PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066484

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066484

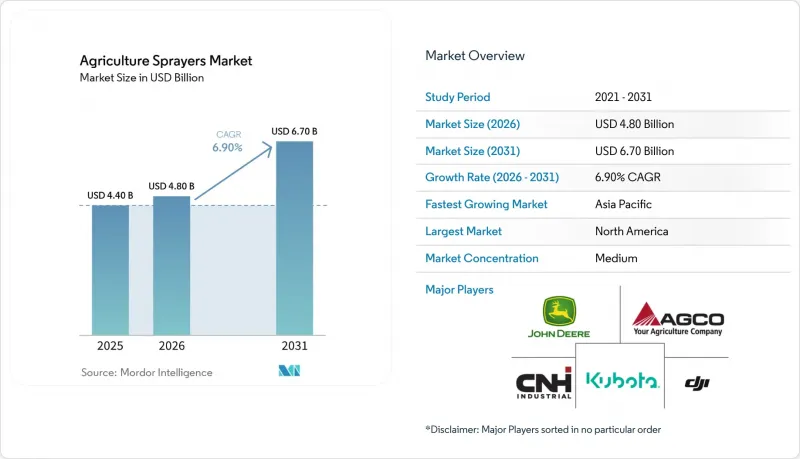

Agriculture Sprayers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the agriculture sprayers market size is projected to grow from USD 4.4 billion in 2025 to USD 4.8 billion in 2026 and USD 6.7 billion by 2031, registering a CAGR of 6.9% from 2026 to 2031.

This report is Segmented by Source of Power (Manual, Solar-Powered, and More), by Product Type (Tractor-Mounted, and More), by Application (Field Crops And, More), by Spray Volume (Low Volume and More), by Technology Level (Conventional and More), by Pump Mechanism (Diaphragm Pumps and More), and by Geography (North America, Africa and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Agriculture Sprayers Market Trends and Insights

Growth in Agrochemical Usage

Increasing pesticide application intensity continues to drive baseline equipment demand in the agriculture sprayers market. According to the United States Department of Agriculture Economic Research Service (USDA, ERS), herbicide-tolerant soybean acreage in the United States accounted for 96% of the planted area in 2024 and 2025, highlighting the ongoing reliance on crop protection chemical applications in large-scale farming systems. Higher spraying frequency in broadacre crops leads to increased equipment operating hours and accelerates wear on components such as nozzles, pumps, hoses, and boom assemblies. This trend supports consistent replacement demand for agricultural sprayers and aftermarket consumable components, particularly in intensive row-crop production regions where multiple spray applications are standard during the growing season.

Precision Spraying Upgrades Using Sensors

Sensor-based upgrades are expanding opportunities in the agriculture sprayers market, as many growers can retrofit their existing equipment instead of replacing entire machines. Deere & Company has introduced expanded upgrade options and boom configurations for Model Year 2026 equipment and earlier models, indicating that retrofitting is becoming a significant adoption pathway rather than a niche solution. As sensing accuracy improves and installation costs become more justifiable, precision spraying is transitioning from a premium feature to a standard productivity tool for commercial farming operations.

High Upfront Capital Expenditure and Financing Hurdles

Capital costs continue to pose a significant challenge for the agriculture sprayers market, particularly for farms unable to recoup the investment in advanced equipment within two to three seasons. EXEL Industries reported a 15.7% decline in agricultural spraying revenue during the first half of the fiscal year 2024-2025, attributing the weakness in North America to farmers adopting a cautious approach due to limited economic visibility. The challenge is more pronounced in the segment of AI-enabled and autonomous equipment, where purchase decisions often encompass hardware, software, and service costs rather than a single machine expense. This has led some growers to opt for retrofits, delay equipment replacement, or rely on external service providers, even when the technical benefits of upgrading are evident. Without an easing of credit conditions or broader adoption of leasing models, the uptake of advanced technologies is likely to remain below its potential in several established farming regions.

Other drivers and restraints analyzed in the detailed report include:

- Rising Labor Costs and Operator Shortages

- Government Mechanization and Smart-Farming Subsidies

- Limited Operator and Agronomy Data Skills

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The agriculture sprayers market share for the fuel-operated segment held the largest 36.0% in 2025. These sprayers maintain their dominance due to their longer operating endurance and suitability for large boom and self-propelled applications in broadacre farming systems. They are widely preferred in regions such as North America, South America, and Europe, where large field sizes necessitate uninterrupted spraying during narrow application windows. Manual and solar-assisted systems continue to serve niche roles in smallholder agriculture and greenhouse production. The segment's stability is further supported by established dealer networks, maintenance familiarity, and existing fuel infrastructure in major agricultural economies.

The agriculture sprayers market size for the battery-operated segment is forecasted to grow at the fastest 12.1% CAGR from 2026 to 2031. This growth is driven by increasing adoption of drones, lightweight autonomous platforms, and advancements in lithium-ion battery efficiency. Battery-powered systems are becoming increasingly suitable for orchard spraying, greenhouse operations, and compact field applications, where their lower operating noise and reduced emissions offer significant advantages. Manufacturers are also incorporating digital monitoring and automated application systems into battery-operated platforms to enhance precision and performance. Despite this growth, fuel-operated systems remain essential for high-capacity crop protection applications, where extended operating hours are critical for maintaining productivity.

Tractor-mounted systems accounted for the largest 41.4% share in 2025. These sprayers maintain a strong position due to their seamless integration with existing tractor fleets and their cost-effective approach to adopting precision spraying technologies. They are widely used in North America and Europe, where established agricultural machinery infrastructure supports consistent replacement demand. Additionally, trailed and self-propelled sprayers remain relevant for large-scale field operations that require higher tank capacities and wider boom coverage. This segment benefits from robust aftermarket support, easier maintenance, and compatibility with guidance and retrofit technologies commonly used in commercial farming operations.

Unmanned aerial vehicle sprayers are forecasted to expand at the fastest 28.1% CAGR from 2026 to 2031. This growth is driven by increasing labor shortages, rising demand for precision application, and the expanding adoption of aerial spraying in orchards, rice fields, and specialty crops. Unmanned aerial vehicle (UAV) sprayers offer advantages such as terrain adaptability, reduced reliance on labor, and rapid deployment during narrow treatment windows. Manufacturers are enhancing commercial adoption by providing training support, fleet management software, and autonomous route-planning systems. While ground-based sprayers continue to dominate global installed capacity, drone systems are increasingly being adopted for applications where speed, targeted spraying accuracy, and operational efficiency deliver greater economic value to agricultural operators.

Geography Analysis

North America held the largest 32.0% share in 2025. This leadership is attributed to extensive production systems for crops such as corn, soybean, wheat, and canola, which require high-capacity spraying operations. The United States drives regional demand through the widespread adoption of self-propelled sprayers, precision application technologies, and digital farm management systems. Canada also contributes significantly, with large commercial grain operations necessitating advanced spraying equipment capable of high field coverage. Factors such as an established dealer network, recurring equipment replacement cycles, and strong adoption of precision agriculture technologies continue to support stable demand for advanced agricultural spraying platforms across large-scale commercial farming operations in the region.

Asia-Pacific is forecast to grow at the fastest 8.5% CAGR from 2026 to 2031. This growth is driven by increasing farm mechanization, rising deployment of agricultural drones, and expanding government support for precision agriculture technologies. China is advancing agricultural equipment modernization through subsidy programs that promote plant protection drones and smart farming technologies. India, Japan, and Australia are also increasing the adoption of Unmanned Aerial Vehicle (UAV) spraying systems, as labor shortages and challenging terrain enhance the economic value of aerial spraying. Regional manufacturers are focusing on expanding operator training, dealer support, and digital spraying ecosystems, solidifying Asia-Pacific's position as a growing hub for the production and development of advanced agricultural spraying solutions globally.

Europe remains a mature market influenced by regulatory frameworks, where recurring equipment renewal is driven by compliance requirements and improved application control. The European Commission's December 2025 simplification proposal has introduced the possibility of general drone derogations under specific risk conditions, potentially expanding the market for Unmanned Aerial Vehicle (UAV) spraying after 2026. In South America, Brazil's extensive commercial farming base and strong demand for tractor-mounted and self-propelled equipment make the region significant. Meanwhile, the Middle East and Africa, though at an earlier stage, are becoming increasingly relevant as food security objectives and export residue standards encourage selective precision upgrades.

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- Mahindra & Mahindra Limited

- SZ DJI Technology Co., Ltd.

- EXEL Industries

- Maquinas Agricolas Jacto S.A.

- AMAZONEN-WERKE H. DREYER SE & Co. KG

- Bucher Industries AG

- Yamaha Motor Co., Ltd.

- XAG Co., Ltd.

- HORSCH Maschinen GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in agrochemical usage

- 4.2.2 Precision spraying upgrades using sensors

- 4.2.3 Rising labor costs and operator shortages

- 4.2.4 Government mechanization and smart-farming subsidies

- 4.2.5 Artificial Intelligence (AI) spot-spraying economics improve chemical-use payback

- 4.2.6 Growth of specialized drone and orchard spray-service fleets

- 4.3 Market Restraints

- 4.3.1 High upfront capital expenditure and financing hurdles

- 4.3.2 Limited operator and agronomy data skills

- 4.3.3 Mixed-fleet software and control-system interoperability gaps

- 4.3.4 Battery lifecycle, charging, and uptime constraints in peak spray windows

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Source of Power

- 5.1.1 Manual

- 5.1.2 Battery-Operated

- 5.1.3 Solar-Powered

- 5.1.4 Fuel-Operated

- 5.2 By Product Type

- 5.2.1 Handheld

- 5.2.2 Tractor-Mounted

- 5.2.3 Trailed

- 5.2.4 Self-Propelled

- 5.2.5 Unmanned Aerial Vehicle Sprayers

- 5.3 By Application

- 5.3.1 Field Crops

- 5.3.2 Orchards and Vineyards

- 5.3.3 Greenhouse Crops

- 5.3.4 Turf and Gardening

- 5.4 By Spray Volume Capacity

- 5.4.1 Ultra-Low Volume

- 5.4.2 Low Volume

- 5.4.3 High Volume

- 5.5 By Technology Level

- 5.5.1 Conventional

- 5.5.2 Precision and GPS-Guided

- 5.5.3 Artificial Intelligence-Enabled and Autonomous

- 5.6 By Pump Mechanism

- 5.6.1 Diaphragm Pumps

- 5.6.2 Piston Pumps

- 5.6.3 Centrifugal Pumps

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.1.4 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 Australia

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Turkey

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Nigeria

- 5.7.6.3 Rest of Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 CNH Industrial N.V.

- 6.4.3 AGCO Corporation

- 6.4.4 Kubota Corporation

- 6.4.5 Mahindra & Mahindra Limited

- 6.4.6 SZ DJI Technology Co., Ltd.

- 6.4.7 EXEL Industries

- 6.4.8 Maquinas Agricolas Jacto S.A.

- 6.4.9 AMAZONEN-WERKE H. DREYER SE & Co. KG

- 6.4.10 Bucher Industries AG

- 6.4.11 Yamaha Motor Co., Ltd.

- 6.4.12 XAG Co., Ltd.

- 6.4.13 HORSCH Maschinen GmbH

7 Market Opportunities and Future Outlook