PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072498

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072498

Singapore Motor Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

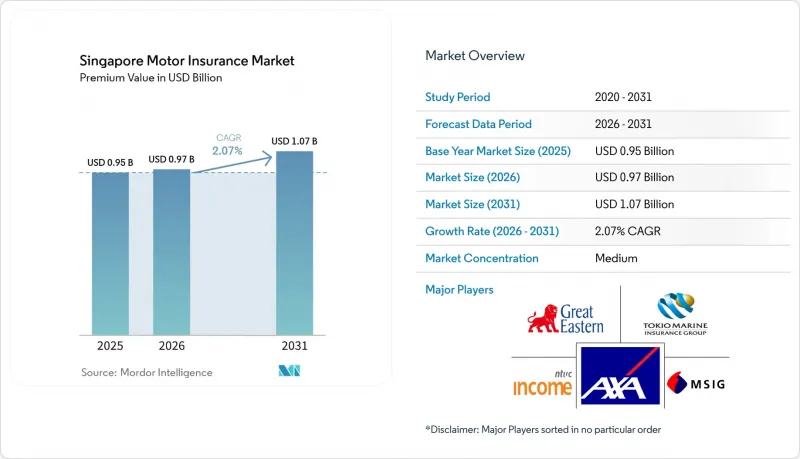

According to Mordor Intelligence, the singapore motor insurance market size in terms of premium value is expected to grow from USD 0.95 billion in 2025 to USD 0.97 billion in 2026 and is forecast to reach USD 1.07 billion by 2031 at 2.07% CAGR over 2026-2031.

This report is Segmented by Policy Type (Comprehensive, Third-Party Fire and Theft, Usage Based and More), Vehicle Type (Private Passenger Car, Motorcycles, and Scooters, and More), Distribution Channel (Agents and Brokers, Direct, Online Price Aggregators, Bancassurance and Automotive Dealerships), and End Users (Personal, Commercial). The Market Forecasts are Provided in Terms of Value (USD)

Singapore Motor Insurance Market Trends and Insights

Mandatory Third-Party Motor Insurance Compliance Under Singapore Law

In Singapore, the Motor Vehicles (Third-Party Risks and Compensation) Act mandates motor insurance, significantly shaping the nation's motor insurance landscape. Legally, every motor vehicle must possess third-party liability coverage. Those who flout this rule face fines or imprisonment, leading to almost universal policy adoption and a consistent premium volume. The Motor Insurers' Bureau bolsters market integrity by compensating victims in incidents with uninsured drivers. Regulatory moves, like mandating accident reports to insurers, aim to curb fraud and speed up claims. The General Insurance Association notes that stringent enforcement has kept motor insurance penetration near 100%. This high penetration grants insurers a predictable market, enabling them to pivot from merely acquiring customers to innovating in product development and refining risk analytics.

EV Adoption Driving Specialized Policies and Coverage Extensions

In Singapore, the surge in electric vehicle (EV) adoption is spurring the evolution of specialized motor insurance policies. While EVs constituted a mere 3.3% of the national car parc in 2024, they dominated new vehicle registrations at 32.5%. This spike is largely attributed to government incentives reaching up to SGD 40,000. Insurers are now crafting products that cater to unique EV risks, including battery degradation, potential damage to charging equipment, and cyber threats. Reflecting the elevated repair costs and the scarcity of spare parts, these tailored policies come with a 15-20% premium over traditional motor insurance. A standout in this arena is Income Insurance's eDrivo plan, boasting features like 24/7 mobile charging support and optional battery replacement coverage. With EV prices on a downward trend and the public charging infrastructure broadening, the premium pool for EV insurance is poised for double-digit growth, underscoring its significance as a strategic growth avenue for insurers.

Price Wars and Discounting on Aggregators Compress Underwriting Margins

Digital insurers are rapidly capturing market share with ultra-low prices, sparking a race-to-the-bottom that tightens margins across the board. In response, some carriers are turning to strategies like offering higher excesses or unbundled add-ons. However, these approaches come with the risk of creating coverage gaps, potentially eroding customer trust. Ongoing discounting pressures the solvency buffers of smaller players, underscoring the critical need for robust capital strength in line with risk-based regulations. The low prices and margins hinders the growth of Singapore motor insurance market.

Other drivers and restraints analyzed in the detailed report include:

- Telematics & Usage-Based Insurance Backed by MAS Sandboxes

- Ride-Hailing and Last-Mile Delivery Fleet Expansion Raising Policy Demand

- Vehicle Population Plateau Limits New Policy Volume

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Comprehensive cover dominated with a 71.85% share in 2025 because high car values and dense traffic elevate perceived loss severity. The Singapore motor insurance market size tied to comprehensive policies is projected to edge up at 1.79% CAGR, underpinned by COE-driven vehicle valuations. Third-party fire-and-theft plus third-party only policies serve older or budget vehicles but face cannibalization when drivers shift to flexible usage-based plans.

Adoption of telematics is reshaping premium mechanics. Usage-based contracts grow 12.12% annually as drivers embrace mileage-linked savings, and MAS sandboxes shorten launch cycles. The Singapore motor insurance market share of usage-based policies would materially dilute fixed-premium dominance, forcing incumbents to refine risk-scoring algorithms and telematics partnerships.

Private cars contributed 80.78% of written premiums in 2025, yielding a stable but low-growth segment because registration caps persist. The Singapore motor insurance market size for private cars is forecast to inch forward at only 1.59% CAGR through 2031. Conversely, motorcycles and scooters record 13.02% CAGR, supported by affordability and delivery-fleet demand, albeit from a lower base.

Electric vehicles inject complexity into underwriting because batteries, power electronics, and aluminium bodywork push repair bills higher. EV policies carry premiums 15-20% costlier than combustion models; however, incentives and charging-network rollout fuel rapid parc growth. By 2030, EVs may comprise a tenth of registered cars, magnifying their impact on loss ratios and giving data-rich insurers an underwriting edge.

Complete Report Scope:

- By Policy Type

- Comprehensive Cover

- Third-Party, Fire & Theft

- Third-Party Only

- Usage-Based / Pay-As-You-Drive Policies

- By Vehicle Type

- Private Passenger Cars

- Motorcycles & Scooters

- Commercial & Light Goods Vehicles

- By Distribution Channel

- Agents & Brokers

- Direct (Insurer Website / Branch)

- Online Price Aggregators

- Bancassurance

- Automotive Dealerships

- By End-User

- Personal Lines

- Commercial Lines

List of Companies Covered in this Report:

- NTUC Income Insurance Co-operative Ltd

- Great Eastern General Insurance Ltd

- MSIG Insurance (Singapore) Pte. Ltd.

- AXA Insurance Pte Ltd (HSBC Life Singapore)

- Tokio Marine Insurance Singapore Ltd

- Sompo Insurance Singapore Pte. Ltd.

- Liberty Insurance Pte Ltd

- DirectAsia Insurance (Singapore) Pte. Ltd.

- Etiqa Insurance Pte. Ltd.

- QBE Insurance (Singapore) Pte. Ltd.

- China Taiping Insurance (Singapore) Pte. Ltd.

- India International Insurance Pte. Ltd.

- Chubb Insurance Singapore Ltd

- AIG Asia Pacific Insurance Pte. Ltd.

- HL Assurance Pte. Ltd.

- FWD Singapore Pte. Ltd.

- Zurich Insurance Company Ltd (Singapore Branch)

- Singapore Life Ltd (Singlife)

- Great American Insurance Company, Singapore Branch

- Allianz Insurance Singapore Pte. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory Third-Party Motor Insurance Compliance Under Singapore Law

- 4.2.2 EV Adoption Driving Specialized Policies and Coverage Extensions

- 4.2.3 Telematics & Usage-Based Insurance Backed by MAS Sandboxes

- 4.2.4 Ride-Hailing and Last-Mile Delivery Fleet Expansion Raising Policy Demand

- 4.2.5 Digital Aggregators Accelerating Direct-to-Consumer Sales Uptake

- 4.2.6 Singpass-Enabled e-KYC Streamlining Policy Issuance

- 4.3 Market Restraints

- 4.3.1 Price Wars and Discounting on Aggregators Compress Underwriting Margins

- 4.3.2 Vehicle Population Plateau Limits New Policy Volume

- 4.3.3 MAS Risk-Based Capital Rules Elevate Solvency Costs for Small Insurers

- 4.3.4 Claims Inflation From ADAS & EV Parts Escalates Repair Expenses

- 4.4 Value / Supply-Chain Analysis

- 4.5 Emerging Trends

- 4.6 Regulatory Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Policy Type

- 5.1.1 Comprehensive Cover

- 5.1.2 Third-Party, Fire & Theft

- 5.1.3 Third-Party Only

- 5.1.4 Usage-Based / Pay-As-You-Drive Policies

- 5.2 By Vehicle Type

- 5.2.1 Private Passenger Cars

- 5.2.2 Motorcycles & Scooters

- 5.2.3 Commercial & Light Goods Vehicles

- 5.3 By Distribution Channel

- 5.3.1 Agents & Brokers

- 5.3.2 Direct (Insurer Website / Branch)

- 5.3.3 Online Price Aggregators

- 5.3.4 Bancassurance

- 5.3.5 Automotive Dealerships

- 5.4 By End-User

- 5.4.1 Personal Lines

- 5.4.2 Commercial Lines

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 NTUC Income Insurance Co-operative Ltd

- 6.4.2 Great Eastern General Insurance Ltd

- 6.4.3 MSIG Insurance (Singapore) Pte. Ltd.

- 6.4.4 AXA Insurance Pte Ltd (HSBC Life Singapore)

- 6.4.5 Tokio Marine Insurance Singapore Ltd

- 6.4.6 Sompo Insurance Singapore Pte. Ltd.

- 6.4.7 Liberty Insurance Pte Ltd

- 6.4.8 DirectAsia Insurance (Singapore) Pte. Ltd.

- 6.4.9 Etiqa Insurance Pte. Ltd.

- 6.4.10 QBE Insurance (Singapore) Pte. Ltd.

- 6.4.11 China Taiping Insurance (Singapore) Pte. Ltd.

- 6.4.12 India International Insurance Pte. Ltd.

- 6.4.13 Chubb Insurance Singapore Ltd

- 6.4.14 AIG Asia Pacific Insurance Pte. Ltd.

- 6.4.15 HL Assurance Pte. Ltd.

- 6.4.16 FWD Singapore Pte. Ltd.

- 6.4.17 Zurich Insurance Company Ltd (Singapore Branch)

- 6.4.18 Singapore Life Ltd (Singlife)

- 6.4.19 Great American Insurance Company, Singapore Branch

- 6.4.20 Allianz Insurance Singapore Pte. Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment