PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689927

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689927

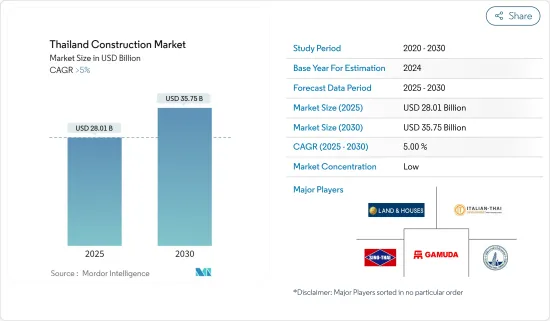

Thailand Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Thailand Construction Market size is estimated at USD 28.01 billion in 2025, and is expected to reach USD 35.75 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

Key Highlights

- The National Economic and Social Development Council (NESDC) reports that Thailand's construction industry had a year-over-year loss of 5.5% in Q1 2022, following a 0.8% decline in Q4 2021. Additionally, in Q1 2022, the total gross fixed capital formation in the construction industry decreased by 5.4% YoY.

- The Thailand Board of Investment (BOI) accepted investment proposals totaling THB209.5 billion (USD 6.6 billion) for industrial and infrastructure projects in June 2022. Additionally, rising consumer and investor confidence is anticipated to help the construction industry's expansion, as are government expenditures in housing, transportation, renewable energy, and rail projects. The expansion of the industry will also be aided by investment in the Southern Economic Corridor (SEC) and Eastern Economic Corridor (EEC) programs. A total of THB669 billion (USD 21.2 billion) in authorized initiatives has been authorized in the EEC, and four of the corridor's six major projects are now under construction and being developed through public-private partnerships (PPPs). The government is still optimistic that private investment would reach THB300 billion (USD 9.5 billion) in the EEC despite the economic hardship.

- Approximately 70% of Thailand's total rentable office space is located in the Bangkok Metropolitan Region (BMR). The central business area (CBD) of Bangkok is where office projects are most frequently found in addition to upscale hotels, apartment complexes, and iconic retail centres. The Silom, Sathorn, Ploenchit, Wireless Road, Asoke, and upper end of Sukhumvit (up to Soi 24) are all included in the CBD. The BTS, MRT, and motorways connecting this neighbourhood to Bangkok's outside regions provide excellent communication linkages. But success has a cost, and the CBD's ability to grow is constrained by a lack of appropriate land and the high cost of what is available.

Thailand Construction Market Trends

Increase in road infrastructure projects

The focus of the spending plans is a significant investment in 20 projects spread across five key sectors. These are anticipated to have the biggest effects on lowering energy and transport costs, enhancing the connection with other nations, sharing revenue and growth fairly across Thailand, and boosting private investment. The expansion of mass rapid transit networks in the BMR will receive an additional 22.1% of this financing, making up the second-largest portion of the total, behind the rail sector, which would receive 65.9% of it. 8.9% of the funding will go to the intercity road system, with the remaining 2.9% and 0.2% going to the air and water transportation sectors, respectively.

Thailand's highway and secondary road network is already far more developed than most of its neighbors, with 66,794 km of public roads, plus highways operated by the Thai Highway and Highway Transport Authority. 354 km. The majority of the country's road network is still country roads and provincial roads, of which 47,916 km and 352,157 km, respectively. For TIDMP, much of the current road development is focused on the development of ring roads around Bangkok and modern four-lane highways outside the BMR and throughout the country. Other major highways awaiting concessions include the Pattaya-Map Ta Phut Expressway, with an estimated value of 20.2 billion BT (USD 569 million), Bang Pa-in-Saraburi-Nakhon Ratchasima Expressway (84.6 billion BT, USD 24 billion), and Bang the Highway. Yai Van Phong Kanchanaburi Expressway (BT 55.6 billion, USD 1.6 billion).

Infrastructure projects drives the market

Thailand's government has settled to speed up framework venture and development in 2022, putting the need on common rail lines and quickening USD 60 billion in investing in megaprojects. The investing and speculation will increment network and coordination all through the Kingdom and with neighboring nations. It'll also impel the completion of 36 megaprojects that ought to invigorate financial advancement. The moves are a portion of the government's progressing nationwide infrastructure overhaul to extend the Kingdom's worldwide competitiveness.

Framework ventures (81% of all public-sector investing in development): Consumption rose 5.8% within the year, with the foremost vital ventures being: (1) the 3 modern MRT lines in Bangkok that are due to be opened in 2022, to be specific (i) the Orange Line from Thailand Social Center to Minburi (Suwinthawong), which is 89.5% total, (ii) the Yellow Line from Lat Phrao to Samrong, which is 88.7% total, and (iii) the Pink Line from Khae Rai to Minburi, which is 83.9% total (data adjust as of December 2021); and (2) stage 3 of the development of the Outline Ta Phut Harbour within the EEC, for which ground was broken in July 2021.

Thailand is to invest around USD 15 billion in transport infrastructure, including upgrades to its key container port, Laem Chabang, in order to boost economic growth. Of the speculation sum, generally, USD 3 billion will go towards updating Laem Chabang to extend Thailand's trade and purport cargo transportation capacity. Other than Laem Chabang, the government plans to construct and create one mechanized holder terminal along Bangkok port's West Wharf in the future.

Thailand Construction Industry Overview

The report covers the major players operating in the Thailand construction market. The market is consolidated, with over 10,000 contractors, according to registrations with the Department of Business Development.

But big contractors dominate, with the top five firms holding 70% market share. The major players in the market include Italian-Thai Development (Italthai), SCG International Corporation Company Limited, Siam Global House Public Company Limited, Land and Houses Public Company Limited, and Add Company NameDohome Public Company Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Thailand was emphasizing renewable energy projects and sustainable construction practices

- 4.2.2 Thai government was investing in various infrastructure projects to improve connectivity, transportation

- 4.3 Market Restraints

- 4.3.1 Construction projects in Thailand often experienced delays and cost overruns due to factors such as unforeseen site conditions

- 4.3.2 Political and Economic Uncertainty

- 4.4 Market Opportunities

- 4.4.1 The adoption of construction technology, Building Information Modeling (BIM), and other digital tools enhanced project management, design, and collaboration among stakeholders.

- 4.5 Value Chain / Supply Chain Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Current Economic and Construction Market Scenario

- 4.8 Technological Innovations in the Construction Sector

- 4.9 Impact of Government Regulations and Initiatives on the Industry

- 4.10 Impact of COVID-19 on the market

5 MARKET SEGMENTATION

- 5.1 By Sector

- 5.1.1 Residential

- 5.1.2 Commercial

- 5.1.3 Industrial

- 5.1.4 Infrastructure (Transportation)

- 5.1.5 Energy and Utilities

- 5.2 By Type

- 5.2.1 New Construction

- 5.2.2 Addition

- 5.2.3 Alteration

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Italian-Thai Development Public Company Limited

- 6.2.2 SCG International Corporation Company Limited

- 6.2.3 Siam Global House Public Company Limited

- 6.2.4 Land and Houses Public Company Limited

- 6.2.5 Dohome Public Company Limited

- 6.2.6 CRC Thai Watsadu Limited

- 6.2.7 Drainage and Sewerage Department

- 6.2.8 Bangkok Komatsu Company Limited

- 6.2.9 SPCC Joint Venture

- 6.2.10 Caterpillar (Thailand) Limited*

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 APPENDIX

- 8.1 Number of permits, type of construction and by region