PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066673

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066673

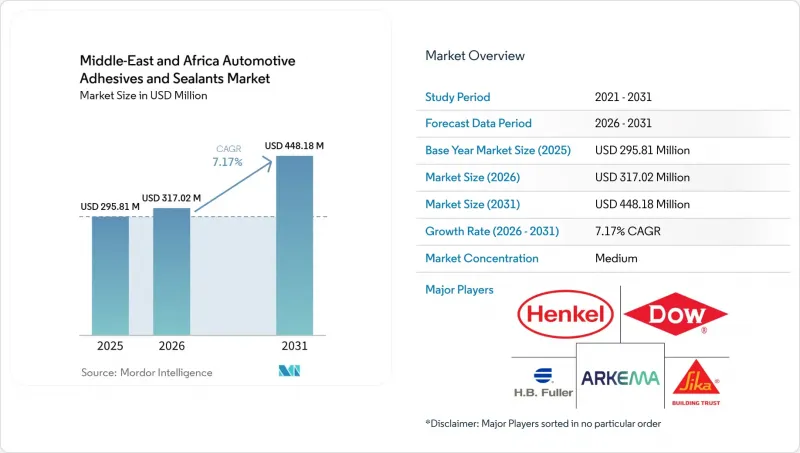

Middle-East And Africa Automotive Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the middle-East and africa automotive adhesives and sealants market size is expected to grow from USD 295.81 million in 2025 to USD 317.02 million in 2026 and is forecast to reach USD 448.18 million by 2031 at 7.17% CAGR over 2026-2031.

This report is Segmented by Resin (Epoxy, Acrylic, Cyanoacrylate, Polyurethane, Silicone, and More), Technology (Water-Borne, Hot-Melt, Reactive, Sealants, Solvent-Borne, and UV-Cured), and Geography (Saudi Arabia, South Africa, United Arab Emirates, Egypt, Nigeria, and Rest of Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Middle-East And Africa Automotive Adhesives And Sealants Market Trends and Insights

Lightweighting Drive to Meet Regional CAFE-Equivalent Standards

Increasing Corporate Average Fuel Economy targets are pushing OEMs to reduce vehicle weight, leading to the substitution of welds with structural epoxies and polyurethanes. These materials provide up to 15% weight savings while maintaining crash energy absorption. For example, a 62% aluminum body-in-white bonded with 180 meters of epoxy reduced curb weight by 100 kg, highlighting the adhesive requirements for mixed-material constructions. Regional suppliers co-locating formulation lines near Ceer's and MG's new plants secure long-term volumes but must manage higher capital investments to meet local-content thresholds.

EV Battery-Pack Bonding Requirements in Hot Climates

Lithium-ion battery packs operating in ambient temperatures above 50 °C require adhesives with thermal conductivity up to 3.4 W/mK and UL 94 V-0 flame ratings. Two-part polyurethane gap fillers meet these requirements but face challenges such as reduced pot life in non-air-conditioned warehouses. To address this, formulators are extending working times using latent-cure catalysts. Morocco's 20 GWh LFP cell line alone is expected to consume approximately 2,000 tons of such materials annually, encouraging the setup of on-site mixing stations within the gigafactory premises.

Volatile MDI and Epoxy Raw-Material Costs

Spot prices for methylene diphenyl di-isocyanate (MDI) rose by 5.86% week-on-week in Q1 2026 after a regional force majeure reduced supply by 15%. Epoxy resin prices increased to USD 3.18 per kg, marking a 38.9% year-on-year rise. These cost increases are squeezing formulator margins on fixed-price OEM contracts and accelerating the transition to more cost-effective acrylic and VAE/EVA chemistries.

Other drivers and restraints analyzed in the detailed report include:

- OEM Localization Policies Boosting Tier-1 Adhesive Sourcing

- Aftermarket Collision-Repair Boom in GCC

- Stringent VOC Limits on Solvent-Borne Chemistries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy resins held 17.46% of the Middle-East and Africa automotive adhesives and sealants market share in 2025, attributed to their 25 MPa lap-shear strength and 180 °C service temperature, which are essential for aluminum-steel assemblies in new EV platforms. Meanwhile, polyurethane and silicone chemistries continue to serve specific applications such as glazing and under-hood gaskets, where elastic recovery or continuous exposure to 150 °C is required.

VAE/EVA resins are projected to grow at the fastest CAGR of 7.31% through 2031, driven by their sub-3-second set times and zero-VOC emissions, making them suitable for hot-melt headliner and carpet-backing applications. Enhanced hydrolysis resistance in advanced VAE grades supports their use in humid coastal regions while meeting interior-odor standards, creating opportunities in door-panel lamination and pillar trims.

List of Companies Covered in this Report:

- 3M

- ACC Gulf

- Arkema

- Avery Dennison Corporation

- BASF

- DELO Industrial Adhesives

- Dow

- Dymax

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers

- PARKER HANNIFIN CORP

- Permabond LLC

- Pidilite Industries Ltd.

- PPG Industries, Inc.

- RPM International Inc.

- Sika AG

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Lightweighting drive to meet regional CAFE-equivalent standards

- 4.2.2 EV battery-pack bonding requirements in hot climates

- 4.2.3 OEM localization policies boosting Tier-1 adhesive sourcing

- 4.2.4 Aftermarket collision-repair boom in GCC

- 4.2.5 Surge in aluminum and multi-material car bodies

- 4.2.6 Growth of MEA gigafactories for e-mobility

- 4.3 Market Restraints

- 4.3.1 Volatile MDI and epoxy raw-material costs

- 4.3.2 Stringent VOC limits on solvent-borne chemistries

- 4.3.3 Limited cold-chain logistics for two-part systems

- 4.3.4 Skilled-labor shortages for automated dispensing

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin

- 5.1.1 Epoxy

- 5.1.2 Acrylic

- 5.1.3 Cyanoacrylate

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 By Technology

- 5.2.1 Water-borne

- 5.2.2 Hot-melt

- 5.2.3 Reactive

- 5.2.4 Sealants

- 5.2.5 Solvent-borne

- 5.2.6 UV-cured

- 5.3 By Geography

- 5.3.1 Saudi Arabia

- 5.3.2 South Africa

- 5.3.3 United Arab Emirates

- 5.3.4 Egypt

- 5.3.5 Nigeria

- 5.3.6 Rest of Middle-East and Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 ACC Gulf

- 6.4.3 Arkema

- 6.4.4 Avery Dennison Corporation

- 6.4.5 BASF

- 6.4.6 DELO Industrial Adhesives

- 6.4.7 Dow

- 6.4.8 Dymax

- 6.4.9 H.B. Fuller Company

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Huntsman International LLC

- 6.4.12 ITW Performance Polymers

- 6.4.13 PARKER HANNIFIN CORP

- 6.4.14 Permabond LLC

- 6.4.15 Pidilite Industries Ltd.

- 6.4.16 PPG Industries, Inc.

- 6.4.17 RPM International Inc.

- 6.4.18 Sika AG

- 6.4.19 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment