PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073578

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073578

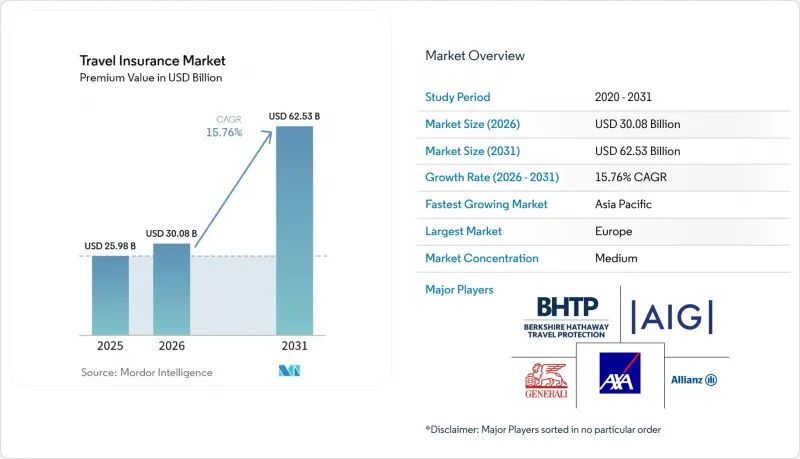

Travel Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the travel insurance market size in terms of premium value is projected to expand from USD 25.98 billion in 2025 and USD 30.08 billion in 2026 to USD 62.53 billion by 2031, registering a CAGR of 15.76% between 2026 to 2031.

This report is Segmented by Insurance Cover Type (Single Trip, Annual Multi-Trip, and More), Distribution Channel (Insurance Intermediaries, Insurance Companies (Direct), and More), End-User Type (Family Travelers, Business Travelers, Senior Citizens, Students, Others), and Geography (North America, South America, Europe, Middle East and Africa, Asia-Pacific). Market Forecasts are in Value (USD).

Global Travel Insurance Market Trends and Insights

Rising Global Tourism and Increased Travel Frequency

International tourism has fully rebounded, carrying strong momentum into the current year, driven by robust cross-border travel and resilient consumer spending in major source markets. This recovery has expanded the base of insured travelers across both leisure and corporate segments. Growing travel volumes align with government projections of continued increases in international arrivals, supporting the broader adoption of travel insurance at the point of booking and through financial services channels. At the same time, elevated load factors and occasional operational constraints are raising the risk of travel disruptions, encouraging more travelers to seek policies that cover delays and interruptions to mitigate financial losses. Similar trends are evident in Asia-Pacific and the Middle East, where infrastructure improvements, resumed flight capacity, and sustained demand are enhancing growth prospects for carriers that tailor benefits to local travel patterns.

Post-Pandemic Boom in Experiential Tourism Across Asia-Pacific

Asia-Pacific tourism is nearing full recovery, with international visitor flows in early 2025 approaching pre-pandemic levels. In 2024, the region welcomed around 648 million international arrivals, reaching nearly 92 % of 2019 levels, while the first half of 2025 alone recorded approximately 296 million arrivals, showing continued growth. The region's diverse destinations, particularly those offering cultural, natural, and experiential attractions, are drawing strong numbers of international travelers[2]. This growth is supported by expanding air connectivity, affordable travel options through low-cost carriers, and the emergence of new source markets, encouraging travelers to embark on more frequent and multi-destination journeys. The shift toward experiential travel, with varied activities, transfers, and complex itineraries, heightens the risk of disruptions from flight delays to health or logistical challenges, making comprehensive travel insurance increasingly essential. The combination of high travel volumes, complex itineraries, and spontaneous travel patterns is driving steady demand for coverage across distribution channels in the Asia-Pacific region.

Rising Fraudulent Claims Pressuring APAC Loss Ratios

Fraud risks in Asia-Pacific are evolving toward digital channels, with data showing that online fraud accounts for a larger share of total losses as criminals exploit remote onboarding and cross-border anonymity. The True Cost of Fraud Study indicates that each Singapore dollar lost to fraud imposes a multiplier of 3.95 when operational, legal, and recovery costs are included, which raises the effective break-even premium thresholds for carriers seeking to maintain stable loss ratios. For insurers active in APAC corridors, this pressure translates into stronger identity verification, device fingerprinting, and behavioral analytics to catch anomalies at the new-account stage, where losses tend to be highest. Parametric triggers for flight delays and weather events help cut opportunistic claims because they rely on independent data sources rather than claimant documentation, which reduces disputes and shortens settlement cycles. Balancing anti-fraud controls with a low-friction customer experience remains critical because high-touch authentication can deter legitimate buyers, especially when purchase windows are short. Over time, the spread of standardized data-sharing and consent frameworks across major markets can improve verification and underwriting precision without slowing sales.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Insurance Requirements for Visas and Entry

- Technological Advancements and Digital Distribution

- High Cost of Comprehensive Travel Insurance and Price Sensitivity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-trip insurance held 46.47% of the travel insurance market share in 2025, which reflects the continued importance of one-off leisure journeys and family vacations where buyers prefer clear benefits and predictable costs. Long-stay or extended-stay policies are projected to grow at 19.84% through 2031, supported by remote work patterns and traveler profiles that require multi-month medical and assistance coverage across jurisdictions, including Indian professionals on extended overseas assignments. The travel insurance market has responded by modularizing benefits around core medical, delay, interruption, and baggage, which improves price-to-value alignment for buyers who do not need full cancellation protection on every trip. Visa-linked medical minimums in the Schengen Area are shaping product baselines and often lead travelers to select higher limits and evacuation options for added peace of mind. For Indian travelers, extended-stay coverage has gained relevance for student, project, and remote work stays that exceed 90 days, where continuous medical support and multilingual assistance become essential.

Annual multi-trip plans serve frequent flyers who prefer continuous protection with streamlined purchase and claims, and they are increasingly configured with flexible add-ons that can be switched on ahead of each journey. Parametric options for flight delays and defined weather events are now embedded into some multi-trip and single-trip plans, and they unlock instant payments for qualifying disruptions based on verifiable data triggers. The travel insurance industry has also focused on cruise benefits and high-value equipment riders for cameras or laptops, which suit content creators and business travelers with sensitive gear. Indian outbound corridors to Europe, North America, and East Asia are seeing broader plan menus, including medical-only and evacuation-focused options for travelers who already receive some cancellation benefits via bank cards. Over the forecast period, extended-stay and annual products should capture more renewals as travelers internalize the convenience of continuous coverage and a single claims experience for multiple trips.

Complete Report Scope:

- Segmentation by Insurance Cover Type

- Single Trip

- Annual Multi-Trip

- Long-Stay / Extended-Stay

- Specialized Policies

- Flight-Delay Insurance

- Cancel-for-Any-Reason (CFAR)

- Adventure-Sports Coverage

- Segmentation by Distribution Channel

- Insurance Intermediaries

- Insurance Companies (Direct)

- Banks & Bancassurance

- Travel Agents & Tour Operators

- Online Aggregators / Comparison Portals

- Others (Airlines & Online Travel Agencies, Super-Apps & Digital Wallets)

- Segmentation by End-User / Traveller Type

- Family Travellers

- Business Travellers

- Senior Citizens

- Students

- Others (Remote Workers, Backpackers, Group Travellers)

- Segmentation by Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Peru

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East And Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Southeast Asia

- Singapore

- Thailand

- Indonesia

- Vietnam

- Philippines

- Malaysia

- Rest of Southeast Asia

- Rest of Asia-Pacific

- North America

Geography Analysis

Europe retained leadership with 41.87% in 2025, reflecting a long-standing base of insured inbound and outbound travel underpinned by clear regulatory guardrails. The Schengen Area's medical coverage requirement for many non-EU visitors supports steady policy uptake, and the planned late-2026 ETIAS start is expected to keep documentation and insurance top of mind for visa-exempt travelers. Embedded distribution remains important at airline, OTA, and card-issuer touchpoints, which helps maintain scale advantages for large carriers and assistance networks in the travel insurance market. India-to-Europe corridors remain a core flow for leisure, education, and business, underscoring the relevance of plans that meet Schengen proof-of-coverage thresholds with sufficient medical and evacuation limits. With product menus that favor modularity and faster payouts, Europe's incumbents and partners are positioned to defend share while adapting to digital buyer preferences across segments.

Asia-Pacific is the fastest-growing region with a projected 19.37% CAGR through 2031, supported by recovering outbound travel from China and robust inbound demand in Japan. Regional seat capacity and low-cost carrier activity have helped pull traffic closer to pre-pandemic baselines, and this underwrites wider policy uptake for medical, delay, and baggage protection in the travel insurance market. Chinese outbound travelers are prioritizing safety and weather resilience, and stated purchase intentions for insurance are strong, which favors plans that combine medical benefits with parametric features. India's data-protection framework reinforces privacy and consent rules for cross-border underwriting, guiding how carriers and partners handle personal data and analytics across acquisition and claims. As Asian routes expand and traveler profiles diversify, product design and claims logistics will be key levers for retention in India and neighboring outbound markets.

North and South America show mixed dynamics that still contribute meaningful growth and product innovation. Parametric flight-delay coverage is scaling through integration with booking flows and mobile apps, which aligns benefits with real travel disruptions and accelerates claims. Brazil's market shows steady premium growth on rising regional travel, and industry association updates indicate higher consumer uptake during peak periods, which supports continued distribution investment in Latin channels. Indian leisure and VFR travelers to North America are a consistent use case for comprehensive plans due to medical cost differentials, which anchor demand for higher-limit products with evacuation and repatriation. Together, these patterns reinforce a broad geographic base for the travel insurance market with region-specific triggers for adoption across product types.

- Allianz SE

- American International Group (AIG)

- AXA SA

- Zurich Insurance Group Ltd.

- Assicurazioni Generali SpA

- Berkshire Hathaway Travel Protection

- Chubb Ltd.

- Seven Corners Inc.

- Travelex Insurance Services

- Tokio Marine Holdings Inc.

- Ping An Insurance (Group) Co.

- Mapfre SA (InsureandGo)

- Aviva plc

- AIA Group Ltd.

- TATA AIG General Insurance Co.

- Bajaj Allianz General Insurance Co.

- Sompo Japan Nipponkoa Holdings

- CSA Travel Protection (Generali Global Assistance)

- HDFC ERGO General Insurance Co.

- MetLife Inc. (Business Travel Accident)

- ERGO Group AG (Munich Re)

- USI Affinity

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Tourism and Increased Travel Frequency

- 4.2.2 Post-Pandemic Boom in Experiential Tourism Across Asia

- 4.2.3 Mandatory Insurance Requirements for Visas and Entry

- 4.2.4 Technological Advancements and Digital Distribution

- 4.2.5 Parametric Flight-Delay Products Scaling in North America

- 4.3 Market Restraints

- 4.3.1 Rising Fraudulent Claims Pressuring APAC Loss Ratios

- 4.3.2 Lack of Consumer Understanding & Perceived Value

- 4.3.3 High Cost of Comprehensive Travel Insurance & Price Sensitivity

- 4.3.4 Data-Privacy Rules (GDPR, PDPA) Hindering Cross-Border Underwriting

- 4.4 Value Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 Segmentation by Insurance Cover Type

- 5.1.1 Single Trip

- 5.1.2 Annual Multi-Trip

- 5.1.3 Long-Stay / Extended-Stay

- 5.1.4 Specialized Policies

- 5.1.4.1 Flight-Delay Insurance

- 5.1.4.2 Cancel-for-Any-Reason (CFAR)

- 5.1.4.3 Adventure-Sports Coverage

- 5.2 Segmentation by Distribution Channel

- 5.2.1 Insurance Intermediaries

- 5.2.2 Insurance Companies (Direct)

- 5.2.3 Banks & Bancassurance

- 5.2.4 Travel Agents & Tour Operators

- 5.2.5 Online Aggregators / Comparison Portals

- 5.2.6 Others (Airlines & Online Travel Agencies, Super-Apps & Digital Wallets)

- 5.3 Segmentation by End-User / Traveller Type

- 5.3.1 Family Travellers

- 5.3.2 Business Travellers

- 5.3.3 Senior Citizens

- 5.3.4 Students

- 5.3.5 Others (Remote Workers, Backpackers, Group Travellers)

- 5.4 Segmentation by Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Peru

- 5.4.2.4 Chile

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Middle East And Africa

- 5.4.4.1 United Arab Emirates

- 5.4.4.2 Saudi Arabia

- 5.4.4.3 South Africa

- 5.4.4.4 Nigeria

- 5.4.4.5 Rest of Middle East & Africa

- 5.4.5 Asia-Pacific

- 5.4.5.1 China

- 5.4.5.2 India

- 5.4.5.3 Japan

- 5.4.5.4 South Korea

- 5.4.5.5 Australia

- 5.4.5.6 Southeast Asia

- 5.4.5.6.1 Singapore

- 5.4.5.6.2 Thailand

- 5.4.5.6.3 Indonesia

- 5.4.5.6.4 Vietnam

- 5.4.5.6.5 Philippines

- 5.4.5.6.6 Malaysia

- 5.4.5.6.7 Rest of Southeast Asia

- 5.4.5.7 Rest of Asia-Pacific

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Allianz SE

- 6.4.2 American International Group (AIG)

- 6.4.3 AXA SA

- 6.4.4 Zurich Insurance Group Ltd.

- 6.4.5 Assicurazioni Generali SpA

- 6.4.6 Berkshire Hathaway Travel Protection

- 6.4.7 Chubb Ltd.

- 6.4.8 Seven Corners Inc.

- 6.4.9 Travelex Insurance Services

- 6.4.10 Tokio Marine Holdings Inc.

- 6.4.11 Ping An Insurance (Group) Co.

- 6.4.12 Mapfre SA (InsureandGo)

- 6.4.13 Aviva plc

- 6.4.14 AIA Group Ltd.

- 6.4.15 TATA AIG General Insurance Co.

- 6.4.16 Bajaj Allianz General Insurance Co.

- 6.4.17 Sompo Japan Nipponkoa Holdings

- 6.4.18 CSA Travel Protection (Generali Global Assistance)

- 6.4.19 HDFC ERGO General Insurance Co.

- 6.4.20 MetLife Inc. (Business Travel Accident)

- 6.4.21 ERGO Group AG (Munich Re)

- 6.4.22 USI Affinity

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment