PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066666

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066666

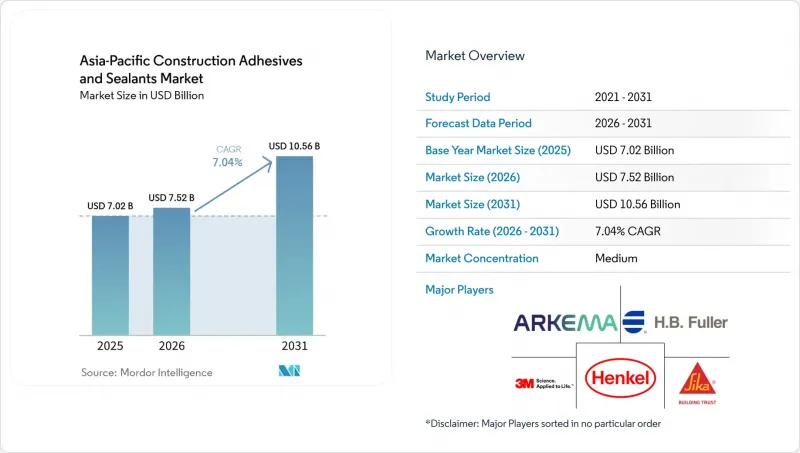

Asia-Pacific Construction Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific construction adhesives and sealants market size was valued at USD 7.02 billion in 2025 and is estimated to grow from USD 7.52 billion in 2026 to reach USD 10.56 billion by 2031, at a CAGR of 7.04% during the forecast period (2026-2031).

This report is Segmented by Resin Type (Acrylic, Cyanoacrylate, Epoxy, and More), Technology (Water-Borne, Solvent-Borne, and More), Application (Flooring and Tiling, Roofing, and More), End-Use Sector (Residential, Commercial, and More), and Geography (Australia, China, India, Japan, Vietnam, Thailand, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Construction Adhesives And Sealants Market Trends and Insights

Infrastructure Megaproject Pipeline Across APAC

Thailand's USD 36 billion land-bridge will specify marine-grade polysulfide sealants for tidal-zone piers and tunnel linings. Vietnam's Thu Thiem 4 Bridge used expansion-joint systems that endured 100,000 compression cycles, a performance now replicated in metro-viaduct projects. BMI forecasts regional construction spending to climb from USD 2,429 billion in 2025 to USD 2,580.4 billion in 2026, led by India at 6.2% growth. Automated adhesive-dispensing systems are trimming on-site labor by 30% and lifting bond-strength consistency by 40%, raising entry barriers for smaller blenders. Collectively, megaproject pipelines anchor long-run visibility that sustains the Asia-Pacific Construction Adhesives and Sealants market.

Green-Building Codes Boosting Low-VOC Sealants Demand

China's GB 33372-2020 sets differentiated VOC ceilings, and Beijing's DB11/1983-2022 tightens limits to 50 g/L for interior applications, effectively banning solvent-borne mastics in state projects. Hong Kong's Construction Industry Council certification caps exterior sealant emissions at 100 g/L, favoring water-borne acrylics and modified-silane polymers. Japan's 4VOC voluntary registry lets architects select products with verified emission data, dovetailing with JPY 208.8 billion (USD 1.395 billion) allocated for seismic upgrades in FY2025. Singapore's Green Building Masterplan requires 80% of new builds to achieve Green Mark Platinum by 2030, incentivizing Environmental Product Declarations that multinational suppliers can readily furnish. These codes accelerate substitution toward water-borne chemistries, expanding the Asia-Pacific Construction Adhesives and Sealants market.

Volatile Petrochemical Feedstock Prices

Ethylene margins slid 50% in H2 2024 as capacity additions outpaced polymer demand. A 90% shipping-lane closure scenario in the Strait of Hormuz during mid-2025 forced South Korean crackers to idle units, slashing regional olefin supply. Adhesive formulators cannot hedge beyond six months because forward curves lack liquidity, so spot price spikes squeeze margins. Bio-naphtha pilots in Thailand and Malaysia trade at 30-40% premiums, confining uptake to green-building showcases. Feedstock volatility, therefore, tempers margin expansion inside the Asia-Pacific Construction Adhesives and Sealants market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of Modular and Prefab Construction

- E-Commerce Warehousing Fuelling Industrial Flooring Adhesives

- Stricter VOC Limits on Solvent-Borne Technologies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane captured 25.14% of 2025 revenue, anchoring its leadership across roofing, insulation, and flooring. Silicone is set to outpace at 7.18% CAGR during the forecast period (2026-2031) because supertall facades require +-25% movement plus UV stability. Neutral-cure profiles avert corrosion on anodized aluminum, making them the default for curtain-wall contractors. Epoxy remains a niche, but its 3,500 PSI tensile strength enables weld-free prefab steel connections, saving hot-work permits and insurance surcharges.

Volume dynamics pivot on sustainability. Dow's carbon-neutral silicone service provides Life-Cycle-Assessment documentation that eases Green Mark Platinum submissions, tilting premium projects toward silicone. Acrylics dominate luxury-vinyl-tile installations, especially in e-commerce warehouses where pressure-sensitive tack accelerates handover. Commodity VAE dispersions in dry-mix mortars face price pressure as Chinese overcapacity drags margins. Cyanoacrylates and hot-melts stay confined to modular-factory lines where instant tack justifies price premiums. Each resin tier, therefore, targets discrete value pools inside the Asia-Pacific Construction Adhesives and Sealants market.

Sealant (1K and 2K) combined for 44.37% of 2025 sales, reflecting reliance on weatherproofing and structural glazing in seismic-prone geographies. One-component silicones are prevalent in residential facades due to application simplicity, whereas two-component systems prevail on bridges and tunnels that demand extended pot life. The Asia-Pacific Construction Adhesives and Sealants market share for water-borne adhesives is poised to climb at a CAGR of 7.32% during the forecast period (2026-2031). Beijing's procurement standards already enforce near-zero-VOC interiors, pushing contractors toward water-borne acrylics.

Reactive chemistries, moisture-cure polyurethanes, and two-part epoxies are stealing share in prefab factories where six-minute handling strength boosts throughput. Hot-melts remain small because outdoor durability concerns persist, but they retain popularity in furniture edge-banding. Enforcement gaps between tier-1 and interior provinces create dual pricing structures: solvent-borne acrylics linger in rural zones, while city-center towers specify water-borne or modified-silane systems. This policy gradient will continue to shape technology substitution inside the Asia-Pacific Construction Adhesives and Sealants market.

List of Companies Covered in this Report:

- 3M

- Aica Kogyo Co., Ltd.

- Arkema

- Ashland Inc.

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- ITW Performance Polymers

- Momentive

- Pidilite Industries Ltd.

- PPG Industries Inc.

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Group

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Infrastructure megaproject pipeline across APAC

- 4.1.2 Green-building codes boosting low-VOC sealants demand

- 4.1.3 Rapid growth of modular and prefab construction

- 4.1.4 E-commerce warehousing fuelling industrial flooring adhesives

- 4.1.5 Substitution of mechanical fasteners by structural adhesives

- 4.1.6 Ageing building stock retrofits in mature Asia-Pacific economies

- 4.2 Market Restraints

- 4.2.1 Volatile petrochemical feedstock prices

- 4.2.2 Stricter VOC limits on solvent-borne technologies

- 4.2.3 Silicone monomer supply disruptions in China

- 4.2.4 Skilled labour shortage for advanced application methods

- 4.3 Value Chain Analysis

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Bargaining Power of Buyers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Others

- 5.2 By Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Reactive

- 5.2.4 Hot-melt

- 5.2.5 Sealants (1K and 2K)

- 5.3 By Application

- 5.3.1 Flooring and Tiling

- 5.3.2 Roofing

- 5.3.3 Wall Panels and Facades

- 5.3.4 Insulation and Weatherproofing

- 5.3.5 Infrastructure Joints (bridges and tunnels)

- 5.4 By End-use Sector

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.4.4 Infrastructure

- 5.5 By Country

- 5.5.1 Australia

- 5.5.2 China

- 5.5.3 India

- 5.5.4 Indonesia

- 5.5.5 Japan

- 5.5.6 Malaysia

- 5.5.7 Singapore

- 5.5.8 South Korea

- 5.5.9 Thailand

- 5.5.10 Vietnam

- 5.5.11 Philippines

- 5.5.12 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/(%)Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Aica Kogyo Co., Ltd.

- 6.4.3 Arkema

- 6.4.4 Ashland Inc.

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 ITW Performance Polymers

- 6.4.9 Momentive

- 6.4.10 Pidilite Industries Ltd.

- 6.4.11 PPG Industries Inc.

- 6.4.12 Shin-Etsu Chemical Co., Ltd.

- 6.4.13 Sika AG

- 6.4.14 Soudal Group

- 6.4.15 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment