PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073536

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073536

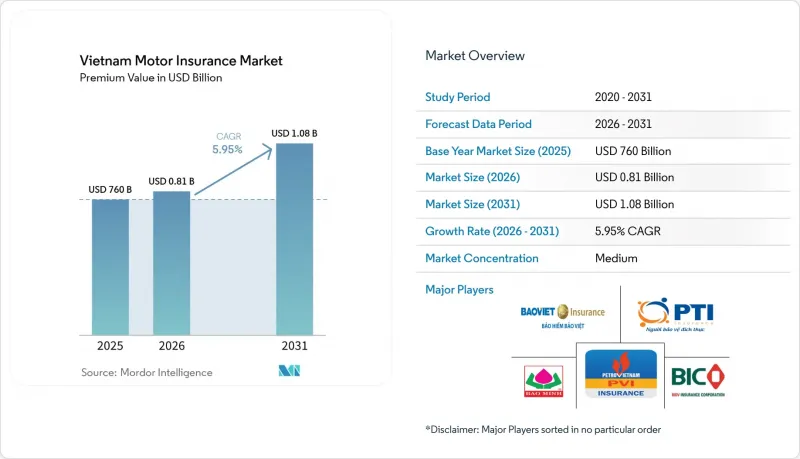

Vietnam Motor Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the vietnam motor insurance market size in terms of premium value is projected to be USD 760 billion in 2025, USD 0.81 billion in 2026, and reach USD 1.08 billion by 2031, growing at a CAGR of 5.95% from 2026 to 2031.

This report is Segmented by Coverage Type (Comprehensive Coverage, Third-Party Liability, Theft and Fire, Personal Accident Add On), Vehicle Type (Passenger Vehicles and Commercial Vehicles, Two Wheelers), and Distribution Channel (Direct, Agents and Brokers and More), End User (Individual, Commercial Fleet), and Region. The Market Forecasts are Provided in Terms of Value (USD).

Vietnam Motor Insurance Market Trends and Insights

Compulsory Third-Party Liability Mandate Driving Policy Uptake

The Vietnam motor insurance market has been reshaped by Decree 67/2023/ND-CP, which fixes premiums by vehicle class and imposes direct insurer accountability for agent conduct. Compliance checks at registration points and cross-border standardisation under the ASEAN Compulsory Motor Insurance System are pulling previously uninsured vehicles into formal cover. Northern and Central provinces, where enforcement had lagged, are now posting double-digit policy growth as local authorities tighten verification. As compulsory uptake saturates, carriers are layering add-ons such as personal-accident and roadside assistance to widen average premiums per policy, sustaining revenue momentum beyond the short-term regulatory spike.

Rapid Growth of Vehicle Ownership in Tier-2 and Tier-3 Cities

Second-tier urban areas are powering the next wave of expansion for the Vietnam motor insurance market. Rising disposable incomes have lifted nationwide auto sales 12.6% in 2024 to 340,142 units, with the sharpest increases in provincial capitals outside Hanoi and Ho Chi Minh City. New owners in these regions often purchase smaller-engine cars or electric two-wheelers, creating risk profiles that differ from metropolitan drivers. Insurers are extending agent networks eastward along coastal growth corridors while deploying app-based quote engines that reach customers where physical branches are scarce. The end of fee exemptions on domestically produced cars in late 2024 briefly cooled demand, underscoring the sensitivity of this growth engine to fiscal policy. Nonetheless, multi-channel carriers that craft lower-ticket, modular products for first-time buyers are winning share in these high-velocity locales.

Price-Sensitive Rural Customers Undermine Profitability

Households in agrarian districts earn a median monthly salary of VND 7.7 million (USD 303), limiting capacity to buy anything beyond mandatory cover. For the Vietnam motor insurance market, low-ticket two-wheeler policies often carry fixed administration costs that erode margins. Insurers are stripping products to core benefits, deploying AI chatbots to cut servicing expense, and synchronising renewals with popular mobile-money apps to lift persistency. Longer term, rising rural incomes and broader credit access may enable upselling to comprehensive packages, but in the medium term, profitability hinges on operational frugality rather than rate increases.

Other drivers and restraints analyzed in the detailed report include:

- Government-Backed E-Certificate Platform Accelerating Digital Policies

- Expansion of Expressways Increasing Long-Distance Driving Risk

- Fraudulent Claims & Parts Counterfeiting Inflate Loss Ratios

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Third-party liability delivered 67.12% of the Vietnam motor insurance market share in 2025, anchored by the compulsory mandate and standardised tariff bands. Comprehensive cover, though starting from a smaller base, is forecast to grow at 8.01% CAGR through 2031 as vehicle values climb and lenders require broader protection. To capture that upside, carriers bundle collision, theft, and natural-catastrophe riders into competitively priced packages, cross-selling during renewal cycles. ACLI alignment across ASEAN corridors has also prompted fleets operating cross-border routes to augment base policies with extended limits, marginally lifting average premiums.

Consumers increasingly perceive the limits of compulsory policies, especially after Typhoon Yagi's VND 10 trillion claim wave. This awareness fuels an upshift toward comprehensive and add-on personal accident covers, tightening the linkage between vehicle financing and insurance. Insurers deploy risk-based pricing that rewards safe-driving history captured via onboard diagnostics. As a result, the Vietnam motor insurance market registers a gradual mix shift that underpins premium growth even as policy counts plateau.

Passenger cars commanded 54.22% of written premiums in 2025, representing the largest slice of the Vietnam motor insurance market size, but electric two-wheelers are poised to outpace with a 9.18% CAGR to 2031. Battery degradation, charger-fire risks, and higher torque profiles demand fresh underwriting parameters. VinFast, holding 43.4% of the electric two-wheeler segment, supplies telematics data to insurance partners, enabling behaviour-based premiums that could reduce claims frequency by up to 12%, according to pilot results shared with regulators. Commercial vehicles, though smaller in policy count, post superior average premiums due to cargo, driver liability, and downtime-loss extensions linked to expressway usage.

Market entrants capitalise on the data gap in new-energy segments by offering flexible deductibles that incentivise responsible charging practices. Early-adopter advantage is significant: the first insurers to launch comprehensive EV motorcycle cover have already secured 40% of issued policies in Ho Chi Minh City. As lithium-ion repair costs fall, actuarial uncertainty will ease, tightening rate bands and stabilising loss experience across the Vietnam motor insurance market.

Complete Report Scope:

- Segmentation by Coverage Type

- Comprehensive Coverage

- Third-Party Liability

- Theft & Fire

- Personal Accident Add-on

- Segmentation by Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Two-Wheelers

- Segmentation by Distribution Channel

- Direct (Online & Company-Owned)

- Agents & Brokers

- Bancassurance

- Segmentation by End-User

- Individual

- Commercial Fleet

- Segmentation by Region

- Northern Vietnam

- Central Vietnam

- Southern Vietnam

List of Companies Covered in this Report:

- Bao Viet Insurance Corporation

- PVI Insurance Corporation

- Post & Telecommunication Insurance Corporation (PTI)

- Bao Minh Insurance Corporation

- Military Insurance Corporation (MIC)

- Petrolimex Insurance Corporation (PJICO)

- Bank for Investment & Development Insurance Corporation (BIC)

- Liberty Insurance Ltd.

- AIG Vietnam Insurance Co. Ltd.

- MSIG Insurance (Vietnam) Co. Ltd.

- Tokio Marine Insurance Vietnam Co. Ltd.

- Fubon Insurance (Vietnam) Co. Ltd.

- Samsung Fire & Marine Insurance (Vietnam) Co. Ltd.

- Hyundai Marine & Fire Insurance Vietnam Co.

- VietinBank Insurance JSC (VBI)

- MBVina Insurance Corporation

- BIDV MetLife

- FWD Insurance Vietnam

- Chubb Insurance Vietnam Co. Ltd.

- Zurich Insurance Vietnam Branch

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Compulsory Third-Party Liability Mandate Driving Policy Uptake

- 4.2.2 Rapid Growth of Vehicle Ownership in Tier-2 & Tier-3 Cities

- 4.2.3 Government-Backed E-Certificate Platform Accelerating Digital Policies

- 4.2.4 Expansion of Expressways Increasing Long-Distance Driving Risk

- 4.2.5 Foreign Insurer Entry Catalyzing Product Innovation & Bundling

- 4.2.6 Usage-Based Insurance Pilots Supported by Telematics Sandbox

- 4.3 Market Restraints

- 4.3.1 Price-Sensitive Rural Customers Undermine Profitability

- 4.3.2 Fraudulent Claims & Parts Counterfeiting Inflate Loss Ratios

- 4.3.3 Margin Squeeze from Intensive Rate Competition Among 30+ Carriers

- 4.3.4 Limited Actuarial Data for New-Energy Vehicles

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of Substitutes

- 4.6.4 Threat of New Entrants

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, VND bn)

- 5.1 Segmentation by Coverage Type

- 5.1.1 Comprehensive Coverage

- 5.1.2 Third-Party Liability

- 5.1.3 Theft & Fire

- 5.1.4 Personal Accident Add-on

- 5.2 Segmentation by Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.2.3 Two-Wheelers

- 5.3 Segmentation by Distribution Channel

- 5.3.1 Direct (Online & Company-Owned)

- 5.3.2 Agents & Brokers

- 5.3.3 Bancassurance

- 5.4 Segmentation by End-User

- 5.4.1 Individual

- 5.4.2 Commercial Fleet

- 5.5 Segmentation by Region

- 5.5.1 Northern Vietnam

- 5.5.2 Central Vietnam

- 5.5.3 Southern Vietnam

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Bao Viet Insurance Corporation

- 6.4.2 PVI Insurance Corporation

- 6.4.3 Post & Telecommunication Insurance Corporation (PTI)

- 6.4.4 Bao Minh Insurance Corporation

- 6.4.5 Military Insurance Corporation (MIC)

- 6.4.6 Petrolimex Insurance Corporation (PJICO)

- 6.4.7 Bank for Investment & Development Insurance Corporation (BIC)

- 6.4.8 Liberty Insurance Ltd.

- 6.4.9 AIG Vietnam Insurance Co. Ltd.

- 6.4.10 MSIG Insurance (Vietnam) Co. Ltd.

- 6.4.11 Tokio Marine Insurance Vietnam Co. Ltd.

- 6.4.12 Fubon Insurance (Vietnam) Co. Ltd.

- 6.4.13 Samsung Fire & Marine Insurance (Vietnam) Co. Ltd.

- 6.4.14 Hyundai Marine & Fire Insurance Vietnam Co.

- 6.4.15 VietinBank Insurance JSC (VBI)

- 6.4.16 MBVina Insurance Corporation

- 6.4.17 BIDV MetLife

- 6.4.18 FWD Insurance Vietnam

- 6.4.19 Chubb Insurance Vietnam Co. Ltd.

- 6.4.20 Zurich Insurance Vietnam Branch

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment