PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072559

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072559

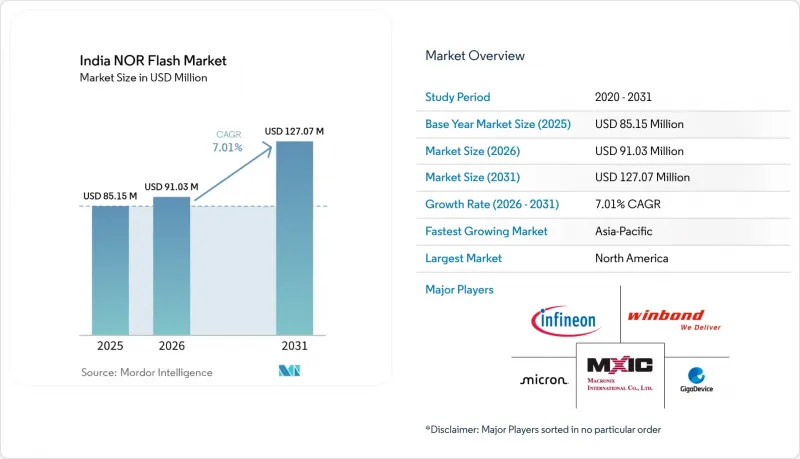

India NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india NOR flash market size is expected to increase from USD 85.15 million in 2025 to USD 91.03 million in 2026 and reach USD 127.07 million by 2031, growing at a CAGR of 6.9% over 2026-2031.

This report is Segmented by Type (Serial NOR Flash, and More), Interface (SPI Single/Dual, and More), Density (2 Mbit and Less, and More), Voltage (3 V Class, and More), End-User Application (Consumer Electronics, Automotive and More), Process Technology Node (65 Nm, 45 Nm, and More), and Packaging Type (WLCSP/CSP, and More). The Market Forecasts are Provided in Terms of Both Value (USD) and Volume (Units).

India NOR Flash Market Trends and Insights

Government PLI and Semiconductor Subsidies Lower Capital Barriers

India Semiconductor Mission 2.0 earmarked INR 1,000 crore (USD 120 million) for new assembly-test-mark-pack sites, while the Electronics Component Manufacturing Scheme approved 22 projects worth INR 41,863 crore (USD 5.02 billion) in January 2026, unlocking private coinvestment and reducing payback hurdles for local EMS companies. Micron's USD 2.75 billion ATMP plant in Sanand signals confidence in foreign direct investment and encourages the formation of an ecosystem around Gujarat.

Secure-Boot Mandates Accelerate Serial NOR Demand

The Bureau of Indian Standards now requires cryptographic signature checks for consumer IoT firmware, pushing OEMs to add dedicated non-volatile code storage that can execute in place.Macronix answered with its ArmorBoot MX76 family up to 1 GB that supports dual 3.0 V and 1.8 V rails for secure-boot smart-meter designs. Early compliance efforts in smart-meter and payment-terminal rollouts ensure sustained design-in activity through 2027.

Lack of Advanced Domestic Fabs Constrains Supply Security

Ten semiconductor ventures cleared under ISM phases are primarily focused on 28 nm logic or compound semiconductors, rather than embedded non-volatile memory. As a result, all sub-55 nm NOR wafers are currently sourced from Taiwan and China, creating a dependency on these regions. This reliance poses a risk, especially during periods of supply chain disruptions or geopolitical tensions. Additionally, a 70% spike in DRAM spot prices during the first quarter of 2026 highlighted how foundry lines often shift priorities during market crunches. Such shifts further exacerbate the challenges for NOR production, leading to extended lead times and constrained supply. This dynamic underscores the vulnerability of the NOR supply chain in the current semiconductor landscape.

Other drivers and restraints analyzed in the detailed report include:

- Automotive ADAS Electronics Need Functional-Safety NOR Flash

- Make in India Smartphone Output Sustains High-Volume Consumption

- Import Tariffs Inflate Memory Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Serial devices held 62.7% share in 2025 and are projected to outgrow the overall India NOR Flash market. These devices offer significant advantages by reducing board area and pin counts compared to parallel parts. This efficiency is particularly valued in applications such as consumer IoT, automotive control units, and industrial PLCs. The compact design and enhanced functionality of serial products make them a preferred choice for modern applications, driving their adoption across various industries.

Parallel NOR, on the other hand, continues to find use in legacy telecom and avionics backplanes that require 16-bit buses. However, vendors are increasingly positioning Octal serial parts as drop-in upgrades for these systems. Octal serial parts match the 400 MB/s throughput of parallel NOR while significantly reducing the footprint. Companies like Winbond, Macronix, and GigaDevice expanded their Octal portfolios during 2025-2026, providing designers with a seamless migration path to serial technology without compromising on bandwidth.

Quad SPI generated 47.6% of interface revenue in 2025. However, Octal and xSPI interfaces are witnessing the fastest growth, driven by JEDEC xSPI 2.0 certification and the increasing demand for high-speed reads of 300-400 MB/s in automotive applications. These advancements are enabling manufacturers to meet the growing need for faster and more efficient memory solutions. The adoption of Octal and xSPI is further supported by their ability to deliver enhanced performance while maintaining compatibility with existing systems.

Leading vendors, such as Infineon with its Semper series and GigaDevice with the GD25LX256E, are integrating xSPI interfaces with features like functional safety and low power consumption. These innovations cater to the evolving requirements of industries like automotive and industrial automation. Meanwhile, Single and Dual SPI interfaces continue to hold relevance in ultra-cost-sensitive applications, such as wearables and sensors, where firmware size remains minimal, and cost efficiency is a priority.

Mid-range 32-64 Mbit devices continued to dominate in 2025, accounting for 28.7% of the market share. These devices remain a preferred choice due to their balance of cost and performance, catering to a wide range of applications. However, the demand for higher-capacity devices is steadily increasing, driven by advancements in technology and the growing need for efficient data storage solutions. AI co-processors, such as Mindgrove's V2600, are a key driver of this trend as they require larger model weights to function effectively.

In the defense sector, avionics systems are increasingly procuring radiation-tolerant parts with capacities of 256 Mbit or more. These components are sourced through contracts with Bharat Electronics, addressing the specific needs of high-reliability applications. While this segment represents a low-volume niche, it remains highly profitable due to the premium pricing of specialized components. The demand for such devices is expected to grow as defense systems continue to evolve and require more advanced memory solutions.

Complete Report Scope:

- By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Mbit and Less NOR

- More than 2-4 Mbit NOR

- More than 4-8 Mbit NOR

- More than 8-16 Mbit NOR

- More than16-32 Mbit NOR

- More than 32-64 Mbit NOR

- More than 64-128 Mbit NOR

- More than 128-256 Mbit NOR

- Greater than 256 Mbit NOR

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V-3.6 V)

- Others -1.2 V Class and Similar

- By End-user Application (Value, Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other End-user Applications

- By Process Technology Node (Value)

- 90 nm and More

- 65 nm

- 55 nm (incl. 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

List of Companies Covered in this Report:

- Winbond Electronics Corporation

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Infineon Technologies AG

- Micron Technology Inc.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Renesas Electronics Corporation

- Wuhan XMC

- Puya Semiconductor (Shanghai) Co. Ltd.

- Samsung Semiconductor

- Alliance Memory

- Zbit Semiconductor

- XTX Technology (Shenzhen) Limited

- Shenzhen Longsys Electronics Co. Ltd.

- Cypress Semiconductor Corporation

- Eon Silicon Solution Inc.

- AMIC Technology Corporation

- Elite Semiconductor Memory Technology Inc.

- Jiangsu Fudan Microelectronics Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Impact of Government-Led PLI and Semiconductor India Subsidies on Capital Expenditures

- 4.2.2 Implementation of Secure-Boot Standards by the Bureau of Indian Standards to Strengthen IoT Device Security

- 4.2.3 Growth in Domestic Automotive ADAS ECU Market

- 4.2.4 Expansion of Smartphone Production under the Make in India Initiative

- 4.2.5 Rising Demand for Octal NOR Flash in Domestic Aerospace and Defense Avionics Modules

- 4.2.6 Adoption of IoT Edge AI Chips Requiring On-Device Code Storage

- 4.3 Market Restraints

- 4.3.1 Limited Indigenous Wafer Fabrication Capabilities for Advanced Sub-55 nm NOR Flash Technology in India

- 4.3.2 Impact of High Import Duties on Landed Costs of NOR Flash versus Southeast Asian Manufacturing Hubs

- 4.3.3 Declining Demand for Discrete NOR Flash Components Due to OEMs' Transition to Multi-Chip Packages

- 4.3.4 Supply Uncertainty from China-Taiwan Geopolitical Risks Affecting Contract Foundry Allocation for Indian Buyers

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing Analysis

- 4.10 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, VOLUME)

- 5.1 By Type (Value, Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Mbit and Less NOR

- 5.3.2 More than 2-4 Mbit NOR

- 5.3.3 More than 4-8 Mbit NOR

- 5.3.4 More than 8-16 Mbit NOR

- 5.3.5 More than16-32 Mbit NOR

- 5.3.6 More than 32-64 Mbit NOR

- 5.3.7 More than 64-128 Mbit NOR

- 5.3.8 More than 128-256 Mbit NOR

- 5.3.9 Greater than 256 Mbit NOR

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65 V-3.6 V)

- 5.4.4 Others -1.2 V Class and Similar

- 5.5 By End-user Application (Value, Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Other End-user Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and More

- 5.6.2 65 nm

- 5.6.3 55 nm (incl. 58 nm)

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Other Packaging Types

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles

- 6.4.1 Winbond Electronics Corporation

- 6.4.2 Macronix International Co. Ltd.

- 6.4.3 GigaDevice Semiconductor Inc.

- 6.4.4 Infineon Technologies AG

- 6.4.5 Micron Technology Inc.

- 6.4.6 Integrated Silicon Solution Inc.

- 6.4.7 Microchip Technology Inc.

- 6.4.8 Renesas Electronics Corporation

- 6.4.9 Wuhan XMC

- 6.4.10 Puya Semiconductor (Shanghai) Co. Ltd.

- 6.4.11 Samsung Semiconductor

- 6.4.12 Alliance Memory

- 6.4.13 Zbit Semiconductor

- 6.4.14 XTX Technology (Shenzhen) Limited

- 6.4.15 Shenzhen Longsys Electronics Co. Ltd.

- 6.4.16 Cypress Semiconductor Corporation

- 6.4.17 Eon Silicon Solution Inc.

- 6.4.18 AMIC Technology Corporation

- 6.4.19 Elite Semiconductor Memory Technology Inc.

- 6.4.20 Jiangsu Fudan Microelectronics Group Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment