Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1685800

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1685800

Asia Pacific Freight and Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 443 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

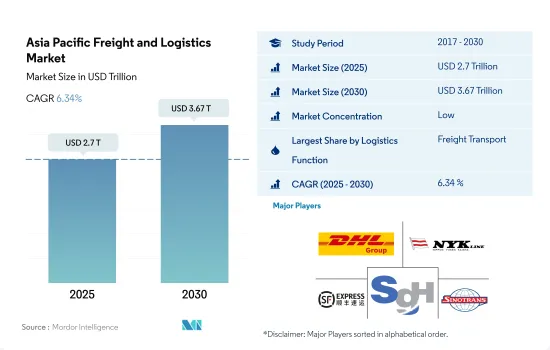

The Asia Pacific Freight and Logistics Market size is estimated at 2.7 trillion USD in 2025, and is expected to reach 3.67 trillion USD by 2030, growing at a CAGR of 6.34% during the forecast period (2025-2030).

Asian Development Bank assists the infrastructure development in the country, boosting freight transport demand

- Since March 2023, two major container truck yards in Zhejiang province, China, near Ningbo, have grappled with an excess of nearly 3,000 idle vehicles. These yards, Hengpu and Beilun, are closely tied to the port's operations. However, they have experienced a notable decline in traffic over the past two years. The accumulation of containers can be attributed to factors such as China's low storage costs, a surge in container supply during the pandemic's export boom, and a significant number of containers returning after the boom subsided.

- The Asian Development Bank (ADB) is actively supporting Pacific DMCs (Developing Member Countries) in their endeavors related to connectivity infrastructure, including planning, construction, and maintenance. Transport projects alone account for over 59% of the ADB's portfolio in the Pacific. This robust support from the ADB is fostering a more robust and sustainable growth trajectory in the Pacific region. Looking ahead, ADB's investments in the Pacific's transportation sector are projected to surpass USD 1.6 billion, with 22 projects slated for funding during 2022-2024, including a notable USD 115 million in co-financing.

Building a sustainable and resilient freight and logistics sector in the Asia Pacific region

- In India, transportation costs dominate the logistics landscape, accounting for 62% of overall logistics costs and 14% of the country's GDP. Given that diesel fuel costs make up the lion's share of transportation expenses, the adoption of zero-emission trucks (ZETs) can significantly slash fuel costs by up to 46% over the vehicle's lifespan. This has far-reaching implications for India's economy. Notably, road freight, which already accounts for over a quarter of oil import expenses, is projected to surge fourfold by 2050. By embracing ZETs, India could potentially save a staggering 838 billion liters of diesel by 2050, translating to a reduction of USD 140.17 billion in oil expenditures.

- With a confluence of factors such as limited new supply, outdated facilities, and evolving consumer preferences driven by the surge in online retail, investments in cold storage properties in the Asia-Pacific were projected to hit USD 5 billion annually by 2032. This surge is primarily driven by the escalating demand for cold chain warehousing in the region.

Asia Pacific Freight and Logistics Market Trends

Asia Pacific freight demands driven by global seaborne trade, which is triggering transport sector investments

- On May 17, 2024, a fair at Tokyo Station in Japan highlighted the growing use of high-speed passenger trains for light freight. This shift, driven by a shortage of commercial drivers and new overtime laws, has increased road delivery costs by up to 20%. Since August 2023, JR East has been running a same-day delivery service from Niigata to Tokyo using a dedicated 12-car Series E trainset. Items transported include fresh food, confectionery, drinks, flowers, precision components, and medical supplies. In September 2023, JR East launched a freight-only service on the Tohoku Shinkansen and now offers Hakobyun-branded freight services across its high-speed and Limited Express networks.

- In the 14th Five-Year Plan (2021-2025), China revealed goals for expanding its transportation network. By 2025, high-speed railways will extend to 50,000 kms, up from 38,000 kms in 2020, with 95% of cities with populations above 500,000 covered by 250-km lines. The country aims to increase its railway length to 165,000 kms, civil airports to over 270, subway lines in cities to 10,000 kms, expressways to 190,000 kms, and high-level inland waterways to 18,500 kms by 2025. The primary objective is to achieve integrated development by 2025, emphasizing advancements in the transformation of the transportation system and its contribution to GDP.

Owing to global uncertainties, crude oil prices are soaring in the Asian economies as most of them are net oil importers

- In 2023, China's crude oil imports rose by 11% to 563.99 MMT, driven by higher global oil prices due to the Russia-Ukraine War. In early 2024, imports increased by 5.1% YoY, reaching 88.31 MMT, as China capitalized on lower prices earlier. Brent futures peaked at USD 97.69 in September 2023, dropped to USD 72.29 in December, and rose to USD 84.05 by March 2024. OPEC+'s decision in March 2024 to extend output cuts has further boosted prices, raising concerns about global demand and potentially slowing China's imports in H2 2024.

- Australia's federal government will introduce a new fuel efficiency standard for passenger and light commercial vehicles starting January 1, 2025. This follows a one-month consultation period before drafting the new laws. Announced as part of the 2023 budget and linked to the EV strategy released in April 2023, the standard sets average CO2 targets for vehicle manufacturers. These targets will gradually decrease, requiring the production of more fuel-efficient and low or zero-emissions vehicles.

Asia Pacific Freight and Logistics Industry Overview

The Asia Pacific Freight and Logistics Market is fragmented, with the major five players in this market being DHL Group, NYK (Nippon Yusen Kaisha) Line, SF Express (KEX-SF), SG Holdings Co., Ltd. and SINOTRANS (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 47682

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Demographics

- 4.2 GDP Distribution By Economic Activity

- 4.3 GDP Growth By Economic Activity

- 4.4 Inflation

- 4.5 Economic Performance And Profile

- 4.5.1 Trends in E-Commerce Industry

- 4.5.2 Trends in Manufacturing Industry

- 4.6 Transport And Storage Sector GDP

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Price

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Logistics Performance

- 4.13 Major Truck Suppliers

- 4.14 Modal Share

- 4.15 Maritime Fleet Load Carrying Capacity

- 4.16 Liner Shipping Connectivity

- 4.17 Port Calls And Performance

- 4.18 Freight Pricing Trends

- 4.19 Freight Tonnage Trends

- 4.20 Infrastructure

- 4.21 Regulatory Framework (Road and Rail)

- 4.21.1 Australia

- 4.21.2 China

- 4.21.3 India

- 4.21.4 Indonesia

- 4.21.5 Japan

- 4.21.6 Malaysia

- 4.21.7 Thailand

- 4.21.8 Vietnam

- 4.22 Regulatory Framework (Sea and Air)

- 4.22.1 Australia

- 4.22.2 China

- 4.22.3 India

- 4.22.4 Indonesia

- 4.22.5 Japan

- 4.22.6 Malaysia

- 4.22.7 Thailand

- 4.22.8 Vietnam

- 4.23 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes 1. Market value in USD for all segments 2. Market volume for select segments viz. freight transport, CEP (courier, express, and parcel) and warehousing & storage 3. Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode Of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode Of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Thailand

- 5.3.8 Vietnam

- 5.3.9 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Alps Logistics

- 6.4.2 C.H. Robinson

- 6.4.3 Deutsche Bahn AG (including DB Schenker)

- 6.4.4 DHL Group

- 6.4.5 DP World

- 6.4.6 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

- 6.4.7 Expeditors International of Washington, Inc.

- 6.4.8 FedEx

- 6.4.9 Kuehne+Nagel

- 6.4.10 NYK (Nippon Yusen Kaisha) Line

- 6.4.11 SF Express (KEX-SF)

- 6.4.12 SG Holdings Co., Ltd.

- 6.4.13 SINOTRANS

- 6.4.14 United Parcel Service of America, Inc. (UPS)

7 KEY STRATEGIC QUESTIONS FOR FREIGHT AND LOGISTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.1.5 Technological Advancements

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.