PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072530

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072530

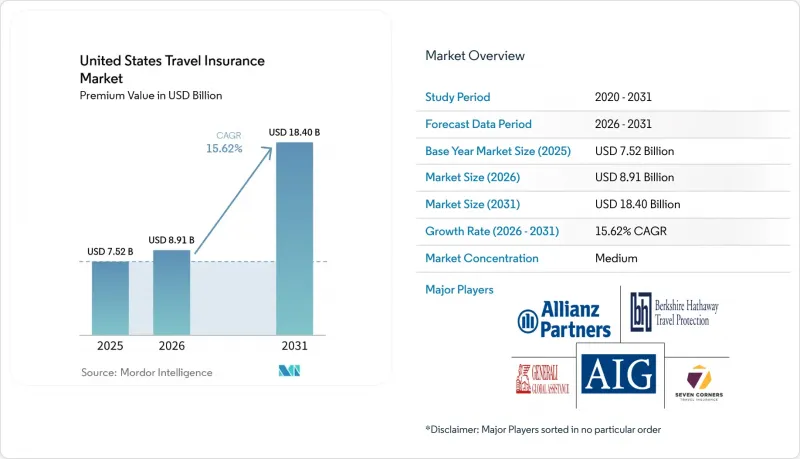

United States Travel Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states travel insurance market size in terms of premium value is projected to expand from USD 7.52 billion in 2025 and USD 8.91 billion in 2026 to USD 18.40 billion by 2031, registering a CAGR of 15.62% between 2026 to 2031.

This report is Segmented by Cover Type (Single-Trip, Annual Multi-Trip, Long/Extended Stay), Benefit (Medical, Trip Cancellation, Baggage and More), Distribution Channel (Direct, Insurance Intermediaries, Banks, Online Aggregators, Travel Agencies, Airlines and Cruise Lines), End Users (Senior Citizens, Family Travellers, and More), and Region. The Market Forecasts are Provided in Terms of Value (USD).

United States Travel Insurance Market Trends and Insights

Surge in Outbound U.S. Leisure Travel

Outbound leisure travel from the U.S. has rebounded, surpassing pre-pandemic levels. Notably, 50% of these travelers are now opting for travel insurance, a significant rise from just 20% in 2020. Furthermore, 15% of travelers are insuring every trip. Financial-loss protection stands out as the primary reason for this coverage, highlighted by 41% of buyers. Younger generations are at the forefront of this trend: 60% of Gen Z and 54% of Millennials are purchasing travel insurance. In contrast, only 45% of Gen X and 43% of Boomers are doing the same, underscoring a generational shift that could reshape long-term demand. Moreover, airlines, cruise lines, and tour operators are witnessing a notable uptick in insurance attachment rates, especially when coverage is bundled during the booking process, bolstering the market's growth trajectory.

Embedded Cover via OTAs & Airlines

The seamless integration of travel insurance into the booking process especially via online travel agencies (OTAs) and airlines has made it notably easier for occasional travelers to opt for coverage. Consequently, 45% of consumers now favor buying insurance directly from their travel providers, moving away from the limited benefits of credit card offerings. Real-time, personalized pricing through API-driven platforms has heightened relevance and boosted conversion rates. In a significant move, PassportCard acquired Pattern in May 2025, propelling the global adoption of embedded insurance solutions among OTAs. As more airlines roll out integrated coverage, insurers are not just increasing customer uptake but are also aiding carriers in turning insurance into a lucrative ancillary revenue stream, further propelling the growth of the U.S. travel insurance market.

Credit-Card Benefits Suppressing Standalone Sales

Premium cards such as Chase Sapphire Reserve include trip-cancellation limits up to USD 10,000 and delay reimbursement of USD 500, fostering a "free coverage" mindset. Yet exclusions for pre-existing conditions, medical costs, and extended trip lengths dilute actual protection. Insurers counter by marketing "top-up" products that fill card gaps and by highlighting claims-service advantages over bank administrators. Consumer education is repositioning credit-card coverage as a baseline rather than a substitute, slowly easing the drag on the US travel insurance market.

Other drivers and restraints analyzed in the detailed report include:

- Extreme Weather Driving Demand

- Medicare Gaps Abroad Push Retirees Toward Specialized Coverage

- COVID-19 Litigation Eroding Trust

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-trip protection held 60.85% US travel insurance market share in 2025 as occasional vacationers favored one-off policies for budget clarity. Purchases spiked during the "revenge-travel" wave, reinforcing the segment's prominence. However, annual plans are expanding at a 15.94% CAGR, above the overall US travel insurance market. Demand originates from frequent flyers, digital nomads, and families seeking administrative ease over multiple journeys. Providers tempt customers with unlimited-trip scopes, concierge services, and bundled medical telehealth, eroding the legacy cost gap. Some carriers tier annual packages to align premiums with trip frequency, broadening appeal while defending profitability.

Travel patterns signal continued convergence. Corporate road-warriors, now pairing business and leisure stays, discover that annual coverage reimburses both trip types. Remote work visas fuel longer overseas stints, nudging travelers toward plans that accommodate extended calendar spans without repeat paperwork. The eventual equilibrium may see single-trip policies remain the entry point while annual products capture loyalty among upwardly mobile demographics, reshaping both retention economics and the US travel insurance market size at segment level.

Emergency treatment claims accounted for 26.9% of 2025 submissions, with average payouts at USD 1,654. The figure underscores travelers' primary fear: unexpected healthcare bills abroad. Among retirees, awareness of Medicare's overseas void further concentrates interest in high-limit medical benefits. Trip cancellation and interruption coverages follow closely, representing more than 40% of aggregate claims as travelers hedge prepaid, non-refundable costs. In both categories, simple wording and instant-claim apps differentiate carriers in the competitive field.

Technology catalyzes new sub-features. Parametric flight-delay add-ons trigger automatic wallet credits when airline data confirm Schedule-B breaches, shrinking claims cycles to minutes. Cybersecurity riders protect personal data and devices, reflecting the modern traveler's reliance on connected gadgets. Innovation within core benefit types expands perceived value and elevates policy penetration, extending the US travel insurance market size across broadening demand curves.

Complete Report Scope:

- By Insurance Cover Type

- Single-Trip Travel Insurance

- Annual Multi-Trip Travel Insurance

- Long-Stay / Extended-Stay Travel Insurance

- By Coverage (Benefit) Type

- Medical & Emergency Care Expense

- Trip Cancellation & Interruption

- Baggage & Personal Effects Loss

- Flight / Travel Delay

- Other Add-On Coverage (Adventure Sports, Rental Car, etc.)

- By Distribution Channel

- Insurance Companies (Direct)

- Insurance Intermediaries & Agents

- Banks & Credit Unions

- Online Aggregators & Comparison Portals

- Travel Agencies & OTAs

- Airlines & Cruise Lines (Embedded)

- By End User Type

- Senior Citizens (65+)

- Family Travelers

- Business Travelers

- Student / Educational Travelers

- Solo Backpackers & Adventure Travelers

- By Geography

- Northeast

- Midwest

- South

- West

List of Companies Covered in this Report:

- Allianz Partners (Allianz Global Assistance)

- American International Group Inc. (AIG Travel Guard)

- Berkshire Hathaway Travel Protection

- Seven Corners Inc.

- Generali Global Assistance

- AXA Assistance USA

- IMG Global

- Travelex Insurance Services

- Nationwide Mutual Insurance Co.

- USI Affinity Travel Insurance Services

- Tokio Marine HCC - Medical Insurance Services

- Travel Insured International

- WorldTrips

- Arch RoamRight

- InsureMyTrip (Squaremouth Holdings)

- Allianz Partners USA (Jefferson Insurance Co.)

- AXA Equitable Life Insurance Co.

- Aviva Travel Insurance (U.S. division)

- MetLife Travel Insurance

- American Express Travel Insurance

- Chubb Travel Protection

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in outbound U.S. leisure travel

- 4.2.2 Embedded cover sold via U.S. OTAs & airlines accelerating adoption

- 4.2.3 Extreme weather-related trip disruption driving medical & cancellation cover demand

- 4.2.4 Medicare gaps abroad push retirees toward specialized medical cover

- 4.2.5 Premium credit-card "top-up" awareness expanding voluntary uptake

- 4.2.6 Affluent Baby-Boomer retirements boosting senior travel frequency

- 4.3 Market Restraints

- 4.3.1 Credit-card benefit perception suppressing standalone policy sales

- 4.3.2 Fragmented state insurance regulation inflates compliance cost

- 4.3.3 Price-sensitive >70-year travelers deterred by high premiums

- 4.3.4 COVID-19 claim litigation eroding consumer trust in policy wording

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Supplier Power

- 4.6.2 Buyer Power

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Insurance Cover Type

- 5.1.1 Single-Trip Travel Insurance

- 5.1.2 Annual Multi-Trip Travel Insurance

- 5.1.3 Long-Stay / Extended-Stay Travel Insurance

- 5.2 By Coverage (Benefit) Type

- 5.2.1 Medical & Emergency Care Expense

- 5.2.2 Trip Cancellation & Interruption

- 5.2.3 Baggage & Personal Effects Loss

- 5.2.4 Flight / Travel Delay

- 5.2.5 Other Add-On Coverage (Adventure Sports, Rental Car, etc.)

- 5.3 By Distribution Channel

- 5.3.1 Insurance Companies (Direct)

- 5.3.2 Insurance Intermediaries & Agents

- 5.3.3 Banks & Credit Unions

- 5.3.4 Online Aggregators & Comparison Portals

- 5.3.5 Travel Agencies & OTAs

- 5.3.6 Airlines & Cruise Lines (Embedded)

- 5.4 By End User Type

- 5.4.1 Senior Citizens (65+)

- 5.4.2 Family Travelers

- 5.4.3 Business Travelers

- 5.4.4 Student / Educational Travelers

- 5.4.5 Solo Backpackers & Adventure Travelers

- 5.5 By Geography

- 5.5.1 Northeast

- 5.5.2 Midwest

- 5.5.3 South

- 5.5.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Allianz Partners (Allianz Global Assistance)

- 6.4.2 American International Group Inc. (AIG Travel Guard)

- 6.4.3 Berkshire Hathaway Travel Protection

- 6.4.4 Seven Corners Inc.

- 6.4.5 Generali Global Assistance

- 6.4.6 AXA Assistance USA

- 6.4.7 IMG Global

- 6.4.8 Travelex Insurance Services

- 6.4.9 Nationwide Mutual Insurance Co.

- 6.4.10 USI Affinity Travel Insurance Services

- 6.4.11 Tokio Marine HCC - Medical Insurance Services

- 6.4.12 Travel Insured International

- 6.4.13 WorldTrips

- 6.4.14 Arch RoamRight

- 6.4.15 InsureMyTrip (Squaremouth Holdings)

- 6.4.16 Allianz Partners USA (Jefferson Insurance Co.)

- 6.4.17 AXA Equitable Life Insurance Co.

- 6.4.18 Aviva Travel Insurance (U.S. division)

- 6.4.19 MetLife Travel Insurance

- 6.4.20 American Express Travel Insurance

- 6.4.21 Chubb Travel Protection

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment