PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034982

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034982

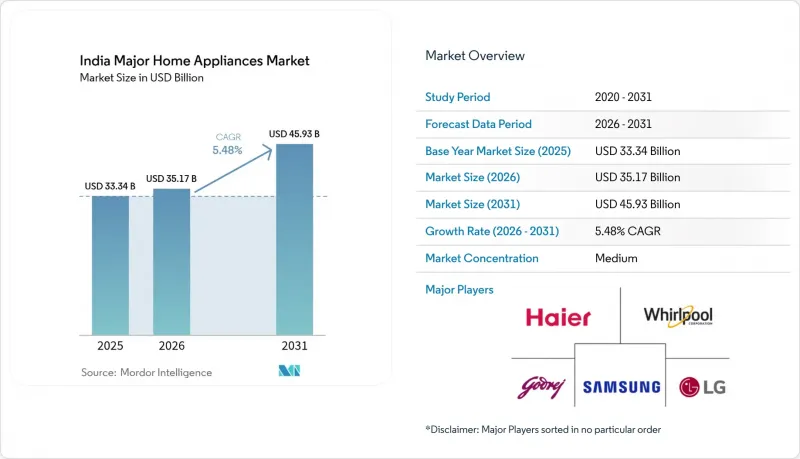

India Major Home Appliances - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The India Major Home Appliances market size is expected to grow from USD 33.34 billion in 2025 to USD 35.17 billion in 2026 and is forecast to reach USD 45.93 billion by 2031 at 5.48% CAGR over 2026-2031.

Solid policy support, premiumization, and omnichannel retail adoption underscore the long-term growth outlook for the India Major Home Appliances market. Production Linked Incentives (PLI) shorten import-led cost disadvantages, while stricter energy-efficiency norms stimulate faster replacement cycles and justify higher average selling prices. Rising disposable incomes, rapid urban nuclear-family formation, and last-mile electrification collectively unlock new unit sales, especially across tier-2 and tier-3 cities where baseline penetration remains low. Competitive intensity is rising because domestic firms scale capacity to capture PLI benefits and global brands launch AI-driven product portfolios to hold share in the India Major Home Appliances market.

India Major Home Appliances Market Trends and Insights

Government PLI & Domestic-Manufacturing Push

The PLI allocation of INR 6,238 crore reinvigorates supply-side dynamics by doubling indigenous content in air conditioners from 25% to 55% and trimming cost disadvantages from 18% to 12%. Forty-two approved applicants, including component specialists for heat exchangers and compressors, collectively committed INR 3,898 crore in greenfield capacity. The incentive design rewards incremental sales rather than capacity creation, ensuring market-driven expansion and discouraging idle assets. Localization reduces working-capital lockups tied to long import cycles, improves just-in-time manufacturing, and positions India as an export base for South Asian markets that require tariff-free sourcing within regional trade pacts. Yet semiconductor constraints remain a weak link, urging coordinated execution of the USD 10 billion India Semiconductor Mission to provide microcontrollers and inverter chips at scale. High-pressure policy coordination among central ministries, state governments, and industry associations sustains momentum and ensures the India Major Home Appliances market continues to internalize value previously lost to imports.

Rising Disposable Income & Premiumization

Average urban household income is projected to rise from USD 7,050 in 2024 to USD 9,640 by 2030, lifting wallet share for discretionary durable purchases. Consumer surveys reveal that 62% of first-time buyers opt directly for energy-efficient, smart-enabled appliances rather than starting with entry-level SKUs. Volume spikes in 9 kg+ washing machines-up 91% in 2024-underscore how dual-income families prioritize capacity and convenience. Samsung's goal to derive 50% of its India revenue from appliances and displays within three years signals broader corporate confidence in premium tiers. AI-powered refrigerators leverage predictive cooling algorithms, lowering annual energy usage by up to 20% and restricting food wastage-tangible benefits that rationalize higher ASPs. As electric-vehicle adoption pushes residential electricity tariffs toward time-of-day pricing, intelligent appliances that shift consumption to off-peak hours become even more attractive, creating a virtuous feedback loop of technology adoption and energy savings within the India Major Home Appliances market.

Semiconductor & Compressor Supply Vulnerabilities

India currently imports almost 75% of the semiconductors used in inverter drives, Wi-Fi modules, and smart-display panels embedded in appliances. Freight surcharges and geopolitical tensions inflate lead-times to 18-20 weeks, prompting manufacturers to hold extra inventory and thus tie up working capital. Compressor manufacturing, meanwhile, is dominated by three local companies meeting just 40% of aggregate demand, forcing OEMs to rely on imports from Thailand and China. The mismatch caused a 7-10% unit cost spike during the 2024 summer peak, a margin squeeze not fully reversible through retail price increases. Medium-term mitigation includes backward integration by global brands into variable-speed compressor lines and joint-venture fabs under the India Semiconductor Mission. Failure to close these bottlenecks could lower utilization rates in newly built PLI-funded plants, undermining the competitiveness of the India Major Home Appliances market.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Norms Spurring Replacement Sales

- Rapid Urban Nuclear-Family Formation

- High GST Slabs on Select Appliances

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The India Major Home Appliances market size attributable to air conditioners reached USD 6.42 billion in 2025 and will increase at a 6.39% CAGR through 2031. Elevated outdoor temperatures, rising heat-wave frequency, and a growing middle class accelerate inverter-based split AC adoption, with 1-ton and 1.5-ton variants comprising 68% of sales. Manufacturers now introduce R32 and R290 refrigerant options to satisfy global warming-potential norms, further differentiating premium SKUs.

Refrigerators remain the volume anchor with 29.02% 2025 market share; single-door models dominate rural zones, whereas frost-free bottom-freezer units gain urban share. Dishwashers, though under 4% household penetration, enjoy 18% annual growth within metros as domestic help costs rise. Microwave-convection combination ovens find traction via bundled recipe apps that simplify Indian cuisine presets, enabling younger consumers to personalize cooking routines. Emerging robotic kitchen assistants demonstrate first-mover advantage for brands that can localize voice support to Hindi, Tamil, and Telugu, thereby broadening user appeal across linguistic demographics. Each product innovation strengthens brand recall and fortifies ecosystem lock-in, pivotal for lifetime-value maximization in the India Major Home Appliances market.

The India Major Home Appliances Market is Segmented by Product (Refrigerators, Freezers, Washing Machines, Dishwashers, Ovens, Air Conditioners, Other Major Home Appliances), Distribution Channel (Multi-Brand Stores, Exclusive Brand Outlets, Online, Other Distribution Channels), and Geography (North India, South India, East India, West India). Forecasts are Expressed in USD.

List of Companies Covered in this Report:

- Blue Star

- Bosch-Siemens (Home Appliances) India

- Crompton Greaves Consumer

- Electrolux AB

- Godrej Appliances

- Haier India

- Hitachi Air-Conditioning India

- IFB Industries

- Kent RO Systems (dishwashers)

- LG Electronics India

- Lloyd (Havells)

- Midea-Carrier India

- Onida

- Panasonic India

- Samsung India

- Voltas-Beko

- Whirlpool of India

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid urban nuclear-family formation

- 4.2.2 Rising disposable income & premiumisation

- 4.2.3 Government PLI & domestic-manufacturing push

- 4.2.4 Energy-efficiency norms spurring replacement sales

- 4.2.5 India-specific IoT ecosystems (e.g., BharOS appliances)

- 4.2.6 Last-mile rural electrification unlocking new demand

- 4.3 Market Restraints

- 4.3.1 Semiconductor & compressor supply vulnerabilities

- 4.3.2 Fragmented cold-chain limiting freezer uptake

- 4.3.3 High GST slabs on select appliances

- 4.3.4 Low consumer credit penetration outside Tier-1 cities

- 4.4 Industry Value Chain Analysis

- 4.5 Porterss Five Forces Analysis

- 4.5.1 Threat Of New Entrants

- 4.5.2 Bargaining Power Of Suppliers

- 4.5.3 Bargaining Power Of Buyers

- 4.5.4 Threat Of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights Into The Latest Trends And Innovations In The Market

- 4.7 Insights On Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, Etc.) In The Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Refrigerators

- 5.1.2 Freezers

- 5.1.3 Washing Machines

- 5.1.4 Dishwashers

- 5.1.5 Ovens (Incl. Combi & Microwave)

- 5.1.6 Air Conditioners

- 5.1.7 Other Major Home Appliances

- 5.2 By Distribution Channel

- 5.2.1 Multi-Brand Stores

- 5.2.2 Exclusive Brand Outlets

- 5.2.3 Online

- 5.2.4 Other Distribution Channels

- 5.3 By Geography

- 5.3.1 North India

- 5.3.2 South India

- 5.3.3 East India

- 5.3.4 West India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Blue Star

- 6.4.2 Bosch-Siemens (Home Appliances) India

- 6.4.3 Crompton Greaves Consumer

- 6.4.4 Electrolux AB

- 6.4.5 Godrej Appliances

- 6.4.6 Haier India

- 6.4.7 Hitachi Air-Conditioning India

- 6.4.8 IFB Industries

- 6.4.9 Kent RO Systems (dishwashers)

- 6.4.10 LG Electronics India

- 6.4.11 Lloyd (Havells)

- 6.4.12 Midea-Carrier India

- 6.4.13 Onida

- 6.4.14 Panasonic India

- 6.4.15 Samsung India

- 6.4.16 Voltas-Beko

- 6.4.17 Whirlpool of India

7 Market Opportunities & Future Outlook

- 7.1 Energy-efficient models dominate consumer preferences

- 7.2 E-commerce and D2C accelerate appliance sales