PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073234

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073234

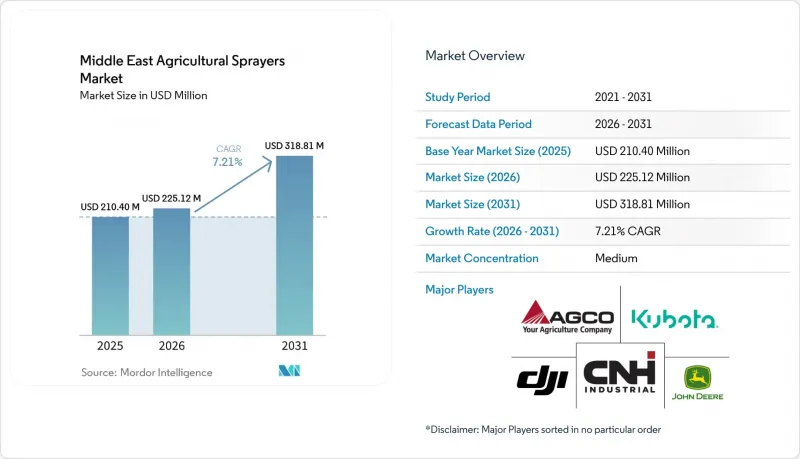

Middle East Agricultural Sprayers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the middle east agricultural sprayers market size is projected to expand from USD 210.40 million in 2025 and USD 225.12 million in 2026 to USD 318.81 million by 2031, growing at an estimated CAGR of 7.21% during 2026-2031.

This report is Segmented by Source of Power (Manual, Solar-Powered, and More), by Product Type (Handheld, Tractor-Mounted, and More), by Application (Field Crops, Orchards and Vineyards, and More), by Technology Level (Conventional, Precision and GPS Guided, and More), and by Geography (Saudi Arabia, United Arab Emirates, and More). The Market Forecasts are Provided in Terms of Value.

Middle East Agricultural Sprayers Market Trends and Insights

Precision Spraying Adoption in Water-Scarce Farms

Freshwater scarcity remains one of the strongest commercial forces driving the Middle East agricultural sprayers market, as growers in the region cannot treat spray water as a low-cost input. The supplied draft states that countries in the region face extreme water stress, and that backdrop makes precision application a practical operating choice rather than a premium feature. The same draft notes that precision agriculture can reduce water use by 20% to 30% and fertilizer use by 25% per crop cycle, thereby improving payback periods for farms managing tight water budgets. This is especially relevant in Saudi Arabia, where food self-sufficiency targets are tied to higher production efficiency, and farms are under pressure to increase output through better input control. Uniformity of spray coverage matters because waste from overlap, runoff, and drift is more costly in arid production systems than in water-abundant agricultural zones. The Middle East agricultural sprayers market is therefore shifting toward equipment that delivers measurable agronomic returns at the farm level, not just mechanical reliability or subsidy eligibility. This benefits suppliers capable of linking sprayer performance to input savings, ensuring consistent crop protection and minimizing labor intervention during application windows.

Orchard and Greenhouse Crop Expansion

Greenhouse expansion and orchard development are creating a distinct demand pattern in the Middle East agricultural sprayers market, as these crops require more controlled, targeted spray applications than broadacre field crops. The supplied draft states that Saudi Arabia installed more than 100 high-tech greenhouses between 2023 and 2025, and that this buildout was supported by Agricultural Development Fund financing for high-tech infrastructure. The commercial meaning is that growers in confined environments increasingly need compact systems, low-drift delivery, canopy penetration, and compatibility with fertigation-linked crop programs rather than large boom equipment. The United Arab Emirates is moving along a similar path under its food security strategy, where precision agriculture and controlled-environment farming are being promoted to strengthen local production under extreme climatic limits. This changes the product mix in the market because greenhouse and orchard operators often prioritize accuracy, residue control, and crop safety over tank size alone. It also underscores the relevance of air-blast systems, robotic platforms, and specialized nozzles that can operate in high-value horticulture without compromising crop quality. As a result, this driver supports both unit demand and value growth, as specialized horticulture spraying equipment typically commands a higher selling price and more stringent service requirements than standard field units.

Limited Battery Runtime During Peak Spray Windows

Battery limitations remain a practical brake on the Middle East agricultural sprayers market because high ambient temperatures reduce the operating comfort margin for electric and drone-based platforms. The supplied draft states that summer field conditions in the region regularly exceed 40°C during peak spray windows, and that this directly affects effective payload and flight duration in lithium-ion systems. The same draft notes that operators in Saudi Arabia can experience 30 to 45 minutes of interruption per battery-swap cycle during summer applications, reducing throughput when crop-protection timing is tight. Even advanced platforms such as DJI Technology Co., Ltd.'s Agras T100 still have to operate within thermal management limits despite much higher payload capability than earlier models. In practice, the limitation keeps fuel-operated and tractor-mounted systems relevant for large-area work even as farms test newer electric formats. The Middle East agricultural sprayers market, therefore, develops as a mixed-technology market rather than a rapid one-way shift to battery platforms. Until energy density, charging logistics, and heat resilience improve further, runtime limits will continue to constrain the pace of adoption of electrified spraying across the region.

Other drivers and restraints analyzed in the detailed report include:

- Drone Service Fleet Penetration in Specialty Crops

- Government Food Security and Mechanization Incentives

- Skilled Operator Shortage for Precision and Drone Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fuel-operated sprayers held 46.2% of the Middle East agricultural sprayers market share in 2025, supported by their range, runtime, and suitability for large-field operations in Saudi Arabia and the United Arab Emirates. This leadership shows that conventional power systems still fit the scale and workload of the region's main farming belts. Battery-operated, solar-powered, and manual systems remained smaller, but they served distinct use cases in greenhouses, remote plots, and low-mechanization farms.

Solar-powered sprayers are anticipated to post the fastest 8.2% CAGR during 2026-2031, reflecting their suitability for off-grid horticulture and areas where handling diesel is less attractive. The Middle East agricultural sprayers market is supporting this shift because the region has high solar irradiance and a growing need for low-energy spraying options in arid zones. Battery systems are also gaining traction in enclosed environments where emissions and noise matter more. Manual units should persist among smallholders, while fuel-operated machines are likely to remain central for high-throughput field coverage.

Tractor-mounted sprayers accounted for 41.4% of revenue in 2025, giving them the largest share in the Middle East agricultural sprayers market across product types. Their lead reflects the continued role of mechanized cereal and row-crop farming in major agricultural zones. Trailed and self-propelled units also served commercial farms that value tank capacity and boom control, while handheld systems maintained a smaller role in localized horticulture and orchard maintenance.

Unmanned aerial vehicle sprayers are anticipated to expand at a 9.8% during 2026-2031, making them the fastest-growing product group in the Middle East agricultural sprayers market. DJI Technology Co., Ltd. strengthened this category through the Agras T100 platform and wider dealer availability in late 2025. Growth is also supported by service fleet models that enable organized operators to buy in bulk and spray hard-to-access plots more efficiently. Tractor-mounted units are estimated to continue anchoring volume. However, unmanned aerial vehicle systems are transforming the approach to building commercial spraying capacity.

Complete Report Scope:

- By Source of Power

- Manual

- Battery-Operated

- Solar-Powered

- Fuel-Operated

- By Product Type

- Handheld

- Tractor-Mounted

- Trailed

- Self-Propelled

- Unmanned Aerial Vehicle Sprayers

- By Application

- Field Crops

- Orchards and Vineyards

- Greenhouse Crops

- Turf and Gardening

- By Technology Level

- Conventional

- Precision and GPS Guided

- AI-Enabled and Autonomous

- By Geography

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

List of Companies Covered in this Report:

- Deere and Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- DJI Technology Co., Ltd.

- Yamaha Motor Co., Ltd.

- EXEL Industries

- Amazonen-Werke H. Dreyer SE and Co. KG

- Kuhn Group

- Mahindra & Mahindra Ltd.

- HORSCH

- STIHL Holding AG and Co. KG

- ISEKI & CO.,LTD.

- Ecorobotix SA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Precision Spraying Adoption in Water-Scarce Farms

- 4.2.2 Orchard and Greenhouse Crop Expansion

- 4.2.3 Drone Service Fleet Penetration in Specialty Crops

- 4.2.4 Government Food Security and Mechanization Incentives

- 4.2.5 Retrofit Demand for Variable-Rate and GPS Kits

- 4.2.6 Demand for Low-Drift Application in High-Value Export Crops

- 4.3 Market Restraints

- 4.3.1 Limited Battery Runtime During Peak Spray Windows

- 4.3.2 Skilled Operator Shortage for Precision and Drone Systems

- 4.3.3 High Import Dependence for Core Components

- 4.3.4 Uneven Farm-Level Access to After-Sales Service Networks

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Source of Power

- 5.1.1 Manual

- 5.1.2 Battery-Operated

- 5.1.3 Solar-Powered

- 5.1.4 Fuel-Operated

- 5.2 By Product Type

- 5.2.1 Handheld

- 5.2.2 Tractor-Mounted

- 5.2.3 Trailed

- 5.2.4 Self-Propelled

- 5.2.5 Unmanned Aerial Vehicle Sprayers

- 5.3 By Application

- 5.3.1 Field Crops

- 5.3.2 Orchards and Vineyards

- 5.3.3 Greenhouse Crops

- 5.3.4 Turf and Gardening

- 5.4 By Technology Level

- 5.4.1 Conventional

- 5.4.2 Precision and GPS Guided

- 5.4.3 AI-Enabled and Autonomous

- 5.5 By Geography

- 5.5.1 Saudi Arabia

- 5.5.2 United Arab Emirates

- 5.5.3 Rest of Middle East

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Deere and Company

- 6.4.2 CNH Industrial N.V.

- 6.4.3 AGCO Corporation

- 6.4.4 Kubota Corporation

- 6.4.5 DJI Technology Co., Ltd.

- 6.4.6 Yamaha Motor Co., Ltd.

- 6.4.7 EXEL Industries

- 6.4.8 Amazonen-Werke H. Dreyer SE and Co. KG

- 6.4.9 Kuhn Group

- 6.4.10 Mahindra & Mahindra Ltd.

- 6.4.11 HORSCH

- 6.4.12 STIHL Holding AG and Co. KG

- 6.4.13 ISEKI & CO.,LTD.

- 6.4.14 Ecorobotix SA

7 Market Opportunities and Future Outlook