PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940731

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940731

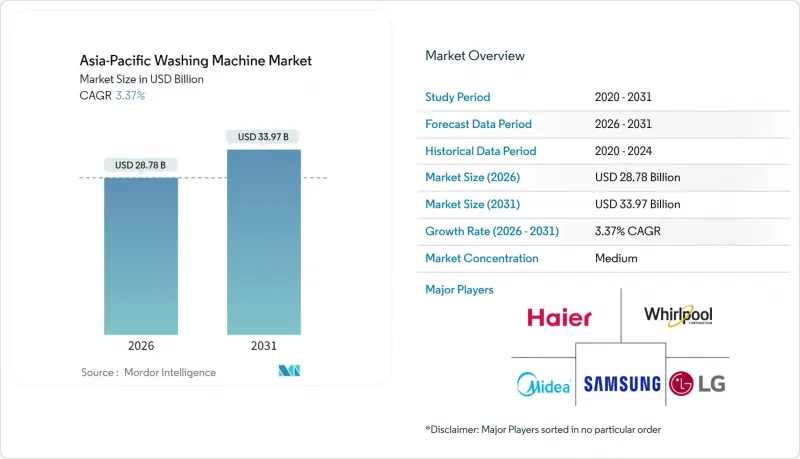

Asia-Pacific Washing Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Asia-Pacific washing machine market size in 2026 is estimated at USD 28.78 billion, growing from 2025 value of USD 27.84 billion with 2031 projections showing USD 33.97 billion, growing at 3.37% CAGR over 2026-2031.

The market's moderate pace reflects a transition from first-time purchases toward replacement demand in urban centers where saturation is high. Premiumization, driven by larger drum capacities, smart connectivity and sustainability features, underpins revenue expansion even as unit growth slows. Chinese brands consolidate share by pairing localized production in the Association of Southeast Asian Nations (ASEAN) with expansive product portfolios, while Korean manufacturers differentiate through advanced AI washing algorithms. E-commerce penetration and flexible buy-now-pay-later schemes broaden access to higher-price models for middle-income households. Government efficiency incentives and water-scarcity regulations accelerate technology upgrades toward fully automatic and front-loading machines, reinforcing a gradual mix shift toward resource-efficient designs. Intensifying competition keeps pricing disciplined, requiring vendors to extract margin through modular platforms, regional sourcing and after-sales services.

Asia-Pacific Washing Machine Market Trends and Insights

Rising Urbanization & Disposable Incomes

Rapid rural-to-urban migration reshapes demand patterns as households prioritize labor-saving appliances that match modern lifestyles. India's washing machine installations climbed sharply in fiscal 2024, and the proportional rise of dual-income families has pushed average drum capacity well beyond 8 kg. Parallel trends in Vietnam, Indonesia and the Philippines reinforce the link between middle-class formation and appliance ownership as shoppers favor compact washer-dryer combos that economize space. Urban consumers increasingly perceive the washing machine as a necessity rather than a discretionary purchase, prompting manufacturers to shift marketing themes toward hygiene and time savings. Retailers report that premium colorways and smart-phone-based controls resonate strongly with younger couples, supporting higher average selling prices. As city infrastructure improves, water-pressure stabilization and three-phase power availability expand the addressable base for fully automatic machines. The urban income effect therefore remains an enduring engine of the Asia-Pacific washing machine market.

Shift Toward Fully Automatic & Smart Machines

Convenience is paramount to time-pressed households, and AI-enabled washers align closely with this preference. Samsung's Bespoke AI Top Load Washer, launched across multiple Asian markets in 2025, detects fabric type and load weight, automatically calibrating water, detergent and cycle duration . Similar adaptive technologies are trickling down from flagship models into mid-tier price points, reinforcing consumer expectations that machines should learn usage patterns over time. Haier's three-drum design illustrates how vendors innovate around traditional hand-washing habits by enabling simultaneous separation of whites, colors and delicate fabrics. Built-in Wi-Fi modules facilitate remote monitoring, predictive maintenance alerts and energy-cost dashboards, which appeal to digitally native buyers. As 5G networks proliferate, cloud-based firmware updates will extend product lifecycles by adding features post-purchase, anchoring brand loyalty. The convergence of automation and connectivity therefore acts as a durable growth lever in the Asia-Pacific washing machine market.

Mature Penetration in Japan & South Korea

Household ownership levels in Japan and South Korea hover near universal coverage, meaning incremental demand stems primarily from replacement rather than first installation. Replacement cycles average between eight and 12 years, lengthening as product reliability improves and on-device diagnostics reduce breakdown-driven retirements. Manufacturers therefore compete fiercely on premium aesthetics, whisper-quiet operation and integrated drying to win share in a static unit base. The pursuit of Hitachi's white-goods division by Korean players signals that inorganic expansion is one of the few viable growth avenues in these saturated markets. Retailers promote subscription-style bundle services, including detergent auto-replenishment and extended maintenance, to lock in customer relationships. Yet, despite such innovations, unit volumes remain flat, dampening the overall Asia-Pacific washing machine market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Government Energy-Efficiency Subsidy Programs

- ASEAN Localization of Chinese OEM Production

- Volatile Steel & Plastic Input Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Top-load models preserved a 54.94% Asia-Pacific washing machine market share in 2025 as familiar ergonomics, quicker cycle times and lower acquisition costs resonated with middle-income consumers. Yet front-loading machines are expanding at 8.75% CAGR, propelled by superior water and energy efficiency, higher spin speeds and stackable designs that suit compact urban dwellings. Premium front loaders integrate auto-dose dispensers, steam cycles and allergen removal programs, steadily eroding the perception of complexity that historically hindered adoption. Top-load vendors respond by introducing impeller-based variants without central agitators, narrowing the gap in fabric care while preserving vertical loading convenience. Retailers report that households upgrading from semi-automatic platforms often leapfrog directly to front loaders, compressing the learning curve. In rural and peri-urban zones where water pressure remains low, top loaders maintain relevance thanks to bucket-fill options and fewer vibration concerns on uneven floors. Over the forecast period, co-existence persists, but the mix shifts gradually in favor of front-loading technology as infrastructure and awareness converge.

Fully automatic machines accounted for 71.34% of the Asia-Pacific washing machine market size in 2025, reflecting widespread preference for set-and-forget convenience. Within this category, AI-driven models that sense load weight, fabric type and detergent residue deliver tangible resource savings, appealing to eco-conscious buyers. Manufacturers layer value by adding secondary top lids for hand-wash items and built-in dryers that remove dependency on external lines. Semi-automatic units retain 22.40% share where inconsistent water supply and financial constraints prevail; these machines continue to evolve with sturdier polypropylene tubs and rust-free exteriors to withstand humid climates. Hybrid platforms emerge, allowing users to toggle between manual and auto modes, thereby easing the transition for first-time urban owners. Looking ahead, voice-control integration with smart assistants could become a standard expectation in the fully automatic sub-segment, reinforcing the technology's dominance.

The Asia-Pacific Washing Machine Market Report is Segmented by Type (Front Load, Top Load), Technology (Fully-Automatic, Semi-Automatic), End Users (Commercial, Residential), Distribution Channel (Multibrand Stores, Exclusive Stores, Online Stores, Other Distribution Channels), and Geography (India, China, Japan, Australia, South Korea, Southeast Asia, and Other). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Haier Smart Home

- LG Electronics

- Samsung Electronics

- Midea Group

- Whirlpool Corp.

- Panasonic Corp.

- Hitachi Ltd.

- Hisense Group

- Toshiba Lifestyle

- Sharp Corp.

- Bosch (Home Appliances)

- Siemens (Home Appliances)

- IFB Industries

- Godrej Appliances

- TCL Technology

- Electrolux AB

- Arcelik (Beko)

- Skyworth Group

- Daewoo Electronics

- Videocon Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising urbanisation and disposable incomes

- 4.2.2 Shift toward fully-automatic and smart machines

- 4.2.3 Government energy-efficiency subsidy programmes

- 4.2.4 ASEAN localisation of Chinese OEM production

- 4.2.5 Water-scarcity regulations favouring front-loaders

- 4.2.6 BNPL and e-commerce instalment schemes

- 4.3 Market Restraints

- 4.3.1 Mature penetration in Japan and South Korea

- 4.3.2 Volatile steel and plastic input costs

- 4.3.3 Rural power-grid instability in SE Asia

- 4.3.4 Rise of refurbishment lengthening replacement cycles

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Type

- 5.1.1 Front Load

- 5.1.2 Top Load

- 5.2 By Technology

- 5.2.1 Fully-Automatic

- 5.2.2 Semi-Automatic

- 5.3 By End Users

- 5.3.1 Commercial

- 5.3.2 Residential

- 5.4 By Distribution Channel

- 5.4.1 Multibrand Stores

- 5.4.2 Exclusive Stores

- 5.4.3 Online Stores

- 5.4.4 Other Distribution Channels

- 5.5 By Geography (Value, US$ Billion)

- 5.5.1 India

- 5.5.2 China

- 5.5.3 Japan

- 5.5.4 Australia

- 5.5.5 South Korea

- 5.5.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.7 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Haier Smart Home

- 6.4.2 LG Electronics

- 6.4.3 Samsung Electronics

- 6.4.4 Midea Group

- 6.4.5 Whirlpool Corp.

- 6.4.6 Panasonic Corp.

- 6.4.7 Hitachi Ltd.

- 6.4.8 Hisense Group

- 6.4.9 Toshiba Lifestyle

- 6.4.10 Sharp Corp.

- 6.4.11 Bosch (Home Appliances)

- 6.4.12 Siemens (Home Appliances)

- 6.4.13 IFB Industries

- 6.4.14 Godrej Appliances

- 6.4.15 TCL Technology

- 6.4.16 Electrolux AB

- 6.4.17 Arcelik (Beko)

- 6.4.18 Skyworth Group

- 6.4.19 Daewoo Electronics

- 6.4.20 Videocon Industries

7 Market Opportunities and Future Outlook

- 7.1 Ultra-low water 6-9 kg front-loaders for drought-prone Indian and Australian states

- 7.2 Pay-per-wash IoT-enabled commercial machines for co-living spaces in tier-2 Chinese and ASEAN cities