PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045767

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045767

Gaming Handheld Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

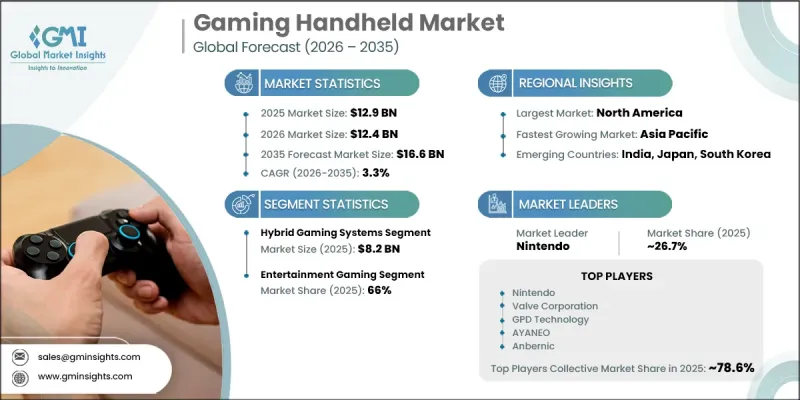

The Global Gaming Handheld Market was valued at USD 12.9 billion in 2025 and is estimated to grow at a CAGR of 3.3% to reach USD 16.6 billion by 2035.

Growth across the handheld gaming industry is fueled by the increasing consumer preference for portable gaming experiences that offer convenience and flexibility. Players are actively seeking compact gaming devices that support entertainment while traveling, commuting, or engaging in daily activities without depending on fixed gaming setups. Handheld gaming consoles continue to gain traction due to their portability, accessibility, and ability to deliver engaging gameplay experiences across a broad selection of titles. Continuous advancements in processor performance, graphics capabilities, battery life, and display quality are significantly improving the overall user experience. Manufacturers are increasingly introducing lightweight gaming devices equipped with responsive controls and enhanced visual performance to attract a wider consumer base. In addition, the rapid expansion of cloud gaming infrastructure and connected gaming ecosystems is accelerating demand within the gaming handheld market. Integration with digital gaming platforms and subscription-based services is improving content accessibility and enhancing user engagement. Portable gaming systems are also becoming more compatible with connected ecosystems and network-based gaming environments. Rising global interest in competitive gaming culture and streaming entertainment is further supporting the adoption of high-performance handheld gaming devices worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.9 Billion |

| Forecast Value | $16.6 Billion |

| CAGR | 3.3% |

In 2025, the hybrid gaming systems segment accounted for USD 8.2 billion. The segment continues to dominate because these devices provide the flexibility to function as portable gaming systems and as home-based gaming consoles when connected to external displays. This dual-purpose functionality enhances convenience and improves the overall gaming experience for users across different environments. Hybrid gaming systems attract a broad range of consumers, including both casual players and performance-focused gamers, due to their ability to combine mobility with advanced gaming capabilities. Growing consumer interest in versatile gaming products and seamless transitions between portable and larger-screen gaming experiences is driving continued demand for hybrid gaming systems across global markets.

The entertainment gaming segment held a 66% share in 2025 and is expected to register a CAGR of 1.8% from 2026 to 2035. Strong adoption of handheld gaming devices for leisure activities, recreational gaming, and immersive digital entertainment experiences continues to support segment growth. Consumers increasingly favor portable gaming platforms that allow uninterrupted gameplay across different locations, making entertainment-focused gaming the leading application area within the market. The segment includes a broad variety of gaming formats designed to appeal to diverse demographics and gaming preferences. Rising engagement with portable entertainment technologies and growing demand for accessible gaming experiences are expected to sustain the expansion of the entertainment gaming segment throughout the forecast period.

U.S. Gaming Handheld Market captured USD 3.9 billion in 2025 and is anticipated to grow at a CAGR of 2.4% from 2026 to 2035. Strong market leadership in the United States is supported by a highly developed gaming ecosystem and rising consumer demand for premium portable gaming devices. Growth is being driven by increasing interest in high-performance handheld consoles that provide advanced gaming experiences and seamless connectivity across multiple gaming environments. Portable gaming devices offering strong graphics performance, improved mobility, and integrated ecosystem compatibility continue to witness rising adoption among consumers in the country. Demand for multifunctional gaming systems that combine portability with enhanced gameplay capabilities is expected to remain a major factor supporting the growth of the U.S. gaming handheld industry.

Major companies operating in the Global Gaming Handheld Market include Nintendo, Valve Corporation, Sony Interactive Entertainment, ASUS, Lenovo, MSI, and AYN. Additional regional participants active in the market include Anbernic, GPD Technology, OneXPlayer, AYANEO, Retroid, Powkiddy, and Atari. Emerging and specialized companies contributing to industry competition include Razer, Logitech, Panic, AYN Thor, Miyoo, ZOTAC, and Trimui. Companies competing in the Global Gaming Handheld Market are adopting multiple strategies to strengthen their market position and improve long-term competitiveness. Leading manufacturers are focusing on continuous product innovation by developing lightweight handheld consoles with advanced graphics, enhanced battery performance, and improved processing capabilities. Many businesses are investing in cloud gaming integration and cross-platform compatibility to expand user engagement and improve accessibility across gaming ecosystems. Strategic partnerships with gaming platform providers and software developers are also helping companies broaden their content offerings and strengthen brand visibility. In addition, market participants are expanding distribution networks and increasing investments in research and development activities to accelerate product launches.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Form

- 2.2.4 Technology

- 2.2.5 Age Group

- 2.2.6 Display Size

- 2.2.7 Price Range

- 2.2.8 Application

- 2.2.9 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising popularity of portable and on-the-go gaming experiences

- 3.2.1.2 Expansion of high-performance gaming ecosystems and cloud gaming services

- 3.2.1.3 Growing gaming community and esports influence globally

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High competition from smartphones and tablets as gaming alternatives

- 3.2.2.2 High product pricing for premium handheld gaming devices

- 3.2.3 Opportunities

- 3.2.3.1 Growth of subscription-based cloud gaming platforms

- 3.2.3.2 Rising demand for hybrid and modular gaming devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.8.1 Pricing analysis (driven by primary research)

- 3.8.1.1 Historical price trend analysis (2019-2024) (driven by primary research)

- 3.8.1.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.8.1.3 Regional price variations and purchasing power parity

- 3.8.1.4 Component cost dynamics and BOM analysis

- 3.8.1.5 Price elasticity of demand by segment

- 3.8.2 Trade data analysis (HS code- 9504.50) (driven by paid data base)

- 3.8.2.1 Import/export volume and value trends (2019-2024) (driven by paid data base)

- 3.8.2.2 Key trade corridors and tariff impact (driven by paid data base)

- 3.8.2.3 HS code classification and trade flow mapping

- 3.8.2.4 Cross-border e-commerce dynamics

- 3.8.3 Impact of AI and generative AI on the market

- 3.8.3.1 AI-driven disruption of existing business models

- 3.8.3.2 GenAI use cases and adoption roadmap by segment

- 3.8.3.3 AI-powered game development and optimization

- 3.8.3.4 Personalized gaming experiences via AI

- 3.8.3.5 AI-enhanced performance management

- 3.8.3.6 Natural language processing for voice control

- 3.8.3.7 Computer vision for eye tracking and biometric controls

- 3.8.3.8 Risks, limitations and regulatory considerations

- 3.8.3.9 AI hardware integration trends (NPUs, edge AI chips)

- 3.8.4 Distribution infrastructure and channel penetration landscape (driven by primary research)

- 3.8.4.1 Channel coverage by region and format (modern vs. traditional trade) (driven by primary research)

- 3.8.4.2 Last-mile infrastructure gaps and emerging channel shifts (driven by primary research)

- 3.8.4.3 E-commerce platform penetration by geography

- 3.8.4.4 Retailer consolidation and shelf space dynamics

- 3.8.1 Pricing analysis (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Dedicated handheld gaming consoles

- 5.3 Hybrid gaming systems

- 5.4 Handheld gaming pcs

- 5.5 Android gaming handhelds

Chapter 6 Market Estimates & Forecast, By Form, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Traditional handheld

- 6.3 Clamshell

- 6.4 Slider

- 6.5 Modular

- 6.6 Foldable

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Touch only

- 7.3 Physical controls

- 7.4 Hybrid touch & physical

- 7.5 Motion control

- 7.6 Voice control

- 7.7 Eye tracking & biometric

Chapter 8 Market Estimates & Forecast, By Age Group, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Children

- 8.3 Teenagers

- 8.4 Adults

Chapter 9 Market Estimates & Forecast, By Display Size, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Small screen devices (3-5 inches)

- 9.3 Medium screen devices (5-7 inches)

- 9.4 Large screen devices (7-9 inches)

- 9.5 Extra-large screen devices (9+ inches)

Chapter 10 Market Estimates & Forecast, By Price Range, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Low

- 10.3 Medium

- 10.4 High

Chapter 11 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Entertainment gaming

- 11.3 Professional & competitive gaming

- 11.4 Educational gaming applications

- 11.5 Cloud & streaming gaming

Chapter 12 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 Offline

- 12.3 Online

Chapter 13 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 U.S.

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Italy

- 13.3.5 Spain

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 South Korea

- 13.4.5 Australia

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.6 MEA

- 13.6.1 Saudi Arabia

- 13.6.2 UAE

- 13.6.3 South Africa

Chapter 14 Company Profiles

- 14.1 Top Global Players

- 14.1.1 Nintendo

- 14.1.2 Valve Corporation

- 14.1.3 Sony Interactive Entertainment

- 14.1.4 ASUS

- 14.1.5 Lenovo

- 14.1.6 MSI

- 14.1.7 AYN

- 14.2 Regional Champions

- 14.2.1 Anbernic

- 14.2.2 GPD Technology

- 14.2.3 OneXPlayer

- 14.2.4 AYANEO

- 14.2.5 Retroid

- 14.2.6 Powkiddy

- 14.2.7 Atari

- 14.3 Emerging & Specialized Players

- 14.3.1 Razer

- 14.3.2 Logitech

- 14.3.3 Panic

- 14.3.4 AYN Thor

- 14.3.5 Miyoo

- 14.3.6 ZOTAC

- 14.3.7 Trimui