PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072499

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072499

Philippines Motor Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

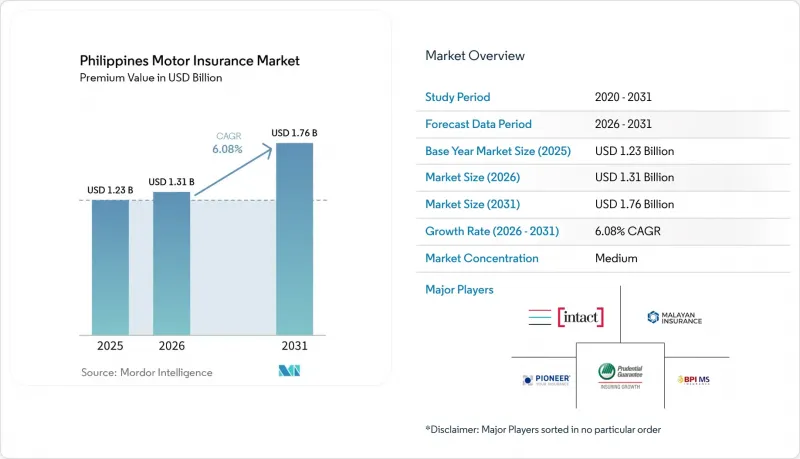

According to Mordor Intelligence, the philippines motor insurance market size in terms of premium value is projected to expand from USD 1.23 billion in 2025 and USD 1.31 billion in 2026 to USD 1.76 billion by 2031, registering a CAGR of 6.08% between 2026 to 2031.

This report is Segmented by Coverage Type (Third-Party Liability, Own-Vehicle Damage, and More), Vehicle Type (Passenger Cars, Commercial Vehicles), Distribution Channel (Direct, Agents/Brokers, and More), Powertrain (ICE Vehicles, and More) and Geography (National Coverage With Concentration in Luzon, Visayas, Mindanao). The Market Forecasts are Provided in Terms of Value (USD).

Philippines Motor Insurance Market Trends and Insights

Mandatory CTPL For Registration

Mandatory CTPL ties insurance to vehicle registration, which sustains a large and recurring policy base across the Philippines motor insurance market as annual renewals reinforce compliance at the Land Transportation Office. The Insurance Commission doubled minimum third-party liability limits in March 2024 and raised no-fault indemnity, which increased the cover value and expanded premium pools for licensed CTPL providers. Online pre-validation of Certificates of Coverage through LTO and DBP Data Center enables real-time verification during registration, which reduces fraudulent certificates and helps stabilize pricing economics for the Philippines motor insurance market. Motor car insurance's prominent role in non-life premiums creates steady inflows that help carriers maintain coverage availability and product variety in the Philippines motor insurance market. As digitization improves transparency at the point of registration, insurers can align pricing with risk and streamline distribution, which supports broader compliance and healthier growth profiles across the Philippines motor insurance market.

Growth In Vehicle Fleet and Motorization

Vehicle registrations and the shift to newer propulsion technologies generate incremental policy opportunities across the Philippines motor insurance market, as each new unit requires at least CTPL, and many opt for broader cover over time. EV registrations rose strongly, and the Electric Vehicle Industry Development Act framework supports adoption through fiscal incentives and policy targets that extend premium potential into new risk categories. The Department of Energy's roadmap outlines multi-year EV expansion under clean energy scenarios, which encourages insurers to tailor products for battery risks, charging infrastructure liabilities, and evolving repair ecosystems in the Philippines motor insurance market. Growth is no longer confined to Metro Manila as digitized verification and online distribution enable insurers to reach provincial areas more efficiently across Visayas and Mindanao. Expansion in emerging economic corridors and logistics hubs increases commercial fleet exposure, which adds volume and diversifies risk in the Philippines motor insurance market. Together, these dynamics sustain a long-term growth runway as motorization deepens and product sophistication rises in the Philippines motor insurance market.

Low Overall Insurance Penetration

Insurance penetration remains below regional benchmarks, which limits the addressable base for voluntary motor cover beyond the mandatory CTPL in the Philippines motor insurance market. While density and penetration improved in 2025, the aggregate level suggests significant room to grow through financial education and easier purchasing journeys. Market participants are expanding digital channels and bancassurance to close awareness and access gaps across the Philippines motor insurance market. Greater inclusion can shift more motorists from CTPL-only to comprehensive and add-ons, which raises average premiums and deepens protection over time. Progress relies on trust-building and frictionless verification at the point of vehicle registration to support consistent take-up in the Philippines motor insurance market. Over the medium term, better enforcement and wider digital reach can help narrow gaps across regions in the Philippines motor insurance market.

Other drivers and restraints analyzed in the detailed report include:

- Motor's Dominant Share in Non-Life Premiums

- Macroeconomic Growth and Rising Insurance Density

- Affordability Constraints For Households

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Third-party liability coverage led with 63.50% of the Philippines motor insurance market share in 2025, supported by the compulsory requirement linked to annual vehicle registration at the Land Transportation Office. The March 2024 increase in mandatory CTPL benefits broadened policy value, which lifted premium capacity and helped formalize the base for recurring renewals in the Philippines motor insurance market. Better verification through the LTO and DBP Data Center reduces fake certificates, which stabilizes pricing and improves the customer experience at registration. As digital distribution and bancassurance mature, more motorists consider add-ons that fit specific needs, which slowly shifts coverage beyond basic liability in the Philippines motor insurance market. These moves reinforce CTPL's role as the entry point while creating space for incremental value through tailored products in the Philippines motor insurance market.

Own-vehicle damage is the fastest-growing optional cover, supported by rising insurance density and product innovation that makes comprehensive protection easier to buy and manage in the Philippines motor insurance market. The Philippines motor insurance market size for own-vehicle damage is projected to expand at a 9.56% CAGR between 2026 and 2031 as digital workflows and partnerships lower friction and improve access. Wider add-on adoption, such as roadside assistance and accident riders, supports policy differentiation as insurers serve varied consumer profiles across regions. Bancassurance partners also cross-sell motor cover to loan and deposit clients, which raises attach rates and broadens protection beyond CTPL in the Philippines motor insurance industry. As unit economics improve through technology and scale, carriers can sustain product breadth and service quality in the Philippines motor insurance market.

Passenger cars commanded 56.80% of the Philippines motor insurance market share in 2025, reflecting their larger base in urban centres and sustained consumer preference for private mobility. Carriers maintain steady renewal volumes from multi-year vehicle finance, and they use technology to reduce friction in quotes, binding, and claims for car owners in the Philippines motor insurance market. As macro stability and insurance density improve, a portion of CTPL-only policies migrate toward broader cover, which supports average premium growth for passenger cars. Bancassurance channels add reach by bundling motor products at the point of financing, which strengthens cross-sell in the Philippines motor insurance market. Digital verification and improved claims response contribute to higher satisfaction for passenger car policyholders in the Philippines motor insurance market.

Commercial vehicles are set to outpace overall market growth as logistics, e-commerce, and provincial development raise fleet needs across the Philippines motor insurance market. The Philippines motor insurance market size for commercial vehicles is projected to expand at a 12.66% CAGR between 2026 and 2031 as operators seek cover for vehicle damage, cargo liability, and business disruption. Risk solutions tailored to fleet operators, including driver programs and route risk management, support lower loss ratios and improved retention in the Philippines motor insurance market. Insurers are also aligning with road safety action plans and infrastructure schedules to refine pricing and improve service reliability for commercial clients. These factors combine to maintain the commercial segment's strong growth momentum in the Philippines motor insurance industry.

Complete Report Scope:

- By Coverage Type

- Third-Party Liability

- Own-Vehicle Damage

- Collision

- Comprehensive (Theft, Glass, Fire, etc.)

- Assistance & Add-ons (Roadside, Legal)

- By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- By Distribution Channel

- Direct

- Agents/Brokers

- Banks

- Embedded Channels (OEM, Affinity, etc.)

- Digital Platforms and Other Emerging Channels

- By Powertrain

- ICE Vehicles

- Electric Vehicles

- Hybrid Vehicles

- Others (Hydrogen FCEV, LPG/CNG, etc.)

List of Companies Covered in this Report:

- Intact Financial Corporation

- Malayan Insurance Group

- Pioneer Insurance Group

- Prudential Guarantee & Assurance (PGA) Group

- BPI MS Insurance Group

- Standard Insurance Group

- Alliedbankers Insurance Group

- Cocogen Insurance Group

- FPG Insurance Group

- PNB Insurance Group

- Sompo Group

- AIG Group (Philippines)

- Oriental Assurance Group

- MAPFRE Group (Philippines)

- Liberty Insurance Group (Philippines)

- Stronghold Insurance Group

- Philippines First Insurance Group

- Bethel Insurance Group

- MAA Insurance Group

- Mercantile Insurance Group

- QBE Group (Philippines) (Seaboard / successor operations)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Mandatory CTPL for registration

- 4.1.2 Growth in vehicle fleet and motorization

- 4.1.3 Motor's dominant share in non-life premiums

- 4.1.4 Macroeconomic growth and rising insurance density

- 4.1.5 High accident and economic loss burden

- 4.1.6 Regulatory strengthening and enforcement actions

- 4.2 Market Restraints

- 4.2.1 Low overall insurance penetration

- 4.2.2 Affordability constraints for households

- 4.2.3 Fake CTPL and unauthorised sellers

- 4.2.4 Road safety and infrastructure gaps raising loss costs

- 4.3 Value / Supply-Chain Analysis

- 4.4 Regulatory or Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Coverage Type

- 5.1.1 Third-Party Liability

- 5.1.2 Own-Vehicle Damage

- 5.1.2.1 Collision

- 5.1.2.2 Comprehensive (Theft, Glass, Fire, etc.)

- 5.1.3 Assistance & Add-ons (Roadside, Legal)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.3 By Distribution Channel

- 5.3.1 Direct

- 5.3.2 Agents/Brokers

- 5.3.3 Banks

- 5.3.4 Embedded Channels (OEM, Affinity, etc.)

- 5.3.5 Digital Platforms and Other Emerging Channels

- 5.4 By Powertrain

- 5.4.1 ICE Vehicles

- 5.4.2 Electric Vehicles

- 5.4.3 Hybrid Vehicles

- 5.4.4 Others (Hydrogen FCEV, LPG/CNG, etc.)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Intact Financial Corporation

- 6.4.2 Malayan Insurance Group

- 6.4.3 Pioneer Insurance Group

- 6.4.4 Prudential Guarantee & Assurance (PGA) Group

- 6.4.5 BPI MS Insurance Group

- 6.4.6 Standard Insurance Group

- 6.4.7 Alliedbankers Insurance Group

- 6.4.8 Cocogen Insurance Group

- 6.4.9 FPG Insurance Group

- 6.4.10 PNB Insurance Group

- 6.4.11 Sompo Group

- 6.4.12 AIG Group (Philippines)

- 6.4.13 Oriental Assurance Group

- 6.4.14 MAPFRE Group (Philippines)

- 6.4.15 Liberty Insurance Group (Philippines)

- 6.4.16 Stronghold Insurance Group

- 6.4.17 Philippines First Insurance Group

- 6.4.18 Bethel Insurance Group

- 6.4.19 MAA Insurance Group

- 6.4.20 Mercantile Insurance Group

- 6.4.21 QBE Group (Philippines) (Seaboard / successor operations)

7 Market Opportunities & Future Outlook