PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073014

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073014

Germany Agricultural Sprayers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

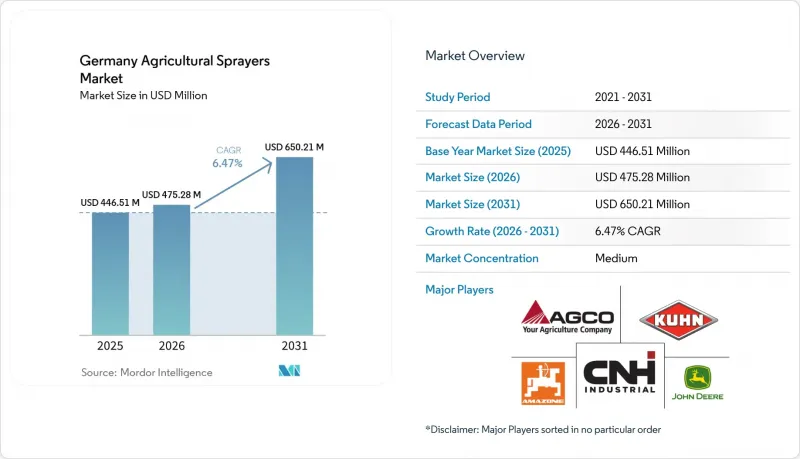

According to Mordor Intelligence, the germany agricultural sprayers market size is estimated to increase from USD 446.51 million in 2025 and USD 475.28 million in 2026 to USD 650.21 million by 2031, growing at a CAGR of 6.47% during 2026 to 2031.

This report is Segmented by Product Type (Handheld Sprayers, Tractor-Mounted Sprayers, Trailed Sprayers, and More), by Source of Power (Manual, Solar-Powered, Fuel-Operated, and More), by Application (Field Crops, Orchards and Vineyards, and More), and by Technology Level (Conventional, Precision and GPS-Guided, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Agricultural Sprayers Market Trends and Insights

Precision Spraying Mandates from Drift Reduction and Buffer-Zone Compliance

Germany's crop protection regime is giving the market a compliance-based demand base rather than a purely discretionary replacement cycle. The Niedersachsen Pflanzenschutzdienst has laid out clear requirements on drift-reduction nozzle classes, boom-height settings, and border-nozzle use, and those rules directly influence which machines and retrofit packages can remain compliant in the field. When a grower uses a nozzle that is not recognized for drift reduction, the practical effect is a wider buffer requirement and a smaller sprayable area at field edges, turning compliance into a clear financial issue rather than a simple technical one. That is why investment in certified precision hardware is moving faster than the typical equipment replacement cycle in many parts of the market. The three-year equipment inspection requirement also creates a recurring decision point, because older conventional machines that fail inspection often require costly repairs or a full replacement to remain in service. This makes demand in the Germany agricultural sprayers market steadier than in several other farm machinery categories. The policy direction is also becoming tighter, with Germany targeting a 50% reduction in plant protection product use by 2030 from the 2004 to 2023 average, which keeps precision application systems relevant to both compliance and cost control.

Labor Scarcity and Rising Custom-Application Costs

Labor shortages are increasing the value of capacity, speed, and automation across the market. Farms and contractors in Northern and Western Europe are working within shorter spray windows, and each operator hour now carries more value during peak treatment periods. This is pushing buyers toward larger booms, bigger tanks, better route efficiency, and more automated functions that let one operator cover more hectares in a day. The change is especially visible in the contractor segment, where machine utilization across multiple farms matters more than single-farm ownership economics. HORSCH Maschinen GmbH expanded its Leeb PT self-propelled line in June 2025 with a 5,000-liter entry-level model aimed at a broader contractor base, underscoring manufacturers' stronger demand for high-capacity machines at a slightly lower entry point than the premium end of the category. Labor scarcity is also supporting autonomous development in specialty crops, where navigation accuracy and repeatability can offset the shortage of trained seasonal operators. Kubota's second-generation KFAST autonomous orchard sprayer moved from field trials in Spain and Portugal toward a limited commercial launch in mid-2026, with full European availability targeted for 2027.

High Upfront Cost of Precision and Autonomous Sprayers

High purchase prices still limit how quickly the Germany agricultural sprayers market can move toward precision-heavy fleets. Studies conducted by the German Association for Technology and Structures in Agriculture on farm machinery economics indicate that direct-injection self-propelled sprayers and precision retrofit systems require significant upfront capital expenditure, slowing adoption among cost-sensitive farming operations. In Germany, large arable farms and agricultural service providers can spread these costs across more hectares, whereas smaller operations often rely on subsidies, financing programs, or equipment-sharing arrangements to justify adoption. Although increased competition is estimated to reduce entry-level pricing for technologies such as unmanned aerial vehicle platforms and precision retrofit systems, the substantial upfront capital requirements remain a significant barrier to the widespread adoption of advanced agricultural sprayers.

Other drivers and restraints analyzed in the detailed report include:

- Subsidies for Targeted Plant Protection and Drift Avoidance

- Precision Retrofits on Large Arable Farms

- Operator Know-How Gap for Advanced Precision Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tractor-mounted sprayers led product revenue with 40.7% in 2025, giving them the largest share of the Germany agricultural sprayers market. Trailed sprayers followed, then self-propelled units, while unmanned aerial vehicle sprayers and handheld models remained smaller categories shaped by narrower use cases and smaller starting bases. Their dominance is further supported by broad compatibility with existing tractors, lower ownership costs, and widespread availability across Germany.

Unmanned aerial vehicle sprayers are projected to expand at a 9.4% CAGR through 2031, giving them the fastest growth path in this segmentation and the strongest expansion in market size among product categories. Self-propelled and trailed platforms are also advancing as contractors seek higher daily coverage, while tractor-mounted systems remain central because they fit established farm fleets and field-scale economics. Handheld sprayers continue to serve smaller horticultural and greenhouse tasks rather than broad-acre field work. Growth is additionally supported by labor shortages, precision application benefits, and increasing acceptance of digital farming technologies.

Fuel-operated systems accounted for 41.2% of 2025 revenue, making them the largest power-source segment for the Germany agricultural sprayers market. Manual systems remained relevant for small-scale use, while solar-powered units remained niche, and battery-operated machines were still smaller in terms of revenue despite stronger technology momentum. Their established infrastructure, proven field performance, and ability to support intensive spraying operations continue to strengthen adoption across Germany.

Battery-operated sprayers are projected to grow at a 7.1% CAGR during the forecast period 2026-2031, the fastest rate across power-source categories in the market. This rise is supported by orchard robots, greenhouse systems, and electric specialty-crop platforms, where tank size and endurance requirements are lower than in broad-acre spraying. Fuel-operated platforms will remain central throughout the forecast period, as large booms, higher horsepower, and long working hours still favor diesel-based machines. Manual and solar-powered systems should continue to play limited, crop-specific roles rather than drive mainstream fleet demand. Increasing sustainability targets and advances in battery efficiency are also encouraging wider adoption across specialized agricultural applications.

Complete Report Scope:

- By Product Type

- Handheld Sprayers

- Tractor-Mounted Sprayers

- Trailed Sprayers

- Self-Propelled Sprayers

- Unmanned Aerial Vehicle Sprayers

- By Source of Power

- Manual

- Solar-Powered

- Fuel-Operated

- Battery-Operated

- By Application

- Field Crops

- Orchards and Vineyards

- Greenhouse Crops

- Turf and Gardening

- By Technology Level

- Conventional

- Precision and GPS-Guided

- AI-Enabled and Autonomous

List of Companies Covered in this Report:

- Amazonen-Werke H. Dreyer GmbH & Co. KG

- CNH Industrial N.V.

- Deere and Company

- AGCO Corporation

- Kuhn Group

- HORSCH Maschinen GmbH

- Lemken GmbH & Co. KG

- Kverneland AS

- Chafer Machinery Ltd

- Knight Farm Machinery Ltd

- Grim S.r.l.

- Bargam S.p.A.

- Pulverizadores Fede S.L.

- DJI Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Precision spraying mandates from drift reduction and buffer-zone compliance

- 4.2.2 Labor scarcity and rising custom-application costs

- 4.2.3 Subsidies for targeted plant protection and drift avoidance

- 4.2.4 Precision retrofits on large arable farms

- 4.2.5 Site-specific pesticide savings from direct injection and application assistants

- 4.2.6 Connected sprayers supported by digital documentation workflows

- 4.3 Market Restraints

- 4.3.1 High upfront cost of precision and autonomous sprayers

- 4.3.2 Operator know-how gap for advanced precision systems

- 4.3.3 Drone-use approvals remain narrow and multi-step

- 4.3.4 Documentation, inspection, and nozzle-compliance burden

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Handheld Sprayers

- 5.1.2 Tractor-Mounted Sprayers

- 5.1.3 Trailed Sprayers

- 5.1.4 Self-Propelled Sprayers

- 5.1.5 Unmanned Aerial Vehicle Sprayers

- 5.2 By Source of Power

- 5.2.1 Manual

- 5.2.2 Solar-Powered

- 5.2.3 Fuel-Operated

- 5.2.4 Battery-Operated

- 5.3 By Application

- 5.3.1 Field Crops

- 5.3.2 Orchards and Vineyards

- 5.3.3 Greenhouse Crops

- 5.3.4 Turf and Gardening

- 5.4 By Technology Level

- 5.4.1 Conventional

- 5.4.2 Precision and GPS-Guided

- 5.4.3 AI-Enabled and Autonomous

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-Level Overview, Market-Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Amazonen-Werke H. Dreyer GmbH & Co. KG

- 6.4.2 CNH Industrial N.V.

- 6.4.3 Deere and Company

- 6.4.4 AGCO Corporation

- 6.4.5 Kuhn Group

- 6.4.6 HORSCH Maschinen GmbH

- 6.4.7 Lemken GmbH & Co. KG

- 6.4.8 Kverneland AS

- 6.4.9 Chafer Machinery Ltd

- 6.4.10 Knight Farm Machinery Ltd

- 6.4.11 Grim S.r.l.

- 6.4.12 Bargam S.p.A.

- 6.4.13 Pulverizadores Fede S.L.

- 6.4.14 DJI Technology Co., Ltd.

7 Market Opportunities and Future Outlook