PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061294

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061294

Asia-Pacific Agricultural Sprayers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

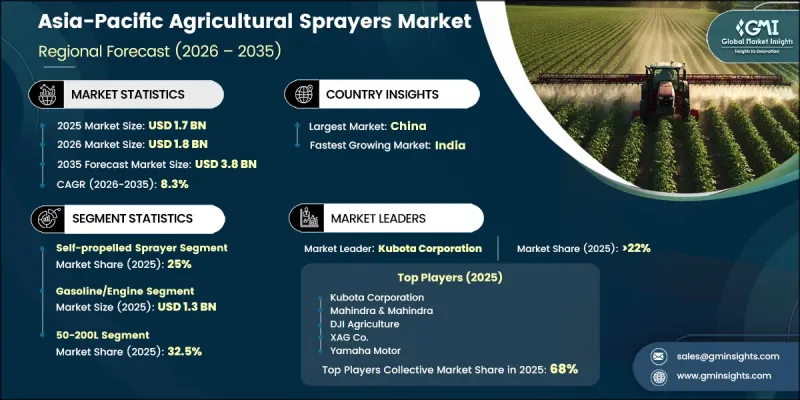

Asia-Pacific Agricultural Sprayers Market was valued at USD 1.7 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 3.8 billion by 2035.

Rapid expansion across the Asia-Pacific agricultural sprayers industry is fueled by rising agricultural mechanization, increasing pressure on farm productivity, and the continued development of crop management and precision agriculture practices throughout the region. Farmers are increasingly investing in advanced spraying equipment to improve operational efficiency, crop protection, and agricultural output. Growing demand for technologically enhanced spraying systems is encouraging manufacturers to focus on product innovation and performance optimization. The market is also benefiting from the modernization of farming operations and the increasing need for efficient agricultural equipment capable of supporting large-scale cultivation activities. Expanding digital sales channels are making agricultural sprayers more accessible to farming businesses by improving product visibility and simplifying purchasing decisions. In addition, manufacturers are emphasizing durable construction, advanced engineering, and long-term operational reliability to meet evolving agricultural requirements. Continuous improvements in farming infrastructure and growing awareness regarding precision spraying technologies are expected to support sustained growth across the Asia-Pacific agricultural sprayers market over the coming years.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.7 Billion |

| Forecast Value | $3.8 Billion |

| CAGR | 8.3% |

The self-propelled sprayer segment accounted for a 25% share, generating USD 430 million in 2025. Demand for self-propelled sprayers continues to rise due to their ability to support high-capacity spraying operations and efficient field coverage across large agricultural areas. Commercial farming businesses are increasingly adopting these systems to improve precision spraying performance and optimize crop protection activities. The segment is also gaining traction because modern self-propelled sprayers are equipped with advanced operational technologies that improve spraying accuracy, field efficiency, and overall productivity. Continuous technological advancements in automated spraying systems are further strengthening the adoption of these machines across large-scale farming operations.

The gasoline and engine-powered segment held a 77.3% share, generating USD 1.3 billion in 2025. Engine-driven sprayers remain highly preferred because they deliver strong operational power, longer working durations, and reliable performance for intensive agricultural applications. These systems are widely utilized by commercial farmers seeking efficient spraying equipment capable of handling demanding field conditions. Manufacturers are also improving fuel efficiency and reducing emissions to align with evolving environmental standards and operational cost concerns. At the same time, battery-operated agricultural sprayers are witnessing rapid growth due to rising environmental awareness, lower maintenance requirements, and improved ease of use among farming operators.

China Agricultural Sprayers Market held a 39.04% share, generating USD 670 million. China's leadership position is supported by its extensive agricultural sector, expanding mechanization initiatives, and growing adoption of precision farming technologies. The market continues to benefit from increasing investments in modern agricultural infrastructure and rising demand for advanced spraying systems that improve farming efficiency and crop management. Agricultural producers across the country are increasingly adopting technologically advanced equipment designed to enhance productivity and operational performance. Ongoing modernization efforts and strong government support for agricultural development continue to generate steady demand for agricultural sprayers across key farming regions.

Major companies operating in the Asia-Pacific agricultural sprayers market include Kubota Corporation, Mahindra & Mahindra, TAFE Motors & Tractors, DJI Agriculture, XAG Co., Ltd., Yamaha Motor, Yanmar Co., Ltd., YTO Group Corporation, Lovol, Changfa Agricultural Equipment, Fieldking Agricultural Equipment, Shaanxi Kingtai Agricultural Machinery, Indo-Farm Equipment, Swaraj, VST Tillers Tractors, Zoomlion Heavy Industry, Hatsuyuki Machinery, Jiangsu Lianyungang Hua Tai Machinery, Zhejiang Ousen Machinery, Shaktiman, and Jiangsu World Agricultural Machinery. Companies operating in the Asia-Pacific agricultural sprayers industry are implementing several strategic initiatives to strengthen their market presence and improve competitive positioning. Manufacturers are heavily investing in research and development activities to introduce technologically advanced spraying systems with precision farming capabilities, automated controls, and improved operational efficiency. Many companies are also focusing on expanding regional distribution networks and digital sales platforms to improve customer accessibility and strengthen market penetration. Strategic partnerships with agricultural equipment dealers and farming organizations are helping businesses increase brand visibility and customer engagement. In addition, manufacturers are prioritizing durable product design, fuel-efficient technologies, and environmentally sustainable solutions to align with evolving agricultural standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product Type

- 2.2.2 Power Source

- 2.2.3 Technology

- 2.2.4 Capacity

- 2.2.5 Usage

- 2.2.6 Crop Type

- 2.2.7 End User

- 2.2.8 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Drivers

- 3.2.2 Pitfalls & Challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (2020-2024) (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium/Mid-Range/Value) (Driven by Primary Research)

- 3.6.3 Price Comparison: Proprietary Brands vs. Partnership Brands vs. Generic

- 3.6.4 Average Selling Price by Product Type & Capacity

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis (Driven by Primary Research)

- 3.10.1 Import/Export Volume & Value Trends (2020-2024) (Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Origin Countries (China, Vietnam, South Korea) (Driven by Primary Research)

- 3.10.3 Tariff Impact & Trade Agreement Implications

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Traditional Spraying Methods

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Farm Size

- 3.11.3 Risks, Limitations & Regulatory Considerations for AI-Enabled Sprayers

- 3.12 Refurbishment Capacity & Dealer Infrastructure Landscape (Driven by Primary Research)

- 3.12.1 Refurbishment Facility Capacity by Region & Key Player (Driven by Primary Research)

- 3.12.2 Dealer Network Density & Auction Throughput Analysis (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Handheld sprayer

- 5.3 Knapsack sprayer

- 5.4 Trailed sprayer

- 5.5 Mounted sprayer

- 5.6 Self-propelled sprayer

- 5.7 Aerial sprayer

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Power Source, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Battery

- 6.3 Gasoline/Engine

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Hydraulic nozzles

- 7.3 Air-assisted electrostatic

- 7.4 Ultra-Low Volume (ULV) spraying

- 7.5 Precision spraying

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Capacity, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Below 50L

- 8.3 50-200L

- 8.4 200-500 L

- 8.5 Above 500L

Chapter 9 Market Estimates & Forecast, By Usage, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Insecticides/Pesticides

- 9.3 Herbicides

- 9.4 Fungicides

- 9.5 Fertilizers

Chapter 10 Market Estimates & Forecast, By Crop Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Cereals & Grains

- 10.3 Oilseeds & Pulses

- 10.4 Fruits & Flowers

- 10.5 Stem & Tubers

- 10.6 Other (Plantation Crops, Forestry, etc.)

Chapter 11 Market Estimates & Forecast, By End User, 2022 - 2035, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Small Farmers

- 11.3 Medium Farmers

- 11.4 Large Farms

- 11.5 Institutions & Commercial Farms

Chapter 12 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 Online

- 12.3 Offline

Chapter 13 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 13.1 Key trends

- 13.2 China

- 13.3 India

- 13.4 Japan

- 13.5 South Korea

- 13.6 Indonesia

- 13.7 Thailand

- 13.8 Singapore

- 13.9 Australia

Chapter 14 Company Profiles

- 14.1 Top Global Player

- 14.1.1 Kubota Corporation

- 14.1.2 Mahindra & Mahindra

- 14.1.3 TAFE Motors & Tractors

- 14.1.4 DJI Agriculture

- 14.1.5 XAG Co., Ltd.

- 14.1.6 Yamaha Motor

- 14.1.7 Yanmar Co., Ltd.

- 14.2 Regional Player

- 14.2.1 YTO Group Corporation

- 14.2.2 Lovol

- 14.2.3 Changfa Agricultural Equipment

- 14.2.4 Fieldking Agricultural Equipment

- 14.2.5 Shaanxi Kingtai Agricultural Machinery

- 14.2.6 Indo-Farm Equipment

- 14.2.7 Swaraj

- 14.2.8 VST Tillers Tractors

- 14.2.9 Zoomlion Heavy Industry

- 14.3 Emerging Players

- 14.3.1 Hatsuyuki Machinery

- 14.3.2 Jiangsu Lianyungang Hua Tai Machinery

- 14.3.3 Zhejiang Ousen Machinery

- 14.3.4 Shaktiman

- 14.3.5 Jiangsu World Agricultural Machinery