PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044294

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044294

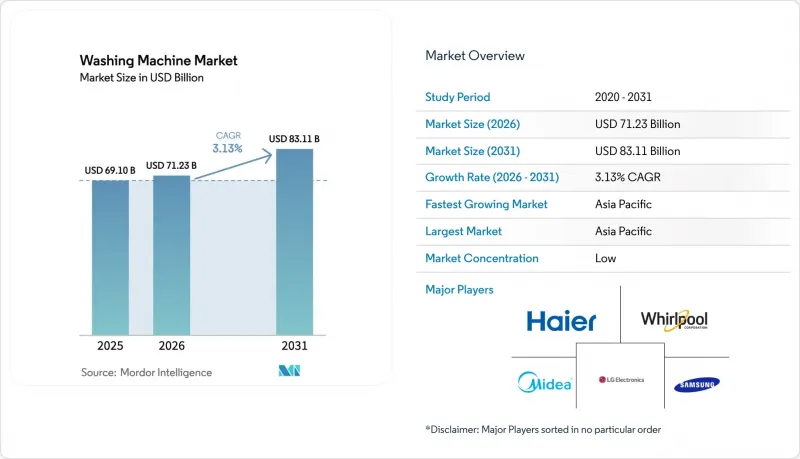

Washing Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The global washing machine market size is expected to grow from USD 69.10 billion in 2025 to USD 71.23 billion in 2026 and is forecast to reach USD 83.11 billion by 2031, growing at a CAGR of 3.13% over 2026-2031.

Front-loaders continue to hold the lead on installed base and resource efficiency, while top-loaders gain momentum on faster cycles and price positioning in value-conscious segments. Demand is shaped by rule-tightening in energy and water performance, microfibre filtration policies that nudge compliant designs, and right-to-repair frameworks that extend lifecycles and shift value into after-sales services. Digital features that automate dosing, sense fabrics, and schedule around dynamic tariffs reinforce premiumization, particularly when tied to brand ecosystems. Omnichannel distribution broadens reach in Asia-Pacific, where online sales scale quickly, encouraging localized inventory and faster order-to-install timelines to close the last-mile gap for bulky appliances. Compliance-led differentiation and smart-grid integration are strengthening the upgrade case for advanced models in the global washing machine market.

Global Washing Machine Market Trends and Insights

Regulatory-Driven Replacement Toward High-Efficiency, Low-Water Washers

Standards and labeling frameworks are aligning toward lower energy and water footprints, which is bringing forward the replacement of older models and favoring premium, efficient designs. In the European Union, the rescaled A-G energy label and associated product requirements continue to ratchet down consumption, with the 2030 benchmark guiding new product development and marketing claims toward measurable household savings. This is expanding the addressable pool for efficient front-loaders that meet strict test procedures and verified performance documentation. In the United States, state-level initiatives on microfibre filtration, such as New York's enacted bill requiring high-capture filters for fibers of defined size thresholds, increase compliance costs yet differentiate early movers that integrate proven filtration designs. As brands align product portfolios with these requirements, consumers see clearer life-cycle value from energy and water savings, which supports higher average selling prices without stalling adoption. These policy signals are translating into clearer upgrade pathways across price tiers in the global washing machine market.

Premiumization via Smart/Connected Features and Ecosystem Bundling

Feature sets that automate detergent dosing, identify fabric type, and schedule cycles around off-peak tariffs are expanding the price-to-value equation for connected washers and combos. Samsung's Bespoke AI Laundry lineup ties AI Energy Mode and fabric-sensing logic to SmartThings, enabling automated energy optimization and cycle orchestration within a broader home ecosystem. Whirlpool has introduced a FreshFlow venting approach and advanced sealing to limit odors, while pairing with app features that reduce manual interventions and minimize rewash scenarios. LG's AI Direct Drive 2.0 and ThinQ bring fabric detection, motion-control logic, and remote cycle control to multiple form factors, which is positioning connected washers as a clear step-up path from conventional models. Ecosystem bundling across laundry, refrigeration, and air conditioning strengthens lock-in effects for brands that harmonize software, accessories, and optional subscriptions. These premium attributes underpin a durable upgrade narrative in the global washing machine market as connectivity becomes an expected capability in higher-tier SKUs.

Input Cost Volatility and Supply Chain Disruptions Pressuring Margins

Electronics content in connected washers makes them sensitive to component lead times and logistics, which can swing sharply during tight supply conditions. Manufacturers with deeper integration in controls and boards, or with localized board production, can shorten procurement cycles and curb air freight exposure, which stabilizes unit economics. Where original equipment makers diversify production footprints and supplier bases, they mitigate tariff and freight volatility that can otherwise erode gross margins. Large players that disclose on-time-in-full metrics and resilience actions note more predictable throughput for launch cycles that rely on specific motor controllers, sensors, and connectivity modules. Such measures help maintain consistent availability of premium SKUs while defending price points during component cost spikes. The net effect is a sustained incentive to localize critical subassemblies and spread risk in the global washing machine market.

Other drivers and restraints analyzed in the detailed report include:

- Omnichannel and Online Retail Accelerating Access and Price Discovery

- Emerging Microfibre Filtration Mandates Favoring Compliant Designs

- Right-to-Repair and Longevity Policies Elongating Replacement Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Front-load washers commanded 65.92% of the global washing machine market share in 2025, driven by superior resource efficiency and higher final spin speeds that reduce residual moisture before drying. Top-loaders are projected to post a 4.62% CAGR through 2031 as value buyers seek shorter cycles and easier mid-cycle access, especially in markets where water costs and floor space are less constraining. The global washing machine market is channeling product development into washer-dryer combos with ventless heat-pump systems that cut energy use and eliminate the need for external vents in apartments. Flagship models from leading brands now integrate AI features that detect soil level and fabric type, which helps reduce rewash rates and strengthens the upgrade story in mid-to-premium price bands. In showrooms, transparent energy-label comparisons and live spin-speed demos help articulate differences between front-load and top-load designs for buyers who want performance clarity at the point of sale. Compliance with water and energy thresholds is easier with front-load designs, while top-loaders are improving via impeller redesigns, higher spin speeds, and smarter cycle logic. The global washing machine market benefits as both formats modernize to meet efficiency and convenience goals.

Cycle-speed expectations and form-factor constraints are reshaping assortments, with washer-dryer combos emerging as a space-saving path to premium energy performance. Samsung's combo line illustrates how a single-drum product with heat-pump drying can achieve significant energy reductions while fitting urban apartments, and pricing strategies that include periodic discounts and financing lower adoption barriers for first-time buyers of combo systems. Brands are also building use-case features, such as enhanced odor control or pet-hair cycles, to address specific household needs without requiring add-on equipment. Regulatory expectations remain a key design anchor, with front-loaders natively aligned to stricter water factors and top-loaders catching up via mechanical and software refinements. Proposed recalibrations of water-use standards in the United States could create more room for cycle-time optimization, which would support the resurgence of top-load adoption where speed and simplicity matter most. Across formats, integrated AI that tunes dosage and motion patterns by fabric class is becoming a baseline differentiator, which continues to shape premium product positioning in the global washing machine market.

The 6-8 kg capacity bracket accounted for 45.81% of 2025 sales, balancing space efficiency and family load flexibility at accessible price points. The segment is projected to grow at a 4.91% CAGR through 2031 as more dual-income households consolidate laundry time into fewer cycles, and as urban floor plans favor 24-27-inch platforms that fit standard closets and laundry alcoves. The global washing machine market size for the 6-8 kg segment is set to rise with this steady volume expansion and consistent upgrade to automatic dosing and faster spins near the segment's mid-tier. Compact formats below 5 kg remain a niche for dorms and single-occupancy homes, valued for portability but constrained by lower spin performance and manual fill trade-offs. At the high end, above-8-kg units have increased traction among larger households and light-commercial environments that benefit from one-and-done loads and robust motors.

Feature upgrades are cascading down into the 6-8 kg tier, including dosing reservoirs sized for multiple washes and mobile apps that simplify maintenance prompts and cycle selection. Bosch's 24-inch compact portfolio demonstrates how connected features and auto-dosing can be adapted for small-space use, which widens premium appeal in dense cities. Water-scarce regions steer toward front-load designs within the 6-8 kg tier due to lower consumption per kilogram, while water-abundant or price-sensitive markets still mix in higher-capacity top-loaders. Australia's updated energy-rating requirements are raising the visibility of cycle time and power draw on labels, which nudges makers toward higher spin speeds to reduce drying time without compromising wash quality. As OEMs localize more components and testing, lead times keep improving for private-label and regional brands that rely on stable 6-8 kg volumes as their core. The global washing machine industry continues to size and tune this segment for mainstream adoption while reserving specialized features for super-capacity and combo models.

The Global Washing Machine Market Report is Segmented by Product Type (Front Load, Top Load, and Twin Tub), Capacity (Below 5 Kg, 5-8 Kg, and Above 8 Kg), Technology (Conventional, and Smart/Connected), End-User (Residential, and Commercial), Distribution Channel, and Geography. The Market Forecasts are Provided in Terms of Value (USD Billion).

Geography Analysis

Asia-Pacific led with 40.71% share in 2025 and is projected to grow at a 3.39% CAGR through 2031 as urbanization, digital commerce, and localized manufacturing capacity align across major economies. China remains the region's largest country market and is transitioning from volume replacement toward premium-connected features as households trade up to AI-enabled models. India's strong consumption momentum supports broader adoption of fully automatic washers and localized product lines that address variable water pressure and hard water, aided by investments in domestic component manufacturing and printed circuit board capacity to reduce lead times. Online shares across key Asia-Pacific markets are high and rising, which prompts brands to localize inventory and partner for installation to maintain delivery speed and quality. Australia's updated GEMS framework elevates the visibility of energy and water performance and program time on labels, which supports broader adoption of front-loaders and heat-pump combos in water-stressed regions. The global washing machine market benefits from scale effects across Asia-Pacific as component ecosystems and logistics densify.

Europe is the second-largest region by contribution and is one of the fastest-growing developed markets due to stringent energy labeling and rising repairability expectations that redefine premium value. The European Union's rescaled A-G labels set a clear hierarchy for energy performance, and the 2030 benchmark for energy use guides engineering targets for next-generation washers. Western Europe's retailer assortments are moving early toward compliant SKUs to avoid stranded inventory risk, which rewards early movers that pre-comply with upcoming rules on filtration or repairability. The United Kingdom and Nordic countries show strong momentum for heat-pump drying and efficient laundry solutions where electricity tariffs favor reduced consumption, and households increasingly consider life-cycle costs when selecting appliances. Large European makers disclose alignment with repairability and longevity goals, while assembling connected features that integrate with common smart-home platforms. This policy and retailer structure sustains steady premiumization in the global washing machine market across Europe.

North America maintains a balanced growth profile at roughly the global pace, with steady replacement cycles and rising expectations for smart-home compatibility. Leading brands have announced capacity and technology investments in United States plants to strengthen supply resilience and support product lines tied to renewable energy sourcing at sites. Demand-response ready features are gaining visibility as utilities expand dynamic tariffs and rebate eligibility for connected appliances that automate off-peak operation. In Canada and the United States, brand stores and multi-brand retailers continue to anchor the path to purchase for larger capacity models, while direct-to-consumer channels layer in flexible financing and accelerated fulfillment. Mexico's role in North American manufacturing networks has expanded, offering tariff-resilient options and shorter logistics legs for regional demand. This regional ecosystem supports the long-run installed base and upgrade cadence in the global washing machine market.

- Whirlpool Corporation

- Haier Smart Home Co., Ltd.

- LG Electronics Inc.

- Samsung Electronics Co., Ltd.

- BSH Hausgerate GmbH

- Electrolux AB

- Panasonic Corporation

- Midea Group Co., Ltd.

- Hisense Home Appliances Group Co., Ltd.

- Arcelik A.S.

- Miele & Cie. KG

- Toshiba Lifestyle Products & Services Corporation

- Hitachi Global Life Solutions, Inc.

- Fisher & Paykel Appliances Ltd.

- Godrej & Boyce Mfg. Co. Ltd. (Godrej Appliances)

- IFB Industries Ltd.

- Sharp Corporation

- Winia Electronics Co., Ltd.

- Alliance Laundry Systems LLC

- Dexter Laundry, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory-Driven Replacement Toward High-Efficiency, Low-Water Washers

- 4.2.2 First-Time Adoption Among Expanding Middle-Class Households In Asia-Pacific

- 4.2.3 Premiumization Via Smart/Connected Features and Ecosystem Bundling

- 4.2.4 Omnichannel and Online Retail Accelerating Access and Price Discovery

- 4.2.5 Emerging Microfibre Filtration Mandates Favoring Compliant Designs

- 4.2.6 Grid-Interactive, Demand-Response Capable Washers Unlocking Utility Incentives

- 4.3 Market Restraints

- 4.3.1 Price Sensitivity And Informal/Used Appliance Competition in Emerging Markets

- 4.3.2 Input Cost Volatility And Supply Chain Disruptions Pressuring Margins

- 4.3.3 Water Scarcity Constraints And Wastewater Fees Dampening Usage in Stressed Regions

- 4.3.4 Right-To-Repair And Longevity Policies Elongating Replacement Cycles

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Front Load

- 5.1.1.1 With Dryers

- 5.1.1.2 Without Dryers

- 5.1.2 Top Load

- 5.1.2.1 With Dryers

- 5.1.2.2 Without Dryers

- 5.1.3 Twin Tub

- 5.1.1 Front Load

- 5.2 By Capacity

- 5.2.1 Below 5 kg

- 5.2.2 5 - 8 kg

- 5.2.3 Above 8 kg

- 5.3 By Technology

- 5.3.1 Conventional

- 5.3.2 Smart / Connected (IoT)

- 5.4 By End-User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.5 By Distribution Channel

- 5.5.1 B2C/Retail

- 5.5.1.1 Multi-brand Stores

- 5.5.1.2 Exclusive Brand Outlets

- 5.5.1.3 Online

- 5.5.1.4 Other Distribution Channels

- 5.5.2 B2B/Directly from the Manufacturers

- 5.5.1 B2C/Retail

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 Canada

- 5.6.1.2 United States

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 South-East Asia

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East & Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East & Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Whirlpool Corporation

- 6.4.2 Haier Smart Home Co., Ltd.

- 6.4.3 LG Electronics Inc.

- 6.4.4 Samsung Electronics Co., Ltd.

- 6.4.5 BSH Hausgerate GmbH

- 6.4.6 Electrolux AB

- 6.4.7 Panasonic Corporation

- 6.4.8 Midea Group Co., Ltd.

- 6.4.9 Hisense Home Appliances Group Co., Ltd.

- 6.4.10 Arcelik A.S.

- 6.4.11 Miele & Cie. KG

- 6.4.12 Toshiba Lifestyle Products & Services Corporation

- 6.4.13 Hitachi Global Life Solutions, Inc.

- 6.4.14 Fisher & Paykel Appliances Ltd.

- 6.4.15 Godrej & Boyce Mfg. Co. Ltd. (Godrej Appliances)

- 6.4.16 IFB Industries Ltd.

- 6.4.17 Sharp Corporation

- 6.4.18 Winia Electronics Co., Ltd.

- 6.4.19 Alliance Laundry Systems LLC

- 6.4.20 Dexter Laundry, LLC

7 Market Opportunities & Future Outlook

- 7.1 Microfibre-Capture Compliant Washers and Retrofit Filters

- 7.2 Utility-Integrated, Demand-Response Ready Smart Washers

- 7.3 OEM-Certified Refurbishment and Subscription Models