PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045823

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045823

Dog Footwear Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

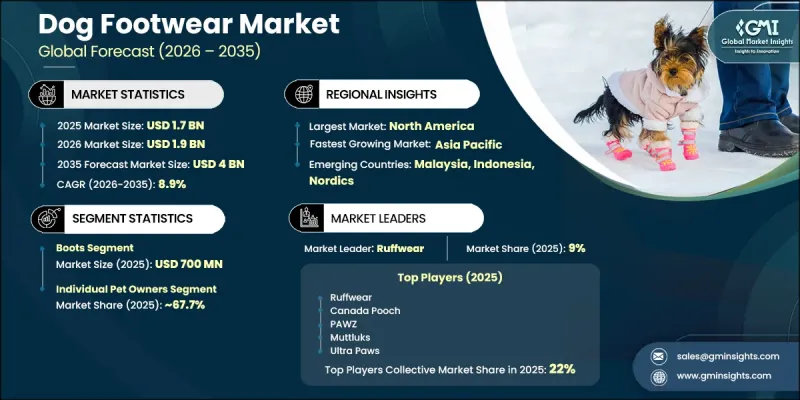

The Global Dog Footwear Market was valued at USD 1.7 billion in 2025 and is estimated to grow at a CAGR of 8.9% to reach USD 4 billion by 2035.

The industry is gaining momentum due to the rising trend of pet humanization, where dogs are increasingly regarded as integral family members rather than companion animals alone. This shift is reshaping consumer expectations around comfort, protection, and lifestyle-oriented pet care products, driving consistent demand for premium dog footwear. Pet owners are increasingly seeking products that combine functional protection with modern design aesthetics, reflecting their own lifestyle preferences. Growing focus on pet health, comfort, and preventive care is also contributing to the perception of dog footwear as an essential accessory rather than a discretionary item. In addition, rising disposable incomes, especially in urban regions, are enabling higher spending on premium pet care solutions. Consumers are increasingly willing to invest in advanced protective footwear that enhances paw safety across varying environmental conditions. This evolving spending behavior is reducing price sensitivity and encouraging product innovation, customization, and material advancements, thereby supporting long-term market expansion across global regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.7 Billion |

| Forecast Value | $4 Billion |

| CAGR | 8.9% |

The dog footwear market is also benefiting from increasing awareness of pet safety in harsh environmental conditions and growing urbanization. Expanding pet care expenditure patterns and the rising popularity of premium pet lifestyle products are further strengthening market demand. Continuous product innovation and growing adoption of specialized protective accessories are expected to sustain growth momentum across both developed and emerging economies.

The boots segment accounted for USD 700 million in 2025. This product category leads the market due to its superior protective performance, durability, and versatility across a wide range of conditions. Dog boots provide enhanced coverage compared to lighter alternatives, offering protection from extreme temperatures, rough terrain, sharp objects, and surface chemicals. Their structured build improves grip, insulation, and long-term usability, making them suitable for both everyday urban walks and outdoor activities. The combination of functional protection and durability continues to drive strong consumer preference for this segment.

The individual pet owners segment held a share of 67.7% in 2025. This segment's leadership is driven by changing perceptions of pet ownership, where dogs are increasingly treated as family members with prioritized health and comfort needs. Individual consumers are actively investing in specialized pet care products, particularly those designed to enhance safety and protection in daily environments. Growing awareness of paw health and protection against temperature extremes and urban surfaces has significantly increased demand for dog footwear among private pet owners.

U.S. Dog Footwear Market held an 81% share, generating USD 0.53 billion in 2025. Market strength in the United States is supported by a highly developed pet care industry and strong consumer spending on premium pet accessories. High pet ownership rates, combined with deep emotional attachment between owners and pets, continue to drive demand for functional and high-quality dog footwear. Increasing awareness of paw protection needs in urban environments and extreme weather conditions further supports sustained market growth across the country.

Major companies operating in the Global Dog Footwear Market include Ruffwear, Muttluks, Kurgo, PawZ Dog Boots, Ultra Paws, Neo Paws, Canada Pooch, Hurtta, Rukka Pets, RC Pet Products, Non-stop Dogwear, Woodrow Wear, Walkee Paws, Bark Brite, RIFRUF, Dogsoxx, Fetchers, Spark Paws, and Guangzhou Voyager Pet Products. Companies operating in the dog footwear market are adopting multiple strategies to strengthen their competitive positioning and expand consumer reach. Manufacturers are focusing on product innovation by developing ergonomic, weather-resistant, and durable footwear designed for different climates and terrains. Emphasis on premium materials and improved comfort features is helping brands differentiate their offerings in a competitive market. Companies are also investing in customization options, allowing pet owners to select sizes, designs, and functional features tailored to specific needs. Expansion of online retail channels and direct-to-consumer platforms is improving accessibility and brand visibility across global markets. Strategic partnerships with pet specialty retailers and veterinary channels are further strengthening distribution networks.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Material

- 2.2.4 Application

- 2.2.5 Price range

- 2.2.6 End user

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology/innovation landscape

- 3.5.1 Material innovation trends

- 3.5.2 Manufacturing technology advancements

- 3.5.3 Customization & 3D printing technologies

- 3.5.4 Smart footwear & wearable integration

- 3.5.5 Sustainability & Eco-Friendly Material Development

- 3.6 Regulatory Framework

- 3.6.1 Pet product safety regulations by region

- 3.6.2 Material & chemical compliance standards

- 3.6.3 Import/export regulations & tariffs

- 3.6.4 Labeling & packaging requirements

- 3.7 Pricing Analysis (Driven by Primary Research)

- 3.7.1 Historical price trend analysis (driven by primary research)

- 3.7.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.7.3 Regional price variations & factors

- 3.7.4 Price sensitivity analysis by consumer segment

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade data analysis HS Code: (4201.00.6000): Dog booties/boots (Driven by paid database)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.10.3 Trade balance by region

- 3.10.4 Emerging trade routes & opportunities

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

- 3.11.4 AI in product design & customization

- 3.11.5 AI-powered sizing & fit recommendations

- 3.12 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.12.1 Channel coverage by region & format (modern vs. traditional trade) (driven by primary research)

- 3.12.2 Last-mile infrastructure gaps & emerging channel shifts (driven by primary research)

- 3.12.3 Omnichannel retail penetration & maturity assessment

- 3.13 Consumer buying behavior analysis

- 3.13.1 Demographic trends & pet ownership patterns

- 3.13.2 Psychographic segmentation of pet owners

- 3.13.3 Factors affecting purchase decisions

- 3.13.4 Product preference & feature prioritization

- 3.13.5 Preferred price range & willingness to pay

- 3.13.6 Preferred distribution channel analysis

- 3.13.7 Brand loyalty & switching behavior

- 3.13.8 Influence of social media & online reviews

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Boots

- 5.2.1 All-terrain boots

- 5.2.2 Winter/snow boots

- 5.2.3 Waterproof boots

- 5.2.4 Fashion boots

- 5.3 Shoes

- 5.3.1 Casual/everyday shoes

- 5.3.2 Sport/performance shoes

- 5.3.3 Indoor shoes

- 5.4 Socks

- 5.4.1 Non-slip socks

- 5.4.2 Therapeutic/medical socks

- 5.4.3 Fashion socks

- 5.5 Sandals

- 5.5.1 Summer sandals

- 5.5.2 Breathable sandals

- 5.6 Paw protectors

- 5.6.1 Disposable paw protectors

- 5.6.2 Reusable paw protectors

- 5.6.3 Paw wax & balm alternatives

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Leather

- 6.2.1 Full-grain leather

- 6.2.2 Synthetic leather

- 6.3 Rubber

- 6.3.1 Natural

- 6.3.2 Synthetic

- 6.4 Neoprene

- 6.5 Nylon

- 6.6 Polyester

- 6.7 Others (biodegradable materials, recycled materials, etc.)

Chapter 7 Market Estimates and Forecast, By Price Range, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 All-Terrain/outdoor activities

- 8.2.1 Hiking & trail activities

- 8.2.2 Running & jogging

- 8.2.3 Rough terrain protection

- 8.3 Weather protection

- 8.3.1 Cold weather/snow protection

- 8.3.2 Hot pavement/summer protection

- 8.3.3 Rain & wet condition protection

- 8.4 Indoor/casual use

- 8.4.1 Home use & floor protection

- 8.4.2 Light protection

- 8.4.3 Fashion & aesthetic use

- 8.5 Medical/therapeutic

- 8.5.1 Injury recovery & wound protection

- 8.5.2 Mobility support for senior dogs

- 8.5.3 Protection for medical conditions

- 8.6 Performance/Sport

- 8.6.1 Professional training

- 8.6.2 Working dogs (police, search & rescue, Military)

- 8.6.3 Competitive activities

Chapter 9 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Individual pet owners

- 9.3 Professional users

- 9.3.1 Veterinary clinics

- 9.3.2 Professional trainers

- 9.3.3 Groomers & pet care services

- 9.3.4 Breeders

- 9.3.5 Working dog handlers

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Online channels

- 10.2.1 E-commerce

- 10.2.2 Company websites

- 10.3 Offline channels

- 10.3.1 Supermarkets/hypermarkets

- 10.3.2 Specialty pet stores

- 10.3.3 Others (departmental stores, etc.)

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Top Global Players

- 12.1.1 Ruffwear

- 12.1.2 Muttluks

- 12.1.3 Kurgo

- 12.1.4 PawZ Dog Boots

- 12.1.5 Ultra Paws

- 12.1.6 Neo-Paws

- 12.1.7 Canada Pooch

- 12.2 Regional Players

- 12.2.1 Hurtta

- 12.2.2 Rukka Pets

- 12.2.3 RC Pet Products

- 12.2.4 Guangzhou Voyager Pet Products

- 12.2.5 Non-stop Dogwear

- 12.2.6 Healers Petcare

- 12.2.7 Saltsox

- 12.3 Emerging Players

- 12.3.1 Dogsoxx

- 12.3.2 Bark Brite

- 12.3.3 Woodrow Wear (Power Paws)

- 12.3.4 Walkee Paws

- 12.3.5 Fetchers

- 12.3.6 Spark Paws

- 12.3.7 RIFRUF