PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072897

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072897

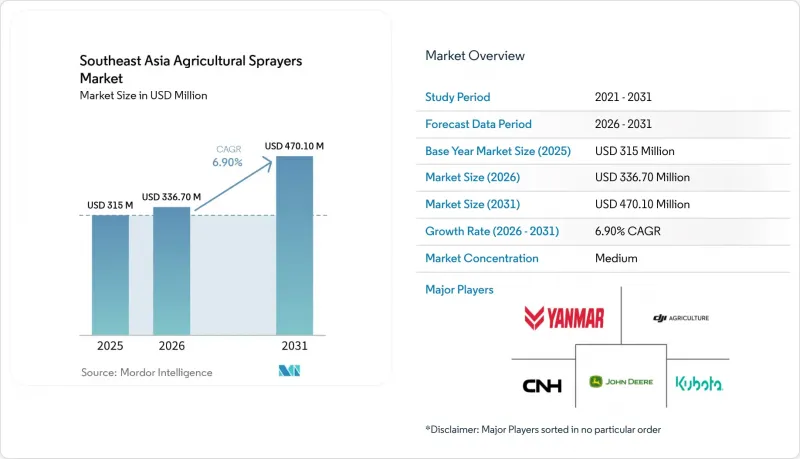

Southeast Asia Agricultural Sprayers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the southeast asia agricultural sprayers market size was valued at USD 315 million in 2025 and estimated to grow from USD 336.7 million in 2026 to reach USD 470.1 million by 2031, at a CAGR of 6.9% during the forecast period (2026-2031).

This report is Segmented by Power Source (Manual, and More), by Product Type (Handheld and More), by Application (Field Crops and More), by Spray Volume Capacity ( Ultra-Low Volume Systems, and More), by Technology Level (Conventional, and More), by Pump Mechanism (Diaphragm Pumps, and More), and Geography (Indonesia, Vietnam, and More). The Market Values are Provided in USD.

Southeast Asia Agricultural Sprayers Market Trends and Insights

Farm Labor Shortages Raise Mechanized Spraying Demand

The rural labor movement in Southeast Asia has become a lasting shift rather than a short cycle, and that is changing spraying decisions at the farm level. In several countries, growers are finding it harder to secure workers for repeated spray passes during narrow crop windows. Manual backpack spraying can require 3 to 5 workers per 50 hectares in a single application round, quickly increasing the labor burden on large farms. As a result, labor scarcity is pushing mechanized sprayers from a convenience purchase into an operating need. Dealers in Indonesia and the Philippines have reported that payback periods for powered spraying equipment are now shortening to under 18 months in higher-value crop systems, which is speeding up purchase decisions that once took years. This is lifting demand for tractor-mounted boom sprayers on medium-scale farms and for drone service contracts on fragmented or difficult terrain where ground access is limited. The Southeast Asia agricultural sprayers market is therefore benefiting from a demand base tied to labor substitution, which is more stable than demand driven only by yield improvement.

Government Mechanization Subsidies and Financing

Public financing initiatives are influencing how farms and cooperatives in Southeast Asia approach sprayer purchases. During 2025, the Philippines' Department of Agriculture's Drones4Rice program offered subsidized access to drone spraying services through hectare-based vouchers, complemented by broader mechanization funding to support the adoption of precision agriculture. In Thailand, the Smart Farmer initiatives, launched in 2025, promoted modernization and the use of precision equipment, such as GPS-guided sprayers and agricultural drones. Similarly, Indonesia's KUR Pertanian financing programs launched in 2025 aim to ease the financial burden on smallholder farmers and cooperatives investing in agricultural machinery, including mechanized spraying systems. These programs not only reduce upfront costs but also prioritize higher-performing equipment with enhanced efficiency, control, and traceability through their eligibility criteria. Consequently, subsidy and financing policies are driving changes in the product mix of the Southeast Asia agricultural sprayers market by increasing demand for advanced spraying technologies.

High Upfront Cost Of Drones And Powered Sprayers

High equipment costs continue to be a significant challenge in the Southeast Asia agricultural sprayers market. Commercial agricultural drones with payload capacities of 20-30 liters are priced between USD 8,000 and USD 20,000, depending on configuration, batteries, and accessories. This pricing restricts ownership primarily to plantations, commercial farms, and well-funded cooperatives. While drone-as-a-service models help reduce upfront investment, operators still incur substantial costs related to equipment, training, and maintenance, leading to higher service prices for small-scale growers. Consequently, advanced spraying systems are being adopted more quickly in organized farming operations, whereas manual and basic powered sprayers remain prevalent on smaller farms.

Other drivers and restraints analyzed in the detailed report include:

- Precision Agriculture and Input-Efficiency Needs

- Palm Oil and Rice Crop Protection Drives Consistent Demand

- Fragmented Smallholder Land Limits Utilization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manual sprayers accounted for 44% of the Southeast Asia agricultural sprayers market in 2025, while battery-operated sprayers are projected to grow the fastest, with a CAGR of 11.3% through 2031. Manual sprayers remain prevalent due to their affordability, particularly for farms with very small landholdings. Additionally, they are easy to repair and require minimal supporting infrastructure, which is crucial in rural areas with limited dealer networks. These factors ensure their continued relevance in various segments of the Southeast Asia agricultural sprayers market, even as advanced products gain traction.

Battery-operated sprayers are increasingly popular as lithium-ion battery costs decline, runtimes improve, and rural electrification becomes more reliable in several countries. This trend is particularly evident in Thailand and Vietnam, where public procurement initiatives and low-emission farming programs are promoting the adoption of electrified tools. Meanwhile, solar-powered sprayers are emerging as a solution for smaller hillside and terraced farming operations. Fuel-powered systems continue to serve plantation and field-crop operations, where longer runtimes and larger tank capacities are essential. This diverse mix indicates that the Southeast Asia agricultural sprayers market is not entirely transitioning away from traditional power systems but is instead incorporating new power formats alongside the established manual base.

Handheld sprayers led product demand, with a 47% share in 2025, as they remain the cheapest and most practical option for fragmented plots. Their strength reflects the reality that a large part of regional agriculture still operates under land, cash, and infrastructure constraints. That gives handheld equipment durable volume even when more advanced systems post faster growth. The Southeast Asia agricultural sprayers market, therefore, continues to be led by a large, low-cost installed base.

UAV (Unmanned Aerial Vehicle) sprayers are projected to grow at a 14.2% CAGR through 2031, making them the fastest-growing product type in the market. Much of this expansion is being driven by drone-as-a-service networks that lower the effective cost of aerial spraying for farms that cannot justify ownership. In May 2026, DJI introduced the Agras T55 with a 50-liter payload and the Agras T100 Dual Battery Spraying System at AGRITECHNICA Asia 2026 in Bangkok, extending drone capability into larger field and plantation use cases. Tractor-mounted, trailed, and self-propelled sprayers continue to serve medium and large farms that require consistent boom coverage and higher daily work rates. Over time, the overlap between advanced ground systems and Unmanned Aerial Vehicle's is likely to intensify as buyers compare not only machine price, but also labor savings, turnaround speed, and service availability.

Complete Report Scope:

- By Power Source

- Manual

- Battery-Operated

- Solar-Powered

- Fuel-Operated

- By Product Type

- Handheld

- Tractor-Mounted

- Trailed

- Self-Propelled

- Unmanned Aerial Vehicle Sprayers

- By Application

- Field Crops

- Orchards and Vineyards

- Greenhouse Crops

- Turf and Gardening

- By Spray Volume Capacity

- Ultra-Low Volume Systems

- Low-Volume Systems

- High-Volume Systems

- By Technology Level

- Conventional

- Precision and GPS-Guided

- Artificial Intelligence-Enabled and Autonomous

- By Pump Mechanism

- Diaphragm Pumps

- Piston Pumps

- Centrifugal Pumps

- By Country

- Indonesia

- Vietnam

- Thailand

- Philippines

- Malaysia

- Cambodia

- Myanmar

- Singapore

- Rest of Southeast Asia

List of Companies Covered in this Report:

- KUBOTA Corporation

- Deere and Company

- CNH Industrial N.V.

- Yanmar Holdings Co., Ltd.

- DJI Agriculture

- XAG Co., Ltd.

- Terra Drone Corporation

- STIHL Holding AG & Co. KG

- AGCO Corporation

- Jacto Inc.

- HARDI International A/S

- EXEL Industries

- Micron Sprayers Ltd.

- ASPEE Agro Equipment Pvt. Ltd.

- Goizper Group

- Yamaho Industry Co., Ltd.

- Bucher Industries AG

- Mahindra & Mahindra Ltd.

- Maruyama Mfg. Co., Inc.

- SOLO Kleinmotoren GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Farm labor shortages raise mechanized spraying demand

- 4.2.2 Government mechanization subsidies and financing

- 4.2.3 Precision agriculture and input-efficiency needs

- 4.2.4 Palm oil and rice crop protection drives consistent demand

- 4.2.5 Low-emission rice programs favor precise spray scheduling

- 4.2.6 Expansion of contract drone service networks

- 4.3 Market Restraints

- 4.3.1 High upfront cost of drones and powered sprayers

- 4.3.2 Fragmented smallholder land limits utilization

- 4.3.3 Drone-compliant pesticide formulations remain limited

- 4.3.4 Flight permits and payload rules slow field operations

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Power Source

- 5.1.1 Manual

- 5.1.2 Battery-Operated

- 5.1.3 Solar-Powered

- 5.1.4 Fuel-Operated

- 5.2 By Product Type

- 5.2.1 Handheld

- 5.2.2 Tractor-Mounted

- 5.2.3 Trailed

- 5.2.4 Self-Propelled

- 5.2.5 Unmanned Aerial Vehicle Sprayers

- 5.3 By Application

- 5.3.1 Field Crops

- 5.3.2 Orchards and Vineyards

- 5.3.3 Greenhouse Crops

- 5.3.4 Turf and Gardening

- 5.4 By Spray Volume Capacity

- 5.4.1 Ultra-Low Volume Systems

- 5.4.2 Low-Volume Systems

- 5.4.3 High-Volume Systems

- 5.5 By Technology Level

- 5.5.1 Conventional

- 5.5.2 Precision and GPS-Guided

- 5.5.3 Artificial Intelligence-Enabled and Autonomous

- 5.6 By Pump Mechanism

- 5.6.1 Diaphragm Pumps

- 5.6.2 Piston Pumps

- 5.6.3 Centrifugal Pumps

- 5.7 By Country

- 5.7.1 Indonesia

- 5.7.2 Vietnam

- 5.7.3 Thailand

- 5.7.4 Philippines

- 5.7.5 Malaysia

- 5.7.6 Cambodia

- 5.7.7 Myanmar

- 5.7.8 Singapore

- 5.7.9 Rest of Southeast Asia

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 KUBOTA Corporation

- 6.4.2 Deere and Company

- 6.4.3 CNH Industrial N.V.

- 6.4.4 Yanmar Holdings Co., Ltd.

- 6.4.5 DJI Agriculture

- 6.4.6 XAG Co., Ltd.

- 6.4.7 Terra Drone Corporation

- 6.4.8 STIHL Holding AG & Co. KG

- 6.4.9 AGCO Corporation

- 6.4.10 Jacto Inc.

- 6.4.11 HARDI International A/S

- 6.4.12 EXEL Industries

- 6.4.13 Micron Sprayers Ltd.

- 6.4.14 ASPEE Agro Equipment Pvt. Ltd.

- 6.4.15 Goizper Group

- 6.4.16 Yamaho Industry Co., Ltd.

- 6.4.17 Bucher Industries AG

- 6.4.18 Mahindra & Mahindra Ltd.

- 6.4.19 Maruyama Mfg. Co., Inc.

- 6.4.20 SOLO Kleinmotoren GmbH

7 Market Opportunities and Future Outlook