PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073230

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073230

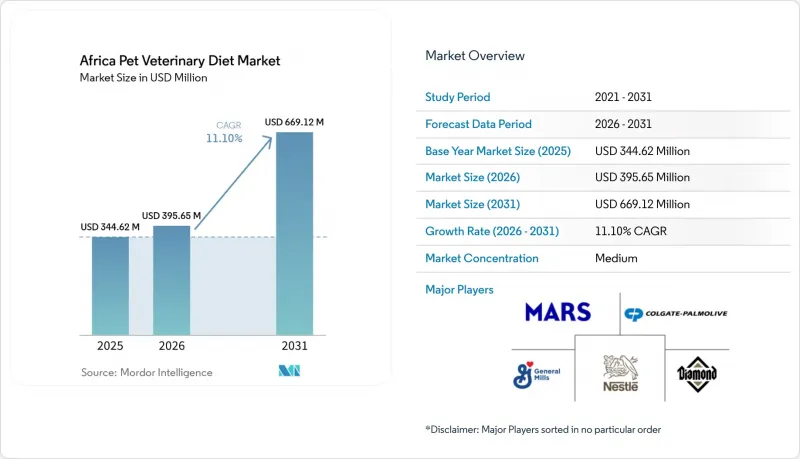

Africa Pet Veterinary Diet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the africa pet veterinary diet market size is projected to grow from USD 344.6 million in 2025 to USD 395.7 million in 2026 and is forecast to reach USD 669.1 million by 2031 at 11.1% CAGR over 2026-2031.

This report is Segmented by Product Type (Diabetes, Digestive Sensitivity, Oral Care Diets, Renal, Urinary Tract Disease, and More), by Pets (Cats, Dogs, and More), by Distribution Channel (Convenience Stores, Online Channel, Specialty Stores, and More), and by Geography (South Africa, Nigeria, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Africa Pet Veterinary Diet Market Trends and Insights

Rising Diagnosis of Chronic Companion-Animal Conditions

Companion animals across Africa are being diagnosed more often with renal disease, urinary problems, digestive sensitivity, skin conditions, and metabolic disorders as formal veterinary access improves. This matters because therapeutic diets typically drive repeat purchases once a condition is identified, making demand steadier than in standard pet food categories. The first official South African pet census, published in May 2026, counted 14.5 million cats and dogs, providing the Africa pet veterinary diet market with a larger, more reliable clinical base than earlier estimates. That pet population is already large enough to support meaningful caseloads in organized practice for renal, urinary, digestive, and weight management. As pet lifespan improves with better general nutrition and care, age-linked conditions such as renal insufficiency and obesity are likely to remain a lasting source of demand for prescription diets.

Expansion of Veterinary Prescription Nutrition Protocols

Veterinary clinics are increasingly treating diet as part of therapy rather than as an optional add-on, which is giving the African pet veterinary diet market a stronger clinical foundation. Royal Canin and the University of Pretoria opened Gauteng's first internationally accredited Cat-Friendly Clinic in July 2025 at the Onderstepoort Veterinary Academic Hospital, raising confidence in feline diagnosis and nutritional management. Clinics trained in accredited settings are more likely to recommend prescription diets earlier in disease management, rather than waiting until the condition is advanced. That gives suppliers with stronger vet education programs a durable advantage that is harder to displace with price cuts alone.

Premium Pricing Limits Mass-Market Adoption

Therapeutic diets still cost 2 to 4 times as much as standard pet food in many African settings, which keeps adoption concentrated among upper-income urban households. South Africa's per-capita pet food expenditure reached USD 9.21 in 2025, but even there, the price gap remains wide for many owners. The problem is not only the headline price, but also the lack of a broad middle tier between premium prescription brands and mass-market feed. That leaves many households treating therapeutic nutrition as a discretionary purchase rather than as part of treatment. The Africa pet veterinary diet market could widen faster if suppliers introduce smaller pack sizes, clinic-linked programs, and more flexible price ladders that reduce trial resistance.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Premium and Preventive Pet Care Spending

- Tele-Veterinary Access and Digital Prescription Workflows

- Low Veterinarian Density Outside Major Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digestive sensitivity captured 17.7% of the product type segment in 2025, making it the largest category in the Africa pet veterinary diet market. This lead reflects how often gastrointestinal issues appear when pets move from informal feeding or home-prepared food to more structured commercial diets. Digestive care also serves as an early entry point into therapeutic nutrition, as owners and veterinarians can often see response patterns more quickly than with some longer-cycle conditions. Renal and urinary tract disease diets held the next most meaningful combined position, supported by stronger recognition that chronic kidney disease and urolithiasis respond well to dietary management. Derma diets and obesity diets remained smaller, but both categories are gaining ground as the Africa pet veterinary diet industry places more weight on non-drug interventions that can support long-term condition control.

Oral care diets are projected to expand at a 9.0% CAGR through 2026 to 2031, making them the fastest-growing product type in the Africa pet veterinary diet market. Diabetes and other veterinary diets are also advancing as feline endocrine and metabolic conditions receive greater attention in practice. A 2026 study, "Beneficial Effects of a Prebiotic-Postbiotic Supplement on Digestive Health and Fecal Microbiota in Dogs and Cats," reported improvements in digestive health and gut microbiota balance among dogs and cats with mild gastrointestinal disturbances, providing stronger clinical validation for microbiome-focused nutritional formulations within the Africa pet veterinary diet industry.

Complete Report Scope:

- By Product Type

- Diabetes

- Digestive Sensitivity

- Oral Care Diets

- Renal

- Urinary Tract Disease

- Derma Diets

- Obesity Diets

- Other Veterinary Diets

- By Pets

- Dogs

- Cats

- Other Pets

- By Distribution Channel

- Convenience Stores

- Online Channel

- Specialty Stores

- Supermarkets and Hypermarkets

- Other Channels

- By Geography

- South Africa

- Nigeria

- Kenya

- Rest of Africa

List of Companies Covered in this Report:

- Mars, Incorporated

- Nestle S.A. (Nestle Purina PetCare Company)

- Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.)

- General Mills, Inc. (Blue Buffalo Pet Products, Inc.)

- Schell & Kampeter, Inc. (Diamond Pet Foods)

- Clearlake Capital Group, L.P. (Wellness Pet Company, Inc.)

- Farmina Pet Foods Holding B.V.

- Agrolimen, S.A. (Affinity Petcare, S.A.)

- PLB International Inc.

- Unicharm Corporation

- Virbac

- Heristo Aktiengesellschaft

- Ultra Pet Company, Inc

- VetsBrands

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising diagnosis of chronic companion-animal conditions

- 4.2.2 Expansion of veterinary prescription nutrition protocols

- 4.2.3 Growth of premium and preventive pet care spending

- 4.2.4 Tele-veterinary access and digital prescription workflows

- 4.2.5 Import liberalization and faster product registration in key markets

- 4.2.6 Microbiome-targeted and functional diet innovation

- 4.3 Market Restraints

- 4.3.1 Premium pricing limits mass-market adoption

- 4.3.2 Low veterinarian density outside major cities

- 4.3.3 Fragmented specialty distribution

- 4.3.4 Limited owner awareness of prescription diet benefits

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product Type

- 5.1.1 Diabetes

- 5.1.2 Digestive Sensitivity

- 5.1.3 Oral Care Diets

- 5.1.4 Renal

- 5.1.5 Urinary Tract Disease

- 5.1.6 Derma Diets

- 5.1.7 Obesity Diets

- 5.1.8 Other Veterinary Diets

- 5.2 By Pets

- 5.2.1 Dogs

- 5.2.2 Cats

- 5.2.3 Other Pets

- 5.3 By Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets and Hypermarkets

- 5.3.5 Other Channels

- 5.4 By Geography

- 5.4.1 South Africa

- 5.4.2 Nigeria

- 5.4.3 Kenya

- 5.4.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Mars, Incorporated

- 6.4.2 Nestle S.A. (Nestle Purina PetCare Company)

- 6.4.3 Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.)

- 6.4.4 General Mills, Inc. (Blue Buffalo Pet Products, Inc.)

- 6.4.5 Schell & Kampeter, Inc. (Diamond Pet Foods)

- 6.4.6 Clearlake Capital Group, L.P. (Wellness Pet Company, Inc.)

- 6.4.7 Farmina Pet Foods Holding B.V.

- 6.4.8 Agrolimen, S.A. (Affinity Petcare, S.A.)

- 6.4.9 PLB International Inc.

- 6.4.10 Unicharm Corporation

- 6.4.11 Virbac

- 6.4.12 Heristo Aktiengesellschaft

- 6.4.13 Ultra Pet Company, Inc

- 6.4.14 VetsBrands

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK