following a similar approach, using reactive hot-melts on tailgates and hoods to reduce weight by 3-5 kilograms per closure. Japan's Stage 4 regulations, effective in 2026, extend lightweighting requirements to vans and mini-trucks, increasing supplier demand for qualified one-component polyurethanes.

Volatility in Isocyanate and Epoxy Feedstock Prices

Unplanned methylene diphenyl diisocyanate (MDI) outages and fluctuations in crude oil prices caused spot-market variations through 2025, reducing the margins of smaller ASEAN formulators by 200-300 basis points. The epoxy market weakened in early 2026, leading some suppliers to delay research and development initiatives and capacity expansion plans. DIC's new Chiba epoxy unit, subsidized to ensure domestic supply, highlights the significant capital investment required to manage raw material risks. While silyl-modified polymer alternatives help reduce isocyanate exposure, they remain limited by thermal-aging constraints above 120°C.

Other drivers and restraints analyzed in the detailed report include:

- Uptick in EV Battery-Pack Gasketing Demand

- Start-Ups Commercializing Bio-Based Polyurethane Chemistries

- OEM Push Toward Mechanical Fastening for Ease of Repair

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane is expected to account for 27.25% of the Asia-Pacific Automotive Adhesives & Sealants market share in 2025, driven by its 400% elongation and moisture-curing properties, which are suitable for mixed-substrate joints. Henkel's thermal-conductive polyurethane grades, offering thermal conductivity of 1.2-3.4 watts per meter-kelvin (W/m*K), are widely used in bonding electric vehicle (EV) modules. Epoxy adhesives are utilized in under-hood applications requiring resistance to temperatures up to 180°C, while silicone adhesives are preferred for high-voltage battery packs due to their dielectric strength exceeding 10 kilovolts per millimeter (kV/mm).

Vinyl acetate ethylene/ethylene vinyl acetate (VAE/EVA) water-borne systems, though currently smaller in market share, are projected to grow at a compound annual growth rate (CAGR) of 6.55% through 2031. Their cost-effectiveness and compliance with volatile organic compound (VOC) regulations make them suitable for applications such as headliners and door panels in India. These adhesives help original equipment manufacturers (OEMs) meet Japan's in-cabin formaldehyde limit of 100 micrograms per cubic meter (µg/m3) without requiring ultraviolet (UV) lamp investments. The market for VAE/EVA adhesives is expected to expand significantly, supported by increased regional production capacity from domestic suppliers.

List of Companies Covered in this Report:

- 3M

- Arkema

- Ashland

- DIC Corporation

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International

- ITW Performance Polymers

- Jowat SE

- PARKER HANNIFIN CORP

- Permabond LLC

- Pidilite Industries Ltd.

- PPG Industries, Inc.

- Shanghai Huitian New Material Co., Ltd

- SHINSUNG PETROCHEMICAL

- Sika AG

- THREEBOND INTERNATIONAL, INC

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 OEM preference for multi-material body-in-white designs

- 4.2.2 Weight-reduction mandates under China VI and CAFE norms

- 4.2.3 Uptick in EV battery pack gasketing demand

- 4.2.4 Start-ups commercialising bio-based polyurethane chemistries

- 4.2.5 Emergence of low-surface-energy composite adhesives

- 4.3 Market Restraints

- 4.3.1 Volatility in isocyanate and epoxy feedstock prices

- 4.3.2 OEM push toward mechanical fastening for ease-of-repair

- 4.3.3 Stringent VOC caps in Japan and South Korea

- 4.3.4 Skill-gap in robot-dispensing programming at Tier-2 plants

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 By Technology

- 5.2.1 Hot-Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 UV-Cured Adhesives

- 5.2.6 Water-borne

- 5.3 By Geography

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Singapore

- 5.3.8 South Korea

- 5.3.9 Thailand

- 5.3.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/(%)Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 DIC Corporation

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Huntsman International

- 6.4.9 ITW Performance Polymers

- 6.4.10 Jowat SE

- 6.4.11 PARKER HANNIFIN CORP

- 6.4.12 Permabond LLC

- 6.4.13 Pidilite Industries Ltd.

- 6.4.14 PPG Industries, Inc.

- 6.4.15 Shanghai Huitian New Material Co., Ltd

- 6.4.16 SHINSUNG PETROCHEMICAL

- 6.4.17 Sika AG

- 6.4.18 THREEBOND INTERNATIONAL, INC

- 6.4.19 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment