PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073575

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073575

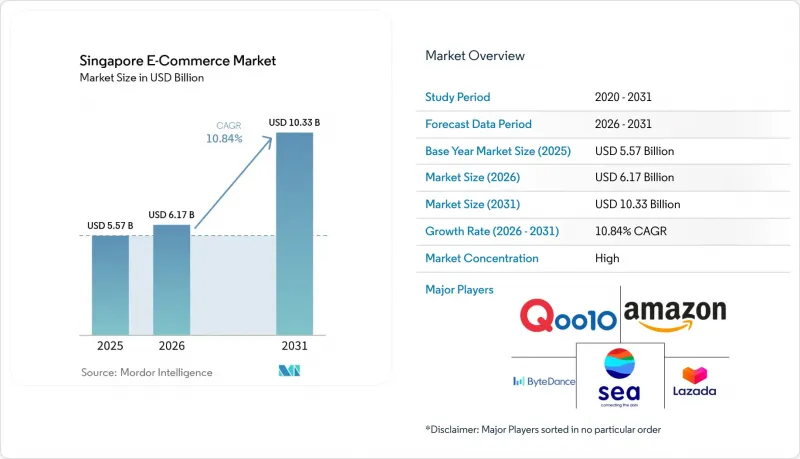

Singapore E-Commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the singapore e-commerce market size in 2026 is estimated at USD 6.17 billion, growing from 2025 value of USD 5.57 billion with 2031 projections showing USD 10.33 billion, growing at 10.84% CAGR over 2026-2031.

This report is Segmented by Business Model (B2B, and B2C), Product Category for B2C E-Commerce (Beauty and More), and Device Type for B2C E-Commerce (Smartphone, Desktop/Laptop, and More). The Market Forecasts are Provided in Terms of Value (USD).

Singapore E-Commerce Market Trends and Insights

Rising Digital-Wallet Penetration

Mobile wallets overtook credit cards in 2024, capturing 45% of transactions as the unified payments entity folded FAST, PayNow, and SGQR into a single governance layer. Gen Z shoppers adopted PayNow at a 68% preference rate once interoperability friction faded, and nearly the entire population is expected to use mobile wallets by end-2025. The SPaN initiative removed technical silos across wallet brands, while Alipay+ integration of six foreign e-wallets deepened inbound tourist spending capabilities. Continuous security upgrades such as DBS Bank's biometric and phishing safeguards sustained user confidence. Together these developments boost shopper frequency, elevate average order values, and sharpen the competitive edge of wallet-first platforms in the Singapore e-commerce market.

Mandatory Nationwide E-Invoice Adoption for B2B (2025)

The Inland Revenue Authority mandated Peppol-based InvoiceNow submissions for GST-registered firms beginning November 2025, shrinking payment cycles from days to hours. Over 28,600 merchants were already connected by 2024 through IMDA's network, and the InvoiceNow Accelerate program waived fees for recently incorporated SMEs. Automating invoice exchange lowers back-office costs and unlocks data visibility that fuels dynamic pricing on B2B marketplaces. The rule also standardizes cross-border transactions, aligning with the Peppol International Invoice to streamline paperwork for China-bound exports now enjoying 94.6% tariff elimination under the upgraded CSFTA. These efficiencies underpin the 12.67% CAGR outlook for B2B trade on the Singapore e-commerce market.

Surge in E-Commerce Scams and Compliance Costs

Police logged 50,376 cyber-fraud cases in 2023, up 49.6% from the prior year, with e-commerce scams among the top five categories.The Shared Responsibility Framework effective December 2024 enforces 12-hour cooling-off windows and real-time surveillance, shifting liability onto platforms and financial institutions. Pokemon card frauds alone cost buyers USD 121,000 since January 2025. Blocking suspect listings, executing AI content scans, and financing refund pools inflate operating expenses. Penalties of up to USD 550,000 or 10% of turnover under the Personal Data Protection Act further weigh on profitability, shaving 2.1 percentage points off forecast CAGR for the Singapore e-commerce market.

Other drivers and restraints analyzed in the detailed report include:

- Same-Day Island-Wide Fulfillment Race

- AI-Powered Live-Stream Commerce Boom

- Manpower Shortages in Last-Mile Delivery

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

B2C channels controlled 87.65% of revenue in 2025, underscoring deep consumer digital maturity across the Singapore e-commerce market share. Mandatory Peppol invoicing pivots SMEs toward online procurement, catalyzing a 12.31% CAGR for B2B commerce and positioning the B2B slice of the Singapore e-commerce market size for steady expansion through 2031. SMEs, which form 99% of enterprises and employ 70% of the workforce, transitioned to e-procurement once fees were waived under InvoiceNow Accelerate. Cross-border tools such as DBS SecureFX permitted hedged FX exposure up to USD 1 million, while Business sans Borders matched local vendors with overseas buyers, amplifying reach.

Network effects deepen as every new invoice-enabled firm simplifies counterpart onboarding, generating a flywheel that moderates customer acquisition costs for B2B platforms within the Singapore e-commerce market. Tariff-free corridors with China heighten export order flows, further validating the digital shift. Meanwhile, B2C incumbents cross-pollinate retail shopper data to upsell supply-chain solutions, blurring channel boundaries and intensifying competition for merchant attention.

Consumer Electronics accounted for 46.82% of 2025 sales, reflecting premium device demand and high discretionary income among Singaporeans. However, food and beverages captured pandemic-induced behavior change and logistics upgrades to post a 12.37% CAGR, the fastest among all categories. Parcel-locker densification and refrigerated Singapore last mile delivery fleets now support fresh-food deliveries inside two-hour windows across the Singapore e-commerce market.

Health-centric lifestyles lifted demand for vitamin supplements and protein-rich ready-to-eat meals, showcased by Betagro's 5 million-pack chicken-breast milestone. Sustainability mandates such as packaging reporting nudged brands toward eco-friendly SKUs that appeal to conscious consumers. Fashion labels Love, Bonito and Charles and Keith innovated with virtual try-ons to deepen shopper engagement, while furniture vendors exploited AR visualization to reduce return rates. Collectively these trends diversify revenue sources and temper reliance on electronics within the Singapore e-commerce industry.

Complete Report Scope:

- By Business Model

- B2B

- B2C

- By Product Category for B2C E-commerce

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories for B2C E-commerce

- By Payment Mode for B2C E-commerce

- Credit/ Debit Cards

- Mobile Wallets

- Other Payment Modes for B2C E-commerce

- By Device

- Smartphone

- Desktop / Laptop

- Other Device Types for B2C E-commerce

List of Companies Covered in this Report:

- Sea Ltd (Shopee)

- Lazada Group SA

- Amazon Asia-Pacific Holdings Pte Ltd

- Qoo10 Pte Ltd

- ByteDance Ltd (TikTok Shop)

- eBay Inc (Gumtree SG)

- Carousell Pte Ltd

- FairPrice Online Pte Ltd

- RedMart Pte Ltd

- Zalora South East Asia Pte Ltd

- Shein Singapore Pte Ltd

- Temu Singapore Pte Ltd

- Sephora Digital SEA Pte Ltd

- iHerb LLC

- Courts Asia Ltd

- Ikea Singapore Pte Ltd

- Decathlon Singapore Pte Ltd

- Love, Bonito Pte Ltd

- Charles and Keith

- Apple South Asia Pte Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising digital-wallet penetration

- 4.2.2 Mandatory nationwide e-invoice adoption for B2B (2025)

- 4.2.3 Same-day island-wide fulfilment race

- 4.2.4 AI-powered live-stream commerce boom

- 4.2.5 Government carbon-neutral logistics grants

- 4.2.6 Cross-border China-Singapore free-trade corridors

- 4.3 Market Restraints

- 4.3.1 Escalating parcel-locker congestion

- 4.3.2 Surge in e-commerce scams and compliance costs

- 4.3.3 Manpower shortages in last-mile delivery

- 4.3.4 Data-sovereignty rules limiting cloud scaling

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Business Model

- 5.1.1 B2B

- 5.1.2 B2C

- 5.2 By Product Category for B2C E-commerce

- 5.2.1 Beauty and Personal Care

- 5.2.2 Consumer Electronics

- 5.2.3 Fashion and Apparel

- 5.2.4 Food and Beverages

- 5.2.5 Furniture and Home

- 5.2.6 Toys, DIY and Media

- 5.2.7 Other Product Categories for B2C E-commerce

- 5.3 By Payment Mode for B2C E-commerce

- 5.3.1 Credit/ Debit Cards

- 5.3.2 Mobile Wallets

- 5.3.3 Other Payment Modes for B2C E-commerce

- 5.4 By Device

- 5.4.1 Smartphone

- 5.4.2 Desktop / Laptop

- 5.4.3 Other Device Types for B2C E-commerce

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Sea Ltd (Shopee)

- 6.4.2 Lazada Group SA

- 6.4.3 Amazon Asia-Pacific Holdings Pte Ltd

- 6.4.4 Qoo10 Pte Ltd

- 6.4.5 ByteDance Ltd (TikTok Shop)

- 6.4.6 eBay Inc (Gumtree SG)

- 6.4.7 Carousell Pte Ltd

- 6.4.8 FairPrice Online Pte Ltd

- 6.4.9 RedMart Pte Ltd

- 6.4.10 Zalora South East Asia Pte Ltd

- 6.4.11 Shein Singapore Pte Ltd

- 6.4.12 Temu Singapore Pte Ltd

- 6.4.13 Sephora Digital SEA Pte Ltd

- 6.4.14 iHerb LLC

- 6.4.15 Courts Asia Ltd

- 6.4.16 Ikea Singapore Pte Ltd

- 6.4.17 Decathlon Singapore Pte Ltd

- 6.4.18 Love, Bonito Pte Ltd

- 6.4.19 Charles and Keith

- 6.4.20 Apple South Asia Pte Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment