PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836648

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836648

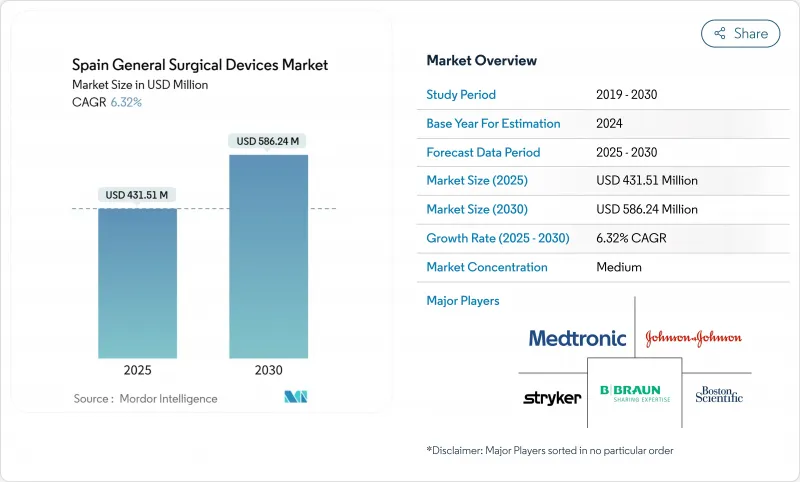

Spain General Surgical Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Spain General Surgical Devices Market size is estimated at USD 431.51 million in 2025, and is expected to reach USD 586.24 million by 2030, at a CAGR of 6.32% during the forecast period (2025-2030).

Budget expansion by the Spanish Ministry of Health, rising volumes of minimally invasive procedures, and steady investments from European recovery funds underpin near-term growth. Demand is reinforced by an aging population, a higher prevalence of chronic diseases, and a policy push that directs 69% of Madrid's health budget toward hospital care. Rapid adoption of single-use electrosurgical instruments aims to curb surgical site infections, which affect 4.51% of Spanish operative cases. Growth is further lifted by inbound surgical tourism. On the supply side, the shortage of advanced laparoscopy-trained surgeons and recurrent electrosurgical generator recalls temper the five-year outlook.

Spain General Surgical Devices Market Trends and Insights

Rising Demand for Minimally-Invasive Surgeries

Spain's surgical landscape is undergoing a paradigm shift as minimally invasive procedures gain traction across specialties, though adoption rates reveal significant regional disparities. The uneven adoption creates market opportunities for device manufacturers who can provide comprehensive training programs alongside their surgical instruments. Post-pandemic surgical recovery guidelines show that 85% of Spanish procedures can transition to outpatient settings. These trends elevate demand for specialized trocars, energy devices, and robotic staplers within the Spain general surgical devices market.

Growing Burden of Chronic Diseases Requiring Surgical Intervention

Spain's demographic transition is creating sustained demand for surgical interventions as chronic disease prevalence rises across age cohorts. This trend drives demand for specialized surgical devices that enable complex procedures in ambulatory settings. Ambulatory oncology programs in Valencia substitute 72.8% of traditional breast surgeries, promoting high-turnover device use. Electrophysiology innovations such as the Varipulse catheter respond to Spain's expanding cardiovascular workload.

Restrictive Reimbursement for Selected MIS Procedures

Spain's reimbursement framework creates significant barriers to minimally invasive surgery adoption, with DRG-based payment systems failing to adequately compensate hospitals for the higher upfront costs of advanced surgical devices. Real-world evidence programs such as RedETS progress slowly due to hospital recruitment hurdles, prolonging uncertainty around coverage expansion.

Other drivers and restraints analyzed in the detailed report include:

- Aging Population Accelerating Procedure Volumes

- Growth of Inbound Surgical Tourism to Spanish Private Hospitals

- Shortage of Advanced Laparoscopy-Trained Surgeons

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Handheld instruments captured 31.22% of Spain general surgical devices market share in 2024 owing to universal utility across open and minimally invasive cases. Disposable scissors, forceps, and retractors meet infection-control targets while remaining cost-efficient for regional hospitals. Electrosurgical platforms are expanding at a 7.98% CAGR supported by single-use pencil adoption to curb a 4.51% national surgical site infection rate. Spain general surgical devices market size for electrosurgical equipment is projected to grow steadily as recalls subside and updated instructions mitigate stroke risk.

Spain's laparoscopic towers, wound-closure kits, and novel single-use duodenoscopes create specialist niches. EXALT Model D has entered reference centers for liver transplant follow-up, proving value in high-risk cohorts. Manufacturers able to bundle disposables with training and after-sales support gain traction in procurement tenders.

Minimally invasive surgery commanded 70.14% of the Spain general surgical devices market in 2024 and is rising at a 7.45% CAGR. Ambulatory care models endorsed during the pandemic normalized outpatient pathways for up to 85% of operations. Spain general surgical devices market size for minimally invasive systems benefits from robotic console times that now average 37 minutes for unilateral inguinal hernia repair.

Open surgery preserves a 29.86% share by supporting trauma, complex oncology, and multisite procedures. Surgeons in smaller hospitals without robotic units rely on improved handheld sets and energy devices. Inter-regional training programs are being piloted to increase laparoscopic uptake, aiming to raise Spain general surgical devices market share for minimally invasive approaches in underserved provinces.

The Spain General Surgical Devices Market Report is Segmented by Product (Handheld Devices, Laparoscopic Devices, Electrosurgical Devices, Wound Closure Devices, and More), Procedure Approach (Open Surgery, and Minimally Invasive Surgery), Application (Gynecology and Urology, Cardiology, and More) and End User (Hospitals, Ambulatory Surgical Centres and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- B. Braun

- Boston Scientific

- Olympus Corp.

- Johnson & Johnson

- Smiths Group

- Medtronic

- Stryker

- Zimmer Biomet

- Karl Storz SE

- Teleflex

- Intuitive Surgical

- Arthrex

- Hologic

- Molnlycke Health Care

- Coloplast

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for minimally-invasive surgeries

- 4.2.2 Growing burden of chronic diseases requiring surgical intervention

- 4.2.3 Ageing population accelerating procedure volumes

- 4.2.4 Growth of inbound surgical tourism to Spanish private hospitals

- 4.2.5 Shift to single-use instruments to mitigate hospital-acquired-infection risk

- 4.2.6 Expansion of ambulatory surgery centres (ASCs) across autonomous communities

- 4.3 Market Restraints

- 4.3.1 Restrictive reimbursement for selected MIS procedures

- 4.3.2 Stringent regulations

- 4.3.3 Recalls & supply-chain disruptions for electrosurgical generators

- 4.3.4 Shortage of advanced laparoscopy-trained surgeons

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Handheld Devices

- 5.1.2 Laparoscopic Devices

- 5.1.3 Electrosurgical Devices

- 5.1.4 Wound-Closure Devices

- 5.1.5 Other Products

- 5.2 By Procedure Approach

- 5.2.1 Open Surgery

- 5.2.2 Minimally Invasive Surgery

- 5.3 By Application

- 5.3.1 Gynecology and Urology

- 5.3.2 Cardiology

- 5.3.3 Orthopedics

- 5.3.4 Neurology

- 5.3.5 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centres

- 5.4.3 Other End Users

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 B. Braun SE

- 6.3.2 Boston Scientific Corp.

- 6.3.3 Olympus Corp.

- 6.3.4 Johnson & Johnson (Ethicon)

- 6.3.5 Smith & Nephew PLC

- 6.3.6 Medtronic PLC

- 6.3.7 Stryker Corp.

- 6.3.8 Zimmer Biomet Holdings

- 6.3.9 Karl Storz SE

- 6.3.10 Teleflex Inc.

- 6.3.11 Intuitive Surgical Inc.

- 6.3.12 Arthrex GmbH

- 6.3.13 Hologic Inc.

- 6.3.14 Molnlycke Health Care AB

- 6.3.15 Coloplast A/S

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment