PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044258

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044258

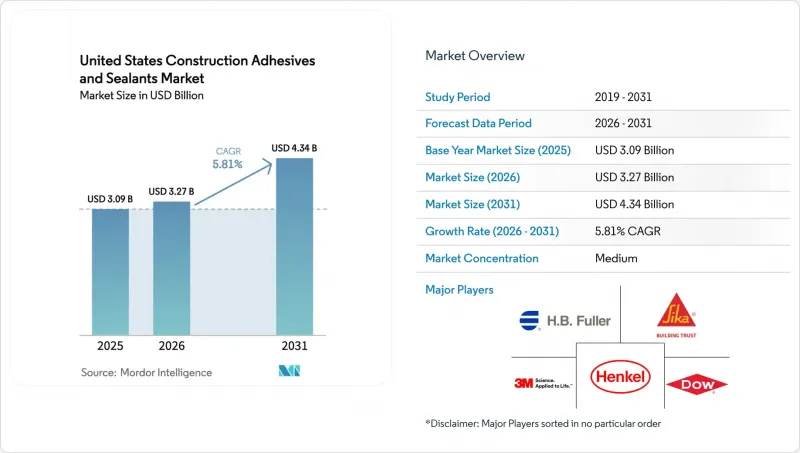

United States Construction Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United States Construction Adhesives and Sealants Market size is expected to increase from USD 3.09 billion in 2025 to USD 3.27 billion in 2026 and reach USD 4.34 billion by 2031, growing at a CAGR of 5.81% over 2026-2031. Implementation of tighter energy-code mandates, the steady rise of off-site modular construction, and fast-maturing bio-based polyurethane chemistries are expanding product demand as stakeholders pursue higher performance and lower embodied carbon targets. Water-borne technology already leads the United States construction adhesives & sealants market, and continued VOC (Volatile Organic Compound) caps under South Coast AQMD (Air Quality Management District) Rule 1168 keep shifting specifications away from solvent-borne systems. Rapid-cure reactive systems are gaining ground because they shorten installation cycles in panelized builds, while silicone and polyurethane chemistries remain indispensable for high-movement facades that must withstand seismic loading and UV exposure. Competitive positioning now hinges on research and development for bio-content, accelerated test approvals, and regional capacity expansions that avert supply bottlenecks in high-growth Sunbelt and Pacific Northwest corridors.

United States Construction Adhesives And Sealants Market Trends and Insights

Tight Energy-Code Adoption Driving High-Performance Building Envelopes

The 2024 edition of the International Energy Conservation Code cut allowable air-leakage to 0.25 cfm/ft2 at 75 Pa, a 38% tightening versus 2021; Washington, Massachusetts, and California codified those limits between July 2024 and January 2025. Low-modulus polyurethane and hybrid SMP formulations, therefore, replaced mechanical fasteners to avoid thermal bridging, especially in climate zones demanding R-value upgrades under ASHRAE 90.1-2022. Adhesives exceeding 25 pli peel strength and 150 psi shear are now baseline requirements, sidelining older acrylic mastics. Demand acceleration for high-elongation products translates directly into higher average selling prices that support incremental research and development.

Rapid Shift to Off-Site Modular Construction

Modular techniques captured 6.2% of the United States non-residential starts in 2025, up from 4.8% in 2020, as developers raced to cut schedules and labor risk. Moisture-cure reactive hot-melts enable 80% bond strength within 90 minutes, keeping throughput near 12 wall cassettes per hour. H.B. Fuller's Swift-Tak 1357 delivers this profile, letting factories eliminate overnight curing and reclaim 1,200 ft2 of floor space. Bathroom-pod builders also migrate toward water-resistant polyurethane and epoxy systems that pass ASTM D1151 humidity aging.

