PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073646

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073646

United Kingdom Car Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

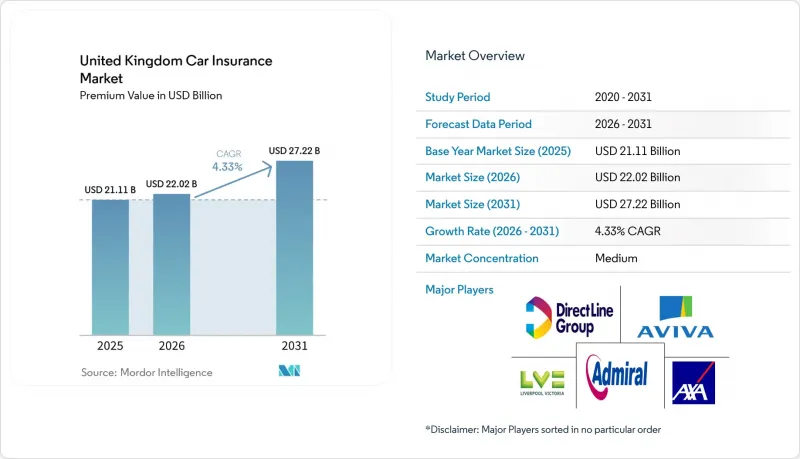

According to Mordor Intelligence, the united kingdom car insurance market size in terms of premium value is expected to increase from USD 21.11 billion in 2025 to USD 22.02 billion in 2026 and reach USD 27.22 billion by 2031, growing at a CAGR of 4.33% over 2026-2031.

This report is Segmented by Coverage Type (Third-Party Liability, Collision/Comprehensive, and More), Application (Personal, Commercial), Distribution Channel (Direct-To-Customer, Intermediated, and Embedded), Vehicle Powertrain (Internal-Combustion, Battery Electric, and More), and Region. The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Car Insurance Market Trends and Insights

Telematics-based usage-based insurance adoption

Usage-based pricing is moving from niche to mainstream as 61% of drivers signal willingness to share vehicle data for customized premiums. Growth accelerates because traditional rating factors understate actual risk, particularly as post-pandemic traffic has rebounded to 105% of 2019 levels. The forthcoming EU-style data-sharing frameworks are likely to increase consumer trust by giving motorists control over telematics consent. Nevertheless, adoption divides along digital affinity lines; technology-savvy motorists embrace data-sharing, while privacy-conscious segments maintain conventional cover. Insurers that orchestrate seamless onboarding and transparent data governance gain a persistent pricing advantage.

Rapid expansion of the UK electric-vehicle parc

Government mandates require 22% of new-car sales to be zero-emission in 2024, and the EV parc's growth reveals wide underwriting gaps. Average EV premiums of USD 1,344 exceed petrol equivalents by 46% because specialized repairs and battery risks elevate severity. A shortage of certified EV technicians drives more total losses for minor damage, lifting claim costs and disrupting parts availability. Chinese manufacturers' limited UK repair infrastructure renders certain models challenging to insure, creating pricing tiers between makes. Insurers that invest early in EV repair networks and training realize profitable niches, while laggards risk margin erosion and reputational setbacks.

Repair-cost and parts-inflation squeezing margins

Average repair bills surged 26% year on year, reaching USD 2 billion in Q3 2024, reflecting sustained cost pressures across the claims value chain. Advanced driver-assistance systems (ADAS) and integrated vehicle electronics increasingly require specialist labour, driving up hourly rates and contributing to prolonged repair cycle times. Simultaneously, lingering global supply-chain disruptions and tariff-related friction have inflated parts prices, compounding claims severity and adding volatility to repair cost forecasts. Players now face difficult trade-offs: either pass rising costs onto consumers through premium hikes or absorb them through tighter margins, both of which invite heightened scrutiny from the FCA under its fair pricing framework. These pressures are pushing insurers to prioritise operational streamlining, invest in digital claims automation, and form strategic procurement alliances with OEMs and repair networks. Insurers are also re-evaluating repair triage models and parts sourcing strategies to reduce leakage and protect customer satisfaction.

Other drivers and restraints analyzed in the detailed report include:

- Post-COVID mileage rebound and growing car ownership

- AI-driven claims automation & fraud analytics

- Price-comparison websites intensifying price wars

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Collision/Comprehensive products led with a 60.85% share in 2025, anchoring the UK car insurance market's largest revenue pool. Optional covers such as key-loss, EV battery, and cyber protections, though smaller, are projected to expand at 5.73% CAGR by 2031. Margin pressure within compulsory lines drives insurers to craft ancillary protections that resonate with emerging mobility risks. The FCA's Consumer Duty prompts clearer benefit articulation, steering product design toward measurable value and transparent pricing. Insurers that modularize offerings provide customers with tailored bundles, raising retention and diversified premium streams.

Third-party liability remains a mandated commodity where service responsiveness overrides coverage latitude. Competitive differentiation shifts to claim-time experience, with AI-supported first-notification workflows raising satisfaction scores. As connected-car data feeds broaden risk granularity, the United Kingdom car insurance market sheds one-size-fits-all plans. Companies that quickly convert behavioral insights into responsibly priced optional features will compound growth and enhance customer stickiness.

Personal vehicle policies generated 82.75% of premiums in 2025, underscoring the historic backbone of the United Kingdom car insurance market. Yet e-commerce expansion, fleet electrification mandates, and telematics insights propel Commercial Vehicles to a leading 6.39% CAGR through 2031. Higher average premiums per unit and proactive risk-management cultures lift commercial underwriting economics. Logistics operators deploy connected-fleet dashboards, supplying granular data that allows insurers to price on activity instead of historical proxies.

Personal lines face aggregator-led commoditization, prompting players to harvest cost efficiencies, personalize offers, and broaden value-added services. Meanwhile, last-mile delivery demand accelerates van registrations beyond 2019 levels, enlarging commercial risk pools. The United Kingdom car insurance market is therefore rebalancing: stable but margin-compressed personal lines coexist with technology-rich, faster-growing commercial segments offering scale playbooks for data-savvy insurers.

Complete Report Scope:

- By Coverage

- Third-Party Liability

- Collision / Comprehensive

- Other Optional Covers

- By Application

- Personal Vehicles

- Commercial Vehicles

- By Distribution Channel

- Direct-to-Consumer (DTC)

- Intermediated (includes agents, brokers, bancassurance, and other traditional third-party channels)

- Embedded (insurance sold as an add-on within another purchase journey)

- By Vehicle Powertrain

- Internal-Combustion Engine (ICE)

- Battery-Electric Vehicles (BEV)

- Plug-in Hybrid Vehicles (PHEV)

- Fuel-Cell Electric Vehicles (FCEV)

- By Region

- London

- South East England

- Scotland

- North West England

List of Companies Covered in this Report:

- Admiral Group

- Aviva plc

- Direct Line Group

- LV= General Insurance

- AXA UK

- Hastings Group

- RSA Insurance

- Ageas UK

- Esure

- NFU Mutual

- Zurich Insurance UK

- Allianz Insurance plc

- Tesco Underwriting

- Saga plc

- Co-op Insurance

- Churchill Insurance

- By Miles

- Cuvva

- Swinton Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Telematics-based usage-based insurance adoption

- 4.2.2 Rapid expansion of the UK electric-vehicle parc

- 4.2.3 Post-COVID mileage rebound & growing car ownership

- 4.2.4 Stricter enforcement of compulsory motor insurance

- 4.2.5 OEM-embedded motor insurance partnerships

- 4.2.6 AI-driven claims automation & fraud analytics

- 4.3 Market Restraints

- 4.3.1 Repair-cost and parts-inflation squeezing margins

- 4.3.2 Price-comparison websites intensifying price wars

- 4.3.3 Data-privacy pushback limiting telematics uptake

- 4.3.4 High EV-battery repair costs increasing risk load

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Insights on Consumer Behaviour Analysis

5 Market Size & Growth Forecasts

- 5.1 By Coverage

- 5.1.1 Third-Party Liability

- 5.1.2 Collision / Comprehensive

- 5.1.3 Other Optional Covers

- 5.2 By Application

- 5.2.1 Personal Vehicles

- 5.2.2 Commercial Vehicles

- 5.3 By Distribution Channel

- 5.3.1 Direct-to-Consumer (DTC)

- 5.3.2 Intermediated (includes agents, brokers, bancassurance, and other traditional third-party channels)

- 5.3.3 Embedded (insurance sold as an add-on within another purchase journey)

- 5.4 By Vehicle Powertrain

- 5.4.1 Internal-Combustion Engine (ICE)

- 5.4.2 Battery-Electric Vehicles (BEV)

- 5.4.3 Plug-in Hybrid Vehicles (PHEV)

- 5.4.4 Fuel-Cell Electric Vehicles (FCEV)

- 5.5 By Region

- 5.5.1 London

- 5.5.2 South East England

- 5.5.3 Scotland

- 5.5.4 North West England

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Admiral Group

- 6.4.2 Aviva plc

- 6.4.3 Direct Line Group

- 6.4.4 LV= General Insurance

- 6.4.5 AXA UK

- 6.4.6 Hastings Group

- 6.4.7 RSA Insurance

- 6.4.8 Ageas UK

- 6.4.9 Esure

- 6.4.10 NFU Mutual

- 6.4.11 Zurich Insurance UK

- 6.4.12 Allianz Insurance plc

- 6.4.13 Tesco Underwriting

- 6.4.14 Saga plc

- 6.4.15 Co-op Insurance

- 6.4.16 Churchill Insurance

- 6.4.17 By Miles

- 6.4.18 Cuvva

- 6.4.19 Swinton Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment