PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066671

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066671

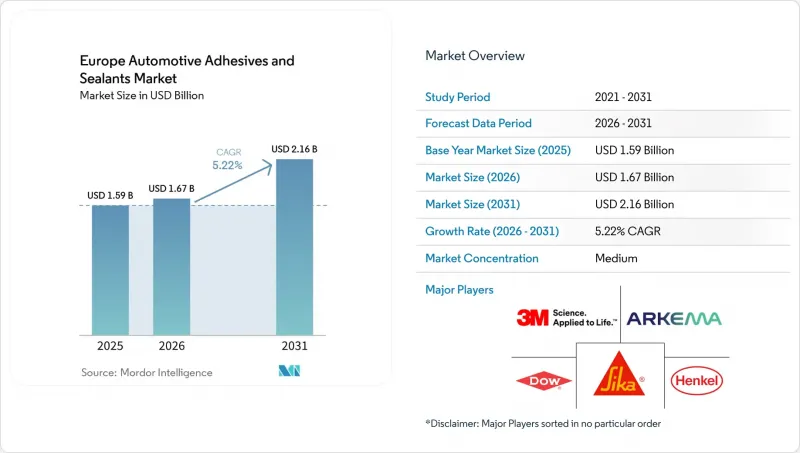

Europe Automotive Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe automotive adhesives and sealants market size was valued at USD 1.59 billion in 2025 and is estimated to grow from USD 1.67 billion in 2026 to reach USD 2.16 billion by 2031, at a CAGR of 5.22% during the forecast period (2026-2031).

This report is Segmented by Resin (Acrylic, Cyanoacrylate, Epoxy, Polyurethane, Silicone, VAE/EVA, Other Resins), Technology (Hot Melt, Reactive, Sealants, Solvent-Borne, UV-Cured Adhesives, Water-Borne), and Geography (France, Germany, Italy, Russia, Spain, United Kingdom, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Europe Automotive Adhesives And Sealants Market Trends and Insights

Lightweighting Drive for EV and ICE Vehicles

Aluminum, composites, and mixed-material architectures are replacing traditional spot-welds with high-peel polyurethane and epoxy bonds. These bonding methods distribute loads effectively and reduce stress concentrations. Hydro achieved a 30% reduction in mass by replacing steel closures with aluminum, maintaining the material's 90% recyclability. BMW's i-Series used elastomer-toughened epoxies to bond carbon fiber to aluminum, addressing thermal-expansion mismatches and protecting the fibers. Audi has improved its formulation cycles by utilizing artificial intelligence (AI)-driven finite-element simulations to evaluate potential chemistries, reducing qualification lead times. The European Union (EU) Automotive Package, which includes a EUR 1.8 billion (USD 2.10 billion) battery incentive, is encouraging original equipment manufacturers (OEMs) to reduce vehicle weight by 100-150 kilograms. This trend is driving the shift from traditional bolts to modern adhesive solutions.

EU VOC-Reduction Regulations Accelerate Low-VOC Chemistries

Directive 2004/42/EC has set a cap of 420 grams per liter (g/l) for volatile organic compounds (VOCs) in topcoats. This regulation is nudging formulators towards more eco-friendly routes, specifically water-borne and ultraviolet (UV)-cure methods. Henkel AG & Co. KGaA's AQUENCE PL 5101, a one-component water-borne adhesive, eliminates the typical four-hour pot-life waste associated with two-part mixes. It also allows line flushes using soapy water. Tesa's 52215 Ultra-Low-VOC tape is making progress in the heating, ventilation, and air conditioning (HVAC) sector, bonding recycled polypropylene seals while adhering to VDA 278 cabin-air standards. However, this tape has a drawback: its lower initial tack extends fixture times. Toyochem's UV-curable TOYOMELT P-201 series addresses this challenge, offering instant curing and 100°C heat resistance, all without the use of solvents.

Isocyanate Price Volatility

In early 2026, prices for Methylene Diphenyl Diisocyanate (MDI) and Toluene Diisocyanate (TDI) increased significantly due to Middle-East tensions disrupting feedstock supply routes. ICIS reported a polyol midpoint price increase of USD 450 per ton within a week. Producers such as BASF and Huntsman implemented price increases ranging from EUR 100 to 300 (USD 117.16 to 351.48) per ton, creating challenges for Tier-2 formulators without long-term contracts. Utilization rates remain around 82%, providing limited relief until new Chinese production capacity transitions to export-grade materials. Original Equipment Manufacturers (OEMs), already under pressure from electric vehicle (EV) margin constraints, are resisting cost pass-throughs, further compressing formulation EBITDA.

Other drivers and restraints analyzed in the detailed report include:

- Surge in European EV Battery-Pack Production

- In-Line Robotic Dispensing Boosts OEM Throughput

- REACH Chemical-Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane accounted for 26.63% of the projected 2025 revenue, driven by its high peel strength (greater than 20 MPa) and impact resilience, which are critical for battery enclosures and body-in-white assemblies. Companies such as Henkel and Dow have invested USD 20 million in expanding a German reactive hot-melt production line to ensure supply. Meanwhile, vinyl acetate ethylene/ethylene vinyl acetate (VAE/EVA) water-borne chemistries are expected to grow at a compound annual growth rate (CAGR) of 5.88% through 2031, as original equipment manufacturers (OEMs) increasingly adopt low-volatile organic compound (VOC) solutions for dashboards and roof-liners. Epoxies continue to dominate module potting applications, with innovations such as Nagoya University's epoxy-thermoplastic elastomer (TPE) hybrid demonstrating 22X impact strength, indicating long-term durability. Silicones, including WEVO-CHEMIE's WEVOSIL 28015 FL, are gaining traction in high-temperature battery seals, meeting the demands of -40°C to +85°C cycling with elastic recovery.

The growth of VAE/EVA does not signal the decline of polyurethanes; instead, both chemistries are expected to coexist, addressing varying requirements for operating temperature and modulus across vehicle zones. For instance, Evonik's VPS SIVO 260 silane promoters enhance polycarbonate adhesion by 27%, ensuring polyurethane remains relevant for transparent roof architectures. Additionally, circular-economy regulations are driving research into beta-amino-ester debondable epoxies, signaling a potential shift toward easier end-of-life disassembly in the coming decade.

List of Companies Covered in this Report:

- 3M

- Alpha Adhesives & Sealants

- Anabond Ltd.

- Arkema

- BASF

- DELO Industrial Adhesives

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian Adhesive

- Huntsman International LLC

- ITW Performance Polymers

- Jowat SE

- PARKER HANNIFIN CORP

- Permabond LLC

- PPG Industries

- Sika AG

- Uniseal Inc.

- Wacker Chemie AG

- Wurth Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Lightweighting drive for EV and ICE vehicles

- 4.2.2 EU VOC-reduction regulations accelerate low-VOC chemistries

- 4.2.3 Surge in European EV battery-pack production

- 4.2.4 In-line robotic dispensing boosts OEM throughput

- 4.2.5 Sensor-embedded "smart" structural adhesives emerge

- 4.3 Market Restraints

- 4.3.1 Isocyanate price volatility

- 4.3.2 REACH chemical-compliance costs

- 4.3.3 Shortage of high-viscosity dosing equipment for battery lines

- 4.3.4 OEM certification delays for novel bio-based systems

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 By Technology

- 5.2.1 Hot-Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 UV-Cured Adhesives

- 5.2.6 Water-borne

- 5.3 By Geography

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/(%)Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Alpha Adhesives & Sealants

- 6.4.3 Anabond Ltd.

- 6.4.4 Arkema

- 6.4.5 BASF

- 6.4.6 DELO Industrial Adhesives

- 6.4.7 Dow

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Hubei Huitian Adhesive

- 6.4.11 Huntsman International LLC

- 6.4.12 ITW Performance Polymers

- 6.4.13 Jowat SE

- 6.4.14 PARKER HANNIFIN CORP

- 6.4.15 Permabond LLC

- 6.4.16 PPG Industries

- 6.4.17 Sika AG

- 6.4.18 Uniseal Inc.

- 6.4.19 Wacker Chemie AG

- 6.4.20 Wurth Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment