PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035133

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035133

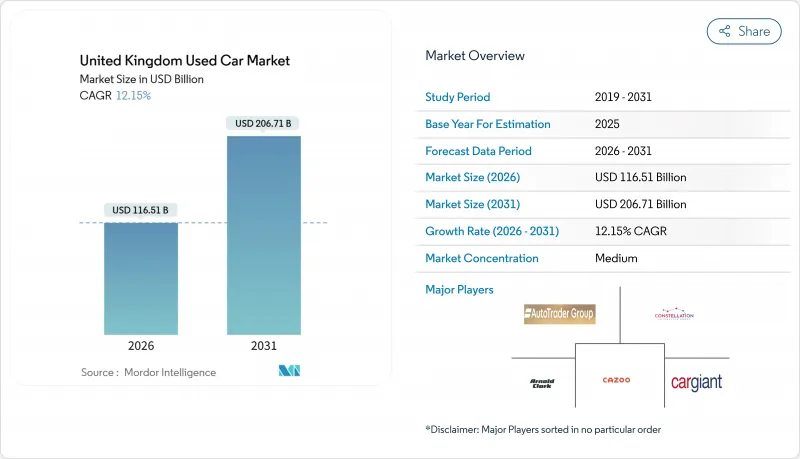

United Kingdom Used Car - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United Kingdom used car market size stands at USD 116.51 billion in 2026 and is projected to reach USD 206.71 billion by 2031, translating into a 12.15% CAGR over the forecast period.

Growth is driven by faster fleet renewal triggered by urban emissions zones, the rise of trusted certified pre-owned programs, and the rapid migration of transactions to digital marketplaces. Buyers are gravitating toward flexible ownership models, such as subscription services, while residual-value guarantees on battery-electric vehicles (BEVs) help alleviate depreciation concerns and accelerate the adoption of electrification. Competitive dynamics are intensifying as franchised dealer groups, auction majors, and pure-play online platforms deploy data-driven pricing tools that compress days-to-sale and widen geographic reach, according to Investegate. Persistent interest-rate headwinds and elevated used-vehicle prices remain the principal brakes on volume recovery. Yet, structurally tighter new-car output keeps near-new stock scarce, supporting pricing power.

United Kingdom Used Car Market Trends and Insights

Rapid Uptake of Online-Only Marketplaces and Click-and-Deliver Models

Auto Trader dominates marketplace browsing time, leveraging instant-offer tools and guaranteed part-exchange options to streamline sales for private sellers. Carwow uses a dealer-bidding engine, introducing transparent auction-style pricing to its retail inventory. This strategy not only earns recognition through Top-Rated badges for low complaint rates but also strengthens digital trust. Real-time pricing engines, such as Vertu Insights, enhance stock turnover and increase profit margins. Mobile-centric buyers now expect home delivery within a short timeframe, prompting even traditional groups to embrace an omnichannel approach.

ULEZ, ZEZ and Clean-Air Zones Accelerating Fleet Turnover Toward Newer Used Cars

London's Ultra-Low Emission Zone now covers every borough, raising compliance to 96% by mid-2024 and pushing owners of older engines to trade into Euro 6-compliant used stock. Similar clean-air charging schemes in Birmingham, Manchester, and Scotland's four Low Emission Zones levy daily fees that erode the economics of running vehicles aged eight years or more. The resulting demand shifts split the United Kingdom's used car market, with compliant petrol and diesel cars attracting urban premiums. At the same time, non-compliant stock is either relocated to rural areas or scrapped. The policy cascade lifts transaction velocity and underpins residual values for younger vehicles. Regional rollouts, including Cardiff's planned 2026 zone, are expected to maintain the regulatory tailwind through the forecast horizon.

High Interest-Rate Environment Raising Finance Costs for Buyers

Although the Bank of England eased the base rate to 4.25% by May 2025, for prime borrowers, used-car APRs hover at moderate levels, while subprime rates can reach significantly higher percentages . This results in an increase in monthly costs on standard loans. The Finance & Leasing Association has reported a decline in used-car finance volumes, citing the exit of entry-level buyers from the market. To sustain sales, dealers are absorbing rate buy-downs, which in turn pressures their gross margins. Additionally, negative equity on older ICE vehicles is making trade-ins more challenging.

Other drivers and restraints analyzed in the detailed report include:

- OEM-Backed Certified Pre-Owned Programs Boost Buyer Trust and Prices

- Attractive Residual-Value Guarantees on Used BEVs and Hybrids

- Used-Car Prices Surge as New-Car Output Faces Crunch

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Independent, unorganized vendors, traditionally dominant in rural catchments and lower price bands, accounted for 58.23% of the United Kingdom's used car market size in 2025. However, their market share is steadily declining due to increasing compliance pressures. The CMA's Phase 2 investigation into Constellation's acquisition of Aston Barclay underscores the increasing regulatory scrutiny of auction consolidations. Larger players leverage scale advantages in data analytics, captive finance, and logistics, leaving smaller, fragmented traders increasingly at risk of losing market share.

Organized dealers captured 41.77% of the United Kingdom's used car market share in 2025; yet, the group is expected to add volume at a 12.82% CAGR through 2031, as certified-pre-owned schemes and nationwide digital storefronts build trust and convenience. This structural tailwind positions organized operators to undercut smaller rivals on nearly-new stock while monetizing finance and service add-ons.

Vehicles aged 3-5 years accounted for 34.28% of the United Kingdom used car market share in 2025, reflecting the traditional depreciation "sweet spot." However, the United Kingdom used car market demand for 0-2 year models is rising fastest at a 12.43% CAGR through 2031, driven by short-cycle fleet returns and demonstrator oversupply.

Younger inventory benefits from full OEM warranty and eligibility for certified programs, supporting premium pricing and faster turns. In contrast, cars older than eight years face mounting urban access fees and higher insurance costs, which suppress their resale values despite their appeal to cash buyers outside city centers. Dealers are increasingly channeling high-mileage or non-compliant stock to export markets, thereby protecting domestic residuals.

Petrol cars still led the United Kingdom's used car market share in 2025, with 53.34%. Yet, BEVs are sprinting ahead with a 19.23% CAGR as infrastructure improves and warranty-supported battery health reports reduce buyer anxiety. The United Kingdom used car market size tied to electrified powertrains is expected to more than triple by 2031.

Diesel's retreat quickens under Clean-Air Zone charges, while hybrids enjoy a hedge against range and refueling constraints. Export demand for diesel units to less-regulated regions partly cushions domestic price falls, but the long-term trajectory remains downward.

The United Kingdom Used Car Market is Segmented by Vendor Type (Organized and Unorganized), Vehicle Age (0-2 Years, 3-5 Years, and More), Fuel Type (Petrol, Diesel, and More), Body Type (Hatchback, Sedan, and More), and Sales Channel (Online, and More), Ownership (First-Owner, and More), Price Band (Less Than USD 7, 000, and More) and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Auto Trader Group plc

- Constellation Automotive Group Ltd

- Arnold Clark Automobiles Ltd

- Cazoo Group Ltd

- Car Giant Ltd

- Lookers plc

- Pendragon plc (CarStore)

- Vertu Motors plc

- Motorpoint Group plc

- Manheim (Cox Automotive U.K.)

- Sytner Group Ltd

- Inchcape plc

- TrustFord (Ford Retail Ltd)

- Jardine Motors Group U.K. Ltd

- AvailableCar Ltd

- Carwow Ltd

- Motors.co.uk Ltd

- Aramis Group

- Peter Vardy Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 ULEZ, ZEZ and Clean-Air Zones Accelerating Fleet Turnover Toward Newer Used Cars

- 4.2.2 OEM-Backed Certified-Pre-Owned Programs Boosting Buyer Trust and Prices

- 4.2.3 Rapid Uptake of Online-Only Marketplaces and Click-and-Deliver Models in the U.K.

- 4.2.4 Subscription-Based Used-Car Schemes Increasing Repeat Demand Cycles

- 4.2.5 Attractive Residual-Value Guarantees on Used BEVs and Hybrids

- 4.2.6 Insurance Telematics Making Older Vehicles Less Cost-Competitive

- 4.3 Market Restraints

- 4.3.1 High Interest-Rate Environment Raising Finance Costs for Used-Car Buyers

- 4.3.2 Used-Car Prices Surge as New-Car Output Faces Crunch

- 4.3.3 ICE Faces Residual-Value Uncertainty Ahead of Upcoming Petrol/Diesel Ban

- 4.3.4 Data-Privacy Concerns Around Connected-Car Ownership Transfers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD), Volume (Units))

- 5.1 By Vendor Type

- 5.1.1 Organized

- 5.1.2 Unorganized

- 5.2 By Vehicle Age

- 5.2.1 0 - 2 Years

- 5.2.2 3 - 5 Years

- 5.2.3 6 - 8 Years

- 5.2.4 More than 8 Years

- 5.3 By Fuel Type

- 5.3.1 Petrol

- 5.3.2 Diesel

- 5.3.3 Hybrid

- 5.3.4 Battery Electric

- 5.3.5 Plug-in Hybrid

- 5.3.6 Other Alt-Fuels (CNG/LPG)

- 5.4 By Body Type

- 5.4.1 Hatchback

- 5.4.2 Sedan

- 5.4.3 Sport Utility Vehicle (SUV)

- 5.4.4 Multi-Purpose Vehicle (MPV)

- 5.5 By Sales Channel

- 5.5.1 Online

- 5.5.2 Offline - Franchised Dealers

- 5.5.3 Offline - Independent Dealers

- 5.5.4 Private-to-Private

- 5.6 By Ownership Type

- 5.6.1 First-Owner

- 5.6.2 Second-Owner

- 5.6.3 Third-or-More Owners

- 5.7 By Price Band

- 5.7.1 Less than USD 7,000

- 5.7.2 USD 7,001 - USD 15,000

- 5.7.3 USD 15,000 - USD 30,000

- 5.7.4 More than 30,000

- 5.8 By Region

- 5.8.1 England

- 5.8.2 Scotland

- 5.8.3 Wales

- 5.8.4 Northern Ireland

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Auto Trader Group plc

- 6.4.2 Constellation Automotive Group Ltd

- 6.4.3 Arnold Clark Automobiles Ltd

- 6.4.4 Cazoo Group Ltd

- 6.4.5 Car Giant Ltd

- 6.4.6 Lookers plc

- 6.4.7 Pendragon plc (CarStore)

- 6.4.8 Vertu Motors plc

- 6.4.9 Motorpoint Group plc

- 6.4.10 Manheim (Cox Automotive U.K.)

- 6.4.11 Sytner Group Ltd

- 6.4.12 Inchcape plc

- 6.4.13 TrustFord (Ford Retail Ltd)

- 6.4.14 Jardine Motors Group U.K. Ltd

- 6.4.15 AvailableCar Ltd

- 6.4.16 Carwow Ltd

- 6.4.17 Motors.co.uk Ltd

- 6.4.18 Aramis Group

- 6.4.19 Peter Vardy Ltd

7 Market Opportunities & Future Outlook