PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072553

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072553

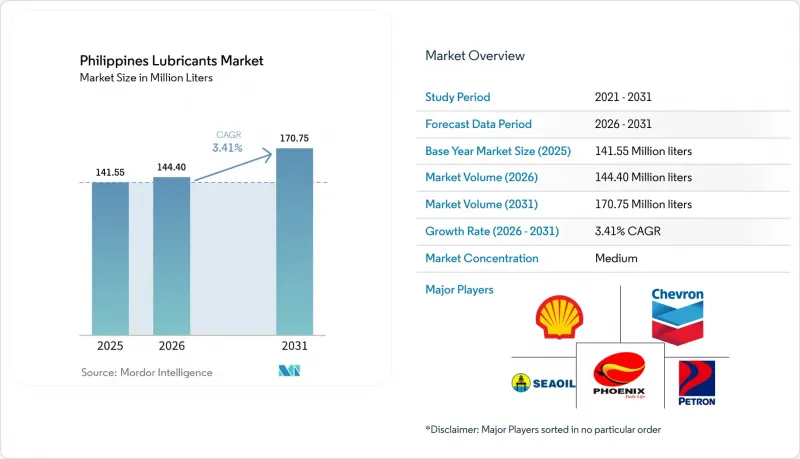

Philippines Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the philippines lubricants market size was valued at 141.55 million liters in 2025 and is estimated to grow from 144.40 million liters in 2026 to reach 170.75 million liters by 2031, at a CAGR of 3.41% during the forecast period (2026-2031).

This report is Segmented by Product Type (Automotive Engine Oil, Industrial Engine Oil, Greases, Metalworking Fluids, Turbine Oil, and More), End-User Industry (Automotive, Marine, Aerospace, Heavy Equipment, and Industrial), and Base Stock Type (Mineral Oil-Based Lubricants, Synthetic Lubricants, Semi-Synthetic Lubricants, and More). The Market Forecasts are Provided in Terms of Volume (liters).

Philippines Lubricants Market Trends and Insights

Increasing Construction Mega-Projects (Build-Better-More)

The PHP 1.545 trillion (USD 26.6 billion) outlay in 2024, equal to 5.8% of GDP, underwrites large road, rail, and bridge builds that keep excavators, cranes, and concrete mixers running in punishing duty cycles. Equipment owners shorten drain intervals, inflating demand for high-zinc hydraulic fluids and extreme-pressure greases. Projects such as the Bataan-Cavite Interlink Bridge and Metro Manila Subway require thousands of heavy machines that rely on Group II base-oil blends for soot control. Yet capital-outlay pauses before elections pared spending to 4.2% of GDP in Q1-Q3 2025, swinging lubricant orders sharply from quarter to quarter. Suppliers with multi-regional depots, notably Shell's 10 warehouses and Petron's 21,000-outlet network, are best placed to flex inventories. Power projects tied to new rail lines also lift turbine-oil pull-through, reinforcing the premium segment.

Industrial Digitalization Boosting Predictive-Maintenance Grade Lubricants

Government Industry 4.0 programs and the Advanced Manufacturing Center spur adoption of sensor-equipped machinery that favors longer-life synthetic hydraulics. Only 14.9% of factories had deployed IoT maintenance by 2024, but early movers in electronics and metalworking already specify OEM-approved zinc-free oils rated beyond 10,000 hours in ASTM D943 testing. Chevron Clarity and equivalents command sizeable premiums and often bundle oil-analysis services. Small and medium manufacturers still default to mineral-based AW 68 fluids, so vendors such as Shell push mobile oil-analysis vans to up-sell synthetics, a model that hinges on scaling technical staff as much as stock volume.

Growing Penetration of Electric and Hybrid Vehicles

EV registrations jumped from 13,000 in 2023 to 21,000 by mid-2024 on the back of import-duty and VAT exemptions under RA 11697, and the government targets a 50% EV sales mix by 2040. Charging stations surpassed 800 sites in 2024, anchored by Meralco, Shell Recharge, and AC Energy. Hybrids still use engine oil but at roughly 60-70% of internal-combustion volume; full battery EVs eliminate it. Suppliers hedge by launching specialized dielectric-cooling fluids, yet the transition is expected to shave 0.6 percentage points off the Philippines lubricants market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of Ride-Hailing and Motorcycle Fleets Demanding High-Temperature 4T Oils

- OEM-Backed Low-Viscosity Synthetic Oils with Extended-Warranty Pull-Through

- Proliferation of Counterfeit/Adulterated Lubricants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automotive Engine Oil, while still accounting for 33.78% of 2025 volume, faces a gradually flattening curve as hybrids lengthen drain intervals. Transmission fluids benefit from automatic-transmission uptake in passenger cars, now 48% of 2024 sales. Greases, metalworking, turbine, and transformer oils remain niche but margin-rich pockets, reinforcing supplier moves toward value-added industrial blends. The Philippines lubricants market size for Industrial Engine Oil is projected to grow faster than any other product family through 2031. Industrial Engine Oil is poised to outpace automotive grades at a 3.15% CAGR, fueled by 29,853 MW of installed power capacity and around-the-clock genset operations that mandate high-soot-load formulations.

Smaller players must pick sides: high-volume, low-margin automotive oils vulnerable to counterfeits, or low-volume, high-spec industrial blends that require technical support. SEAOIL's strategy spans both, leveraging 700+ stations for retail pull while marketing ISO VG 150-320 gear oils to crushing plants.

Complete Report Scope:

- By Product Type

- Automotive Engine Oil

- Industrial Engine Oil

- Transmission Fluids

- Gear Oil

- Brake Fluids

- Hydraulic Fluids

- Greases

- Process Oil (Including Rubber Process Oil and White Oil)

- Metalworking Fluids

- Turbine Oil

- Transformer Oil

- Other Product Types

- By End-user Industry

- Automotive

- Passenger Vehicles

- Commercial Vehicles

- Two-Wheelers

- Marine

- Aerospace

- Heavy Equipment

- Construction

- Mining

- Agriculture

- Industrial

- Power Generation

- Metallurgy and Metalworking

- Textiles

- Oil and Gas

- Other End-Use Industries

- Automotive

- By Base Stock Type

- Mineral Oil-Based Lubricants

- Synthetic Lubricants

- Semi-Synthetic Lubricants

- Bio-Based Lubricants

List of Companies Covered in this Report:

- BP plc

- Chevron Corporation

- China Petroleum & Chemical Corporation

- Exxon Mobil Corporation

- FUCHS

- Gulf Oil International

- Idemitsu Kosan (ENEOS)

- Liqui Moly

- Motul

- Petron Corporation

- PETRONAS Lubricant International

- Phoenix Petroleum

- PTT Lubricants

- Rainchem International Inc.

- Repsol

- Saudi Arabian Oil Co.

- SEAOIL Philippines, Inc.

- Shell plc

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing construction mega-projects (Build-Better-More)

- 4.2.2 Industrial digitalization boosting predictive-maintenance grade lubricants

- 4.2.3 Rapid growth of ride-hailing and motorcycle fleets demanding high-temperature 4T oils

- 4.2.4 OEM-backed low-viscosity synthetic oils with extended-warranty pull-through

- 4.2.5 E-commerce live-selling and quick-lube bay expansion widening retail access

- 4.3 Market Restraints

- 4.3.1 Growing penetration of electric and hybrid vehicles

- 4.3.2 Proliferation of counterfeit/adulterated lubricants

- 4.3.3 Tightening used-oil circular-economy compliance costs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Framework

- 4.6 End-User Trends

- 4.6.1 Automotive Industry

- 4.6.2 Manufacturing Industry

- 4.6.3 Power Generation Industry

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Automotive Engine Oil

- 5.1.2 Industrial Engine Oil

- 5.1.3 Transmission Fluids

- 5.1.4 Gear Oil

- 5.1.5 Brake Fluids

- 5.1.6 Hydraulic Fluids

- 5.1.7 Greases

- 5.1.8 Process Oil (Including Rubber Process Oil and White Oil)

- 5.1.9 Metalworking Fluids

- 5.1.10 Turbine Oil

- 5.1.11 Transformer Oil

- 5.1.12 Other Product Types

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.1.1 Passenger Vehicles

- 5.2.1.2 Commercial Vehicles

- 5.2.1.3 Two-Wheelers

- 5.2.2 Marine

- 5.2.3 Aerospace

- 5.2.4 Heavy Equipment

- 5.2.4.1 Construction

- 5.2.4.2 Mining

- 5.2.4.3 Agriculture

- 5.2.5 Industrial

- 5.2.5.1 Power Generation

- 5.2.5.2 Metallurgy and Metalworking

- 5.2.5.3 Textiles

- 5.2.5.4 Oil and Gas

- 5.2.5.5 Other End-Use Industries

- 5.2.1 Automotive

- 5.3 By Base Stock Type

- 5.3.1 Mineral Oil-Based Lubricants

- 5.3.2 Synthetic Lubricants

- 5.3.3 Semi-Synthetic Lubricants

- 5.3.4 Bio-Based Lubricants

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 BP plc

- 6.4.2 Chevron Corporation

- 6.4.3 China Petroleum & Chemical Corporation

- 6.4.4 Exxon Mobil Corporation

- 6.4.5 FUCHS

- 6.4.6 Gulf Oil International

- 6.4.7 Idemitsu Kosan (ENEOS)

- 6.4.8 Liqui Moly

- 6.4.9 Motul

- 6.4.10 Petron Corporation

- 6.4.11 PETRONAS Lubricant International

- 6.4.12 Phoenix Petroleum

- 6.4.13 PTT Lubricants

- 6.4.14 Rainchem International Inc.

- 6.4.15 Repsol

- 6.4.16 Saudi Arabian Oil Co.

- 6.4.17 SEAOIL Philippines, Inc.

- 6.4.18 Shell plc

- 6.4.19 TotalEnergies

7 Market Opportunities & Future Outlook

- 7.1 White-space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs