PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073357

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073357

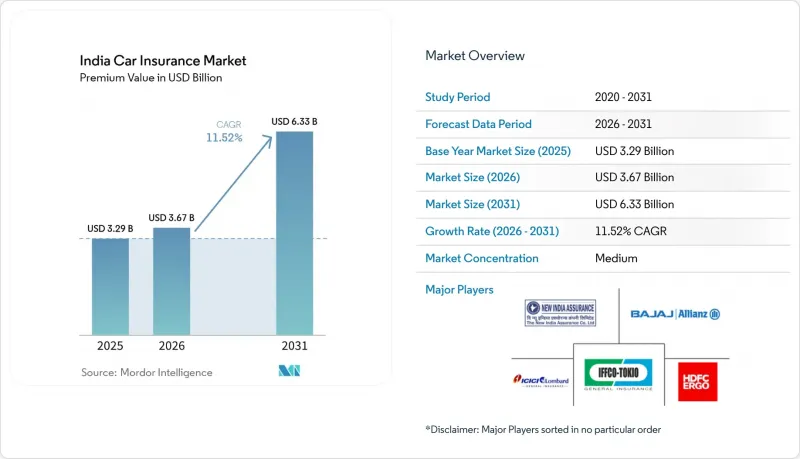

India Car Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india car insurance market size in terms of premium value was valued at USD 3.29 billion in 2025 and is estimated to grow from USD 3.67 billion in 2026 to reach USD 6.33 billion by 2031, at a CAGR of 11.52% during the forecast period (2026-2031).

This report is Segmented by Vehicle Type (Personal, Commercial), Insurance Type (Third Party, Comprehensive), Distribution Channel (Direct, Agents, Brokers, Banks, Other Distribution Channels). The Market Forecasts are Provided in Terms of Value (USD).

India Car Insurance Market Trends and Insights

Strong Vehicle Registration Recovery Drives Premium Volume Growth

Post-FY24 GST cuts lowered purchase prices on entry-level cars, sparking a sharp FY25 jump in passenger-car registrations. Every new vehicle must carry at least third-party cover, so the sales surge converts straight into incremental policies and premium inflows. Gains are most visible in Tier-2 and Tier-3 cities where affordability had stalled insurance uptake and where dealer-assisted financing now bundles multi-year covers by default. Insurers are layering accessories, zero-depreciation, and return-to-invoice add-ons to capture the expanding base and lift average ticket size. Robust retail demand is expected to persist through 2026 as pandemic-era replacement cycles normalize and consumer sentiment improves. Rising showroom traffic is therefore translating into a durable premium tailwind for the India car insurance market.

Digital Distribution Platforms Reshape Customer Acquisition Dynamics

Aggregator portals and insurer apps give buyers instant quotes, video-KYC issuance, and self-service claims, winning trust among digitally native millennials. Policies processed online overtook agent-sourced comprehensive sales in metro areas during FY25, signaling a decisive tilt toward transparent, price-discovery journeys. To defend retention, incumbents are arming agents with mobile CRM tools and embedding click-to-call advisory widgets inside their sites, blending personal advice with digital speed. IRDAI's e-insurance account framework and mandated policy document standardization further favor online channels by cutting paperwork and audit costs. Early evidence shows digital leads are 35% cheaper to acquire than branch walk-ins, strengthening margin upside. Consequently, digital reach has become a core success factor in the India car insurance market.

Stagnant Third-Party Tariff Rates Constrain Revenue Growth

Third-party liability premiums have remained frozen since FY22 while medical inflation and tribunal awards march upward, squeezing top-line growth. Industry combined ratios for TP books now exceed 120%, forcing carriers to cross-subsidize losses with profits from own-damage and investment income. Several rounds of actuarial submissions to IRDAI advocating a 10-15% tariff hike remain under review, prolonging uncertainty. Smaller insurers with heavy motor portfolios face solvency pressure and may curtail product innovation until relief arrives. Prolonged margin compression risks deterring fresh capital inflows and could slow technological upgrades essential for customer experience. Without an imminent tariff revision, the India car insurance market may witness consolidation as weaker players seek scale partners.

Other drivers and restraints analyzed in the detailed report include:

- Telematics and Usage-Based Insurance Gain Regulatory Momentum

- Electric Vehicle Insurance Ecosystem Develops Through OEM Partnerships

- Intense Price Competition Erodes Underwriting Discipline

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Commercial vehicle premiums grew faster than personal lines in FY25, supported by e-commerce logistics expansion and rising goods-movement demand. The segment's 11.34% projected CAGR positions it as a key volume engine for the India car insurance market. Fleet owners embrace telematics to cut accident frequency and unlock premium rebates, bolstering adoption. AI-assessed risk scores consider driver behavior, load types, and route congestion, refining policy pricing. Leasing firms bundle coverage within operating contracts, widening penetration in light-commercial sub-segments. Second-hand truck sales channels are now offering micro-tenure covers to address financing tenure mismatches, an innovation strengthening growth prospects.

Personal vehicles still contribute the largest slice, retaining 72.85% of the India car insurance market share in 2025, owing to steady car ownership growth among middle-income households. Urban buyers increasingly opt for add-ons like engine-protect and zero-depreciation covers, lifting average ticket sizes. Two-wheeler sub-lines face lapsation risk due to informal cash-use patterns, prompting insurers to roll out low-premium, multi-year products. Digital claims tracking apps raise satisfaction scores, aiding renewal conversions. Yet, slowing metro sales and premium discounting temper growth, making diversification into Tier-2 regions crucial for sustaining the India car insurance market.

Complete Report Scope:

- By Vehicle Type

- Personal

- Commercial

- By Insurance Type

- Third Party

- Comprehensive

- By Distribution Channel

- Direct

- Agents

- Brokers

- Banks

- Other Distribution Channels

List of Companies Covered in this Report:

- New India Assurance Co. Ltd.

- ICICI Lombard General Insurance Co. Ltd.

- Bajaj Allianz General Insurance Co. Ltd.

- HDFC ERGO General Insurance Co. Ltd.

- IFFCO TOKIO General Insurance Co. Ltd.

- United India Insurance Co. Ltd.

- Oriental Insurance Co. Ltd.

- SBI General Insurance Co. Ltd.

- Tata AIG General Insurance Co. Ltd.

- Cholamandalam MS General Insurance Co. Ltd.

- Reliance General Insurance Co. Ltd.

- Go Digit General Insurance Ltd.

- Acko General Insurance Ltd.

- Future Generali India Insurance Co. Ltd.

- Royal Sundaram General Insurance Co. Ltd.

- Magma HDI General Insurance Co. Ltd.

- Liberty General Insurance Ltd.

- Raheja QBE General Insurance Co. Ltd.

- Universal Sompo General Insurance Co. Ltd.

- Zurich Kotak General Insurance Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Table of Contents - India Car Insurance Market

2 Introduction

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

3 Research Methodology

4 Executive Summary

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Strong rebound in new-vehicle registrations post-FY24 GST cuts

- 5.2.2 Mandatory long-term third-party cover & proposed hike in TP tariffs

- 5.2.3 Rapid shift to digital/aggregator distribution platforms

- 5.2.4 Telematics-based PAYD / PHYD products gaining IRDAI sandbox approval

- 5.2.5 EV-specific premium-financing bundles from OEM-insurer tie-ups

- 5.2.6 AI-driven touch-less claims reducing loss-adjustment expenses

- 5.3 Market Restraints

- 5.3.1 Flat TP tariff revision in FY25 hurting premium growth

- 5.3.2 Price-led competition compressing Motor OD margins

- 5.3.3 Parts inflation from EV battery imports raising claim severity

- 5.3.4 High court back-logs slowing third-party claim settlement

- 5.4 Value / Supply-Chain Analysis

- 5.5 Regulatory Landscape

- 5.6 Technological Outlook

- 5.7 Porter's Five Forces

- 5.7.1 Threat of New Entrants

- 5.7.2 Bargaining Power of Buyers

- 5.7.3 Bargaining Power of Suppliers

- 5.7.4 Threat of Substitutes

- 5.7.5 Competitive Rivalry

6 Market Size & Growth Forecasts (Value, INR Crore)

- 6.1 By Vehicle Type

- 6.1.1 Personal

- 6.1.2 Commercial

- 6.2 By Insurance Type

- 6.2.1 Third Party

- 6.2.2 Comprehensive

- 6.3 By Distribution Channel

- 6.3.1 Direct

- 6.3.2 Agents

- 6.3.3 Brokers

- 6.3.4 Banks

- 6.3.5 Other Distribution Channels

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 7.4.1 New India Assurance Co. Ltd.

- 7.4.2 ICICI Lombard General Insurance Co. Ltd.

- 7.4.3 Bajaj Allianz General Insurance Co. Ltd.

- 7.4.4 HDFC ERGO General Insurance Co. Ltd.

- 7.4.5 IFFCO TOKIO General Insurance Co. Ltd.

- 7.4.6 United India Insurance Co. Ltd.

- 7.4.7 Oriental Insurance Co. Ltd.

- 7.4.8 SBI General Insurance Co. Ltd.

- 7.4.9 Tata AIG General Insurance Co. Ltd.

- 7.4.10 Cholamandalam MS General Insurance Co. Ltd.

- 7.4.11 Reliance General Insurance Co. Ltd.

- 7.4.12 Go Digit General Insurance Ltd.

- 7.4.13 Acko General Insurance Ltd.

- 7.4.14 Future Generali India Insurance Co. Ltd.

- 7.4.15 Royal Sundaram General Insurance Co. Ltd.

- 7.4.16 Magma HDI General Insurance Co. Ltd.

- 7.4.17 Liberty General Insurance Ltd.

- 7.4.18 Raheja QBE General Insurance Co. Ltd.

- 7.4.19 Universal Sompo General Insurance Co. Ltd.

- 7.4.20 Zurich Kotak General Insurance Co. Ltd.

8 Market Opportunities & Future Outlook

- 8.1 Emerging Product Opportunities (EV, Telematics, UBI)

- 8.2 Distribution & Channel Innovation

- 8.3 Strategic Partnerships & Ecosystem Plays