PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1885889

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1885889

Non-GMO Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

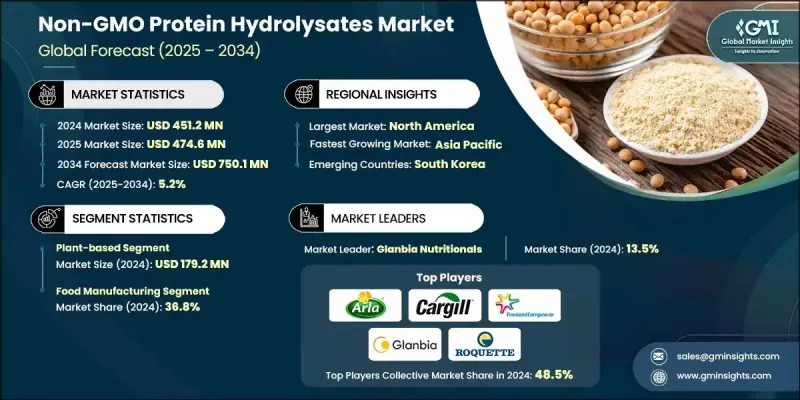

The Global Non-GMO Protein Hydrolysates Market was valued at USD 451.2 million in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 750.1 million by 2034.

These hydrolysates are produced from non-genetically modified sources and undergo controlled hydrolysis to enhance digestibility, functionality, and compatibility with clean-label product standards. Rising interest in natural and non-GMO formulations is strengthening demand across food and beverage applications, sports nutrition, and dietary supplements. North America represents the largest regional market due to strict ingredient regulations and a well-developed manufacturing framework capable of producing premium-grade hydrolysates. Meanwhile, Asia Pacific continues to grow at the fastest pace, supported by rapid urbanization, higher disposable incomes, and increased focus on food safety and agricultural sustainability. Government measures across countries such as India and China further reinforce consumer trust in non-GMO protein ingredients. The rise in food intolerances and allergies is also influencing producers to prioritize hypoallergenic and easily digestible alternatives, which rely heavily on non-GMO hydrolysates. Interest is especially notable in sports and active lifestyle nutrition, where shoppers consistently seek ingredients that deliver performance benefits without synthetic or genetically modified components.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $451.2 Million |

| Forecast Value | $750.1 Million |

| CAGR | 5.2% |

The plant-based category generated USD 179.2 million in 2024, reflecting strong demand for sustainably sourced, GMO-free protein inputs. Growing preference for natural and transparent ingredient lists has led consumers to favor plant-derived hydrolysates that align with ethical and clean-label expectations.

The food manufacturing segment held a 36.8% share in 2024. This segment benefits from increasing use of hydrolysates as functional components that enhance texture, nutritional value, and flavor while meeting rising demand for allergen-friendly and natural ingredients in packaged foods.

North America Non-GMO Protein Hydrolysates Market is projected to grow at a 5.3% CAGR between 2025 and 2034. The region continues to adopt these hydrolysates in functional foods, specialized nutrition, and supplement products, driven by strong consumer awareness and rising preference for clean-label, allergen-conscious options. Advances in enzymatic hydrolysis and sustainable extraction methods are producing higher-quality bioactive ingredients suited to evolving wellness trends.

Leading companies in the Non-GMO Protein Hydrolysates Market include Cargill Inc., Titan Biotech, Glanbia Nutritionals, Roquette Freres, Chaitanya Agro Biotech Pvt. Ltd., FrieslandCampina, International Flavors & Fragrances Inc., Carbery, Tatua Co-operative Dairy Company Limited, and Arla Foods Ingredients Group. Companies are strengthening their competitive position by expanding product lines that feature clean-label, allergen-friendly, and sustainably sourced hydrolysates tailored to food, supplement, and medical nutrition applications. Many firms are investing in advanced enzymatic processing technologies to improve flavor, solubility, and bioactive peptide profiles, enabling higher-value formulations. Strategic collaborations with food manufacturers and wellness brands are helping companies secure long-term supply partnerships. Firms are also emphasizing rigorous quality certification and transparent sourcing practices to reinforce consumer trust in non-GMO ingredients.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Source trends

- 2.2.2 Application trends

- 2.2.3 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer demand for clean-label & non-GMO products

- 3.2.1.2 Increasing prevalence of food allergies & intolerances

- 3.2.1.3 Growing sports nutrition & active lifestyle market

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs & premium pricing

- 3.2.2.2 Limited raw material availability for non-GMO sources

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in animal feed applications

- 3.2.3.2 Emerging applications in personalized nutrition

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By source

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Source, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Plant-based

- 5.2.1 Pea protein hydrolysates

- 5.2.2 Soy protein hydrolysates

- 5.2.3 Rice protein hydrolysates

- 5.2.4 Wheat/gluten hydrolysates

- 5.3 Animal-based

- 5.3.1 Milk protein hydrolysates (whey, casein)

- 5.3.2 Meat protein hydrolysates

- 5.3.3 Egg protein hydrolysates

- 5.4 Marine-based

- 5.4.1 Fish protein hydrolysates

- 5.4.2 Collagen hydrolysates

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Therapeutic & medical applications

- 6.2.1 Infant & pediatric nutrition

- 6.2.2 Adult clinical nutrition

- 6.2.3 Foods for special medical purposes

- 6.3 Consumer nutrition & wellness applications

- 6.3.1 Sports & performance nutrition

- 6.3.2 General health & wellness

- 6.4 Food manufacturing applications

- 6.4.1 Processed food ingredients

- 6.4.2 Beverage ingredients

- 6.4.3 Flavor & texture enhancement

- 6.5 Animal nutrition applications

- 6.5.1 Companion animal feed

- 6.5.2 Livestock feed

- 6.5.3 Aquaculture feed

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Arla Foods Ingredients Group

- 8.2 Carbery

- 8.3 Cargill Inc.

- 8.4 Chaitanya Agro Biotech Pvt. Ltd.

- 8.5 FrieslandCampina

- 8.6 Glanbia Nutritionals

- 8.7 International Flavors & Fragrances Inc

- 8.8 Roquette Freres

- 8.9 Tatua Co-operative Dairy Company Limited

- 8.10 Titan Biotech