VOC-Content Caps Under South Coast AQMD Rule 1168

Rule 1168 drives universal sub-70 g/L VOC limits for most construction adhesives in the Los Angeles basin; OTC states adopted matching caps by 2025, covering 38% of demand. Reformulation costs of USD 120,000-180,000 per SKU deterred mid-tier suppliers, increasing the United States construction adhesives & sealants market concentration around multinationals. Longer tack-free times for water-borne acrylics extend schedules, creating pushback on fast-track jobs.

Other drivers and restraints analyzed in the detailed report include:

- Green-Label Credit Compliance (LEED v4.1/IBU)

- Emergence of Bio-Based Polyurethane Chemistries

- Skilled-Labor Shortage Delaying Adhesive Application

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, acrylic resins represented 28.89% of overall adhesive value, a level grounded in ceramic-tile mastics and drywall joint compounds where cost efficiency and clean-up ease are paramount. This share positions acrylics as the single largest component within the United States Construction Adhesives and Sealants market. The segment's elasticity remains limited, yet Tile Council of North America specifications keep acrylic-latex modifiers mandatory in thin-set mortars. Polyurethane grades are advancing at a 6.24% CAGR during the forecast period (2026-2031), leveraging superior elongation for curtain-wall and dissimilar-substrate bonding. Epoxy adhesives preserve niche status in high-modulus anchoring and crack injection work.

Acrylic innovation points toward lower-VOC and faster-tack water emulsions, aligning with Rule 1168. VAE/EVA copolymers possess quick tack and hot-melt compatibility, a fit for laminated door skins moving at 200 lf/min. Silicone and cyanoacrylate resins occupy specialist corners, fire-stop flashing, and instant-bond repairs. Continued raw-material price swings for acrylate monomers could nudge specifiers toward polyurethane alternatives, yet installer familiarity provides a durable moat.

The United States Construction Adhesives and Sealants Market Report is Segmented by Adhesives Resin (Acrylic, Cyanoacrylate, Epoxy, Polyurethane, Silicone, VAE/EVA, and Other Resins), by Adhesives Technology (Hot-Melt, Reactive, Solvent-Borne, UV-Cured, and Water-Borne), and by Sealants Resin (Polyurethane, Epoxy, Acrylic, Silicone, Polysulfide, and Other Resins). The Market Size and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema Group

- Dow

- Franklin International.

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.

- MAPEI S.p.A.

- Pecora Corporation

- RPM International Inc.

- Sika AG

- Soudal Inc.

- Tremco

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tight energy-code adoption driving high-performance building envelopes

- 4.2.2 Rapid shift to off-site modular construction

- 4.2.3 Green-label credit (LEED v4.1/IBU) compliance requirements

- 4.2.4 Emergence of bio-based polyurethane chemistries

- 4.2.5 On-site 3-D printing of concrete structures

- 4.3 Market Restraints

- 4.3.1 VOC-content caps under South Coast AQMD Rule 1168

- 4.3.2 Skilled-labor shortage delaying adhesive application

- 4.3.3 Fire-test re-certification costs for innovative chemistries

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Adhesives Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 By Adhesives Technology

- 5.2.1 Hot-Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-Borne

- 5.2.4 UV-Cured

- 5.2.5 Water-Borne

- 5.3 By Sealants Resin

- 5.3.1 Polyurethane

- 5.3.2 Epoxy

- 5.3.3 Acrylic

- 5.3.4 Silicone

- 5.3.5 Polysulfide

- 5.3.6 Other Resins

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global-level overview, Market-level overview, Core segments, Financials, Strategic information, Market rank/share, Products & services, Recent developments)

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Dow

- 6.4.4 Franklin International.

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Huntsman International LLC

- 6.4.8 Illinois Tool Works Inc.

- 6.4.9 MAPEI S.p.A.

- 6.4.10 Pecora Corporation

- 6.4.11 RPM International Inc.

- 6.4.12 Sika AG

- 6.4.13 Soudal Inc.

- 6.4.14 Tremco

- 6.4.15 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment