PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043893

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043893

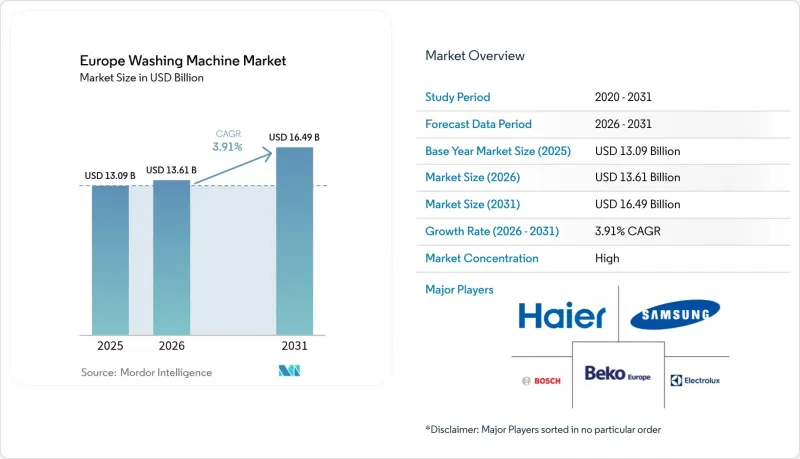

Europe Washing Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe washing machine market size is expected to grow from USD 13.09 billion in 2025 to USD 13.61 billion in 2026 and is projected to reach USD 16.49 billion by 2031, registering a CAGR of 3.91% from 2026 to 2031.

The Europe washing machine market is moving through a pivotal phase shaped by stricter European Union efficiency frameworks, faster replacement behavior, and premium features that lift average selling prices while improving lifecycle value. Product development is accelerating in response to the 2021 rescaled A to G label that raised the bar for top-tier performance, with leading models now surpassing Class A by wide margins in energy use. Front-loaders continue to anchor category dynamics, while smart, Matter-enabled control ecosystems expand consumer appeal through easier app-based operation and energy-aware cycle scheduling. Competitive focus has shifted toward durability, repairability, microplastic mitigation, and secure interoperability, as brands align with new European Union rules and use firmware to keep installed products current across longer service lives.

Europe Washing Machine Market Trends and Insights

European Union Energy Label and Ecodesign Tightening Shift Demand Toward High-Efficiency A-C Class Washers

The 2021 rescale of the energy label replaced A+++, A++, and A+ with a single A to G scale, which reset the top tier to stimulate further innovation and pushed manufacturers to deliver beyond prior thresholds. By late 2025, flagship models like Samsung's Bespoke AI Washer A-65% demonstrated class lower consumption versus the Class A minimum on the standardized test load, signaling rapid gains in core energy performance. The Ecodesign for Sustainable Products Regulation, effective July 2024, expands the policy lens to durability, repairability, recyclability, and Digital Product Passports, reinforcing a system view of lifecycle performance that favors brands able to validate and update claims over time. The European Commission's 2025-2030 Ecodesign Work Plan names washing machines among priority product groups, with expected delegated acts from 2026 and modeled household savings by 2030 that strengthen the case for efficient replacements. Leading manufacturers are commercializing higher efficiency at accessible price points, as shown by Miele's 2025 EnergyHero model positioned with 40% better economy than the Class A threshold in a widely available configuration.

Replacement Cycle Acceleration from Aging Installed Base and Post-Pandemic Usage Intensity

Installed bases across Western Europe are maturing, and many units purchased during the 2005-2015 expansion wave are now at or beyond typical replacement windows, which has led to elevated replacement activity since 2024. Field telemetry shows changing wash behavior, with Electrolux's analysis of millions of cycles in 2024 indicating a shift toward more frequent, shorter programs that add wear to key components and nudge upgrades earlier than planned. The European Union Right to Repair Directive 2024/1799 sets 10-year repair obligations and better access to spare parts and technical information, which is improving transparency and shaping buyer expectations for the next generation of units. Member states are moving to transpose the directive by July 31, 2026, and Germany introduced a national draft in January 2026 that signaled steady progress toward harmonized implementation. In the transition period, some consumers are replacing sooner to capture higher efficiency and repairability before national transposition is complete, which contributes to short-term volume support in several Western markets.

Western Europe's Near-Saturated Household Penetration Caps Volume Upsides

Most households in Western Europe already own a washing machine, which limits unit growth and tilts market momentum toward replacements and product mix upgrades rather than new installations. In markets like Germany, procurement decisions in rentals often sit with property managers who stretch replacement intervals to manage capital budgets, which flattens unit trajectories despite technology advances. Consolidation strategies, such as forming Beko Europe from Whirlpool EMEA and Arcelik's regional business, seek scale and fixed-cost leverage to operate profitably at low volume growth rates. European Union durability standards and longer-life design philosophies also lengthen service spans, which further constrain volume potential even as consumer expectations and regulation push for better performance and repairability. Brands respond by emphasizing premium features, connectivity, and lifecycle service programs that expand revenue per unit over time rather than relying on frequent replacements.

Other drivers and restraints analyzed in the detailed report include:

- Migration to Larger Drum Sizes (>=8 kg) for Bulky Textiles and Family Loads

- Repairability Scores and Modular Design Differentiation Premiumize TCO Value

- Consumer Budget Pressure and Elevated Energy Bills Defer Discretionary Upgrades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Front-load machines commanded 69.62% of the Europe washing machine market share in 2025 as consumers favored high spin efficiency, lower water use, and under-counter fitness, and within this format, smart front-load variants are projected to grow at a 5.88% CAGR through 2031 as Matter-compatible controls make integration easier across home platforms. Leading launches since 2024 showcase touch-centric control and fabric-aware programs, with Samsung bringing AI Wash+ and a 7-inch AI Home interface into its European range and linking to SmartThings for energy-aware scheduling. BSH enabled a cross-brand experience through Home Connect and early adoption of Matter, lowering setup friction for buyers who prioritize seamless device onboarding and voice assistance. LG's AI DD algorithms and connected ThinQ stack compete at similar price points, while Haier Europe's hOn application gained multi-million active users across categories, anchoring engagement at the portfolio level. Top-load maintains a niche footprint where legacy preferences persist, and twin-tub designs continue in limited rural settings that value manual control and grid flexibility, though both subtypes see constrained innovation compared to front-load ecosystems.

Historical production constraints during 2020-2022 affected the availability of connected SKUs, but supply normalization and interoperability standards now allow brands to scale smart features across broader price tiers. Software paths have become a core differentiator as updates deliver new programs such as microplastic reduction cycles and allergen removal without hardware change, which extends relevance across the service life. Security and compliance requirements under the European Union's emerging digital product framework increase the resources needed for safe connectivity, which reinforces incumbent advantages while raising hurdles for new entrants. Compact front-load combos with integrated heat-pump drying are gaining traction in urban retrofits, blending space savings with Class A complete-cycle ratings suited to apartments. Over the forecast period, the Europe washing machine market will continue to center on increasingly intelligent front-loaders as brands embed energy management and filtration capabilities that meet emerging ecodesign thresholds.

The 6-8 kg tier held 46.25% of sales in 2025, balancing weekly laundry volume, energy label performance, and standard cabinetry fit for most European households. Above-8 kg platforms are the fastest-rising capacity choice with a 4.55% CAGR outlook, gaining favor among larger families and buyers who want to clear bedding, sportswear, and outerwear in fewer cycles. Product portfolios are resetting defaults upward, with manufacturers elevating entry capacity and offering precision dosing and mixed-load optimization so that bigger drums maintain low-resource profiles on partial loads. Premium series from incumbents also pair higher capacity with filtration and hygiene features, amplifying perceived value and reinforcing upselling logic for households considering a long-term unit. Space-constrained urban buyers benefit from compact formats that still achieve 6-8 kg without compromising door clearance or under-counter integration.

Innovations like multi-drum architecture and adaptive resource controls compress cycle time for mixed garments, which reduces the time cost of larger loads. Mixed fabric programs that protect delicate fabrics at low temperatures while addressing heavy soil on synthetics are replacing older assumptions that bigger drums trade off care quality for speed. Over the forecast, manufacturers are expected to fine-tune load-detection logic to push even higher accuracy in water and detergent use, which helps maintain Class A outcomes across variable loads. As entry price points migrate toward 8 kg and beyond, buyers will see less need to compromise on capacity even in compact-floorplan homes.

The Europe Washing Machine Market Report is Segmented by Product Type (Front Load, Top Load, and Twin Tub), Capacity (Below 5 Kg, 5-8 Kg, and Above 8 Kg), Technology (Conventional, and Smart/Connected IoT), End-User (Residential, and Commercial), Distribution Channel, and Geography (United Kingdom, Germany, France, Spain, Italy, BENELUX, Nordics, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- BSH Home Appliances GmbH (Bosch, Siemens, etc.)

- Beko Europe B.V. (incl. Whirlpool EMEA brands under JV)

- Electrolux AB (incl. AEG, Zanussi)

- Haier Europe S.p.A. (incl. Candy, Hoover)

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- Miele & Cie. KG

- Whirlpool Corporation (brand presence via Beko Europe licensing)

- Hisense Europe (incl. Gorenje)

- Vestel Elektronik Sanayi ve Ticaret A.?.

- SMEG S.p.A.

- ASKO Appliances AB

- Candy Hoover Group S.r.l. (Haier Europe)

- Bauknecht Hausgerate GmbH

- Grundig Intermedia GmbH

- Midea Group (Midea Europe)

- TCL Electronics (TCL Europe)

- Ebac Ltd.

- Amica S.A.

- Indesit Company S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU Energy Label And Ecodesign Tightening Shift Demand Toward High-Efficiency A-C Class Washers

- 4.2.2 Replacement Cycle Acceleration From Aging Installed Base And Post-Pandemic Usage Intensity

- 4.2.3 Migration To Larger Drum Sizes (?8 Kg) For Bulky Textiles And Family Loads

- 4.2.4 Omnichannel Retail Scale-Up (Assortment, Delivery/Installation) Lifts Category Throughput

- 4.2.5 France's 2025 Microfiber-Filter Rule Catalyzes Pan?Eu Product Redesign And Upsell

- 4.2.6 Repairability Scores And Modular Design Differentiation Premiumize Tco Value

- 4.3 Market Restraints

- 4.3.1 Western Europe's Near-Saturated Household Penetration Caps Volume Upsides

- 4.3.2 Consumer Budget Pressure And Elevated Energy Bills Defer Discretionary Upgrades

- 4.3.3 EU Right?To?Repair Extends Product Lifetimes, Delaying Replacements

- 4.3.4 Water?Scarcity Tariffs and Wastewater Rules Constrain Intensive Cycles

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Front Load

- 5.1.1.1 With Dryers

- 5.1.1.2 Without Dryers

- 5.1.2 Top Load

- 5.1.2.1 With Dryers

- 5.1.2.2 Without Dryers

- 5.1.3 Twin Tub

- 5.1.1 Front Load

- 5.2 By Capacity

- 5.2.1 Below 5 kg

- 5.2.2 5 - 8 kg

- 5.2.3 Above 8 kg

- 5.3 By Technology

- 5.3.1 Conventional

- 5.3.2 Smart / Connected (IoT)

- 5.4 By End User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.5 By Distribution Channel

- 5.5.1 B2C / Retail

- 5.5.1.1 Multi-brand Stores

- 5.5.1.2 Exclusive Brand Outlets

- 5.5.1.3 Online

- 5.5.1.4 Other Distribution Channels

- 5.5.2 B2B / Directly from the Manufacturers

- 5.5.1 B2C / Retail

- 5.6 By Geography (Europe)

- 5.6.1 United Kingdom

- 5.6.2 Germany

- 5.6.3 France

- 5.6.4 Spain

- 5.6.5 Italy

- 5.6.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.6.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.6.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JV, Capacity, New Models)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 BSH Home Appliances GmbH (Bosch, Siemens, etc.)

- 6.4.2 Beko Europe B.V. (incl. Whirlpool EMEA brands under JV)

- 6.4.3 Electrolux AB (incl. AEG, Zanussi)

- 6.4.4 Haier Europe S.p.A. (incl. Candy, Hoover)

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 LG Electronics Inc.

- 6.4.7 Miele & Cie. KG

- 6.4.8 Whirlpool Corporation (brand presence via Beko Europe licensing)

- 6.4.9 Hisense Europe (incl. Gorenje)

- 6.4.10 Vestel Elektronik Sanayi ve Ticaret A.?.

- 6.4.11 SMEG S.p.A.

- 6.4.12 ASKO Appliances AB

- 6.4.13 Candy Hoover Group S.r.l. (Haier Europe)

- 6.4.14 Bauknecht Hausgerate GmbH

- 6.4.15 Grundig Intermedia GmbH

- 6.4.16 Midea Group (Midea Europe)

- 6.4.17 TCL Electronics (TCL Europe)

- 6.4.18 Ebac Ltd.

- 6.4.19 Amica S.A.

- 6.4.20 Indesit Company S.p.A.

7 Market Opportunities & Future Outlook

- 7.1 Built-In, Shallow-Depth Front-Loaders For Space-Constrained Urban Retrofits

- 7.2 Factory-Integrated Microfiber Capture + Microplastic-Aware Eco-Cycles as Premium Differentiators

- 7.3 Service-Based Extended Warranties and Certified Refurbishment Aligned to Right-To-Repair