PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066668

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066668

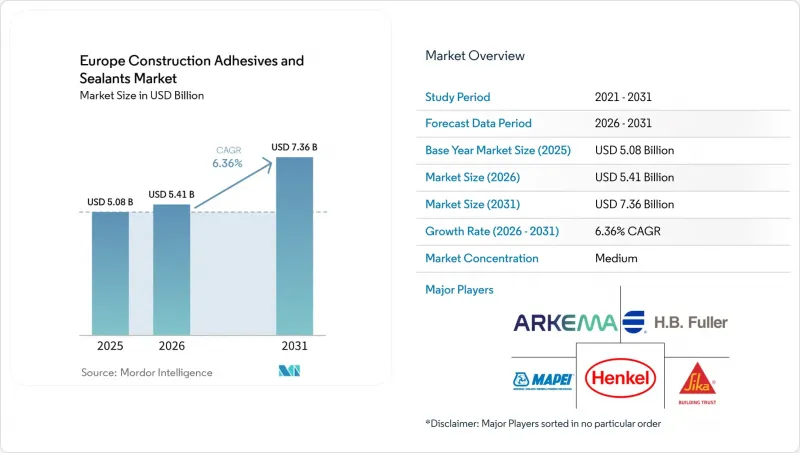

Europe Construction Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe construction adhesives and sealants market size was valued at USD 5.08 billion in 2025 and is estimated to grow from USD 5.41 billion in 2026 to reach USD 7.36 billion by 2031, at a CAGR of 6.36% during the forecast period (2026-2031).

This report is Segmented by Resin Type (Acrylic, Cyanoacrylate, Epoxy, and More), Technology (Water-Borne, Solvent-Borne, and More), Application (Flooring and Tiling, Roofing, and More), End-Use Sector (Residential, Commercial, and More), and Geography (France, Germany, Italy, Russia, Spain, United Kingdom, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Construction Adhesives And Sealants Market Trends and Insights

Rapid Shift to Low-VOC, REACH-Compliant Formulations

The revised CLP entered force on 10 December 2024 and applies from 1 July 2026, adding new hazard classes and digital label rules that compress reformulation windows for D4, D5, and D6 siloxanes. MAPEI's solvent-free silylated polymer, ULTRABOND ECO S955 1K, already meets EMICODE EC1 Plus with TVOC below 60 µg/m3 after 28 days, demonstrating market readiness for low-VOC flooring jobs. The Construction Products Regulation (CPR) revision, effective 8 January 2026, embeds the Digital Product Passport (DPP) and whole-life carbon accounting into CE marking, rewarding early movers who complete third-party verification ahead of public-tender deadlines. National embodied-carbon caps, such as Denmark's 7.1 kg CO2e/m2/year in 2025, tightening to 5.8 kg in 2029, are spreading to Germany and the Netherlands, accelerating the displacement of solvent-borne sealants.

Post-Pandemic EU Renovation Wave (Renovation Wave Initiative)

The European Union (EU) targets energy upgrades for 35 million buildings by 2030, channeling EUR 66 billion in public funding through 2029. The Energy Performance of Buildings Directive (EPBD) recast requires whole-life carbon assessments for new buildings above 1,000 m2 from 2028 and for all new construction from 2030. Germany's Climate & Transformation Fund allocates EUR 12.5 billion (USD 14.59 billion) to rail infrastructure and prioritizes residential retrofits, pushing construction output from a 4.9% contraction in 2024 to 2.5% growth in 2026, the region's fastest rebound. Uptake in France and Spain trails due to fragmented contractor networks, yet improved financing tools are lifting quarter-on-quarter retrofit volumes. Labor remains the choke point because only 25% of construction workers hold at least one green skill, prompting formulators to emphasize error-tolerant, primer-less products that reduce installer training time.

Volatility in Isocyanate and Silicone Feedstock Prices

Wacker Chemie flagged an additional 25% price rise effective 1 February 2026, while silicone DMC (Dimethyl Carbonate) and EVA (Ethylene-Vinyl Acetate) indices rose 28% and 22%, respectively. Converters scramble for eight-to-twelve-week delivery slots versus four-to-six in 2024, carrying extra inventory that absorbs working capital. Isocyanate plants averaged 75-80% utilization through 2025 on weak demand and high energy costs, leaving 2026 stabilization dependent on curtailing Chinese exports. Persistently higher European electricity prices, two to three times U.S. Gulf Coast benchmarks, erode competitiveness and push formulators toward long-term supply contracts.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Off-Site and Modular Construction

- Rising Demand for High-Performance Facade Systems

- Russia-Ukraine War Driven Logistics Disruptions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylic resins maintained 26.75% Europe Construction Adhesives and Sealants market share in 2025, led by flooring and tiling, where open time and water cleanup offset lower bond strength. Silicone's 6.28% CAGR through 2031 stems from mandatory structural glazing in embodied-carbon-capped projects and the phase-out of D4-D6 siloxanes from mid-2026. Polyurethanes remain indispensable for bridge-joint movement capability above +-25% and UV-exposed roofing membranes. Epoxies govern industrial flooring but lose momentum because of long cure cycles and VOC (Volatile Organic Compound) levels incompatible with EMICODE EC1 Plus. Niche streams such as bio-based polyurethanes, backed by BASF's SUSBOARD, and alkali-activated blends trialed in 3D-printed concrete, remain under a very low share of Europe Construction Adhesives and Sealants market size through 2031. Early silicon reformulators gain specification lock-in with facade engineers seeking carbon-neutral EPDs.

Acrylic's installed volume base ensures slow erosion even as water-borne modifiers prune VOC content. Silicone suppliers hedge platinum exposure through recycling catalysts and long-term supply deals. Polyurethane innovators exploit primer-less tech to cut installer hours in labor-scarce regions, boosting uptake in modular factories. Epoxy vendors re-position high-solids, fast-cure grades for extreme-wear logistics floors, while cyanoacrylates persevere in repair kits.

Sealants covered 42.37% of 2025 revenue, ranging from 1K hybrids for facade mullions to 2K polysulfides for runway joints. Water-borne adhesives are expected to expand at a 6.57% CAGR during the forecast period (2026-2031), propelled by Q4 2025 EU VOC ceilings and EMICODE EC1 Plus labeling that caps TVOC at 60 µg/m3 after 28 days. Solvent-borne grades stay relevant in cold-weather jobs where rapid set outweighs emissions penalties, though margins narrow on costlier acetates and glycols. Reactive 2K systems address structural floors and bridges requiring greater than 2 MPa adhesion and 25-year durability, but feedstock turbulence adds price volatility.

Hot-melts thrive in prefab lines, delivering 60-second set times that mirror assembly-line takt yet struggle above 80°C facade service. CPR's 2026 DPP trigger rewards water-borne products with lower embodied carbon, lifting their Europe Construction Adhesives and Sealants market size share by 2031. Formulators cross-license humectants and freeze-thaw stabilizers to ensure pan-European shelf life.

List of Companies Covered in this Report:

- 3M

- Arkema

- BASF

- Dow

- fischer Group of Companies

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hexion Inc.

- Huntsman Corporation

- ITW Performance Polymers

- MAPEI S.p.A.

- Momentive

- PPG Industries Inc.

- RPM International Inc.

- Selena Group

- Sika AG

- Soudal Group

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid shift to low-VOC, REACH-compliant formulations

- 4.2.2 Post-pandemic EU renovation wave (Renovation Wave Initiative)

- 4.2.3 Growth of off-site and modular construction

- 4.2.4 Rising demand for high-performance facade systems

- 4.2.5 Carbon-reduction mandates accelerating structural glazing

- 4.2.6 3D-printed concrete's adhesive and sealant demand

- 4.3 Market Restraints

- 4.3.1 Volatility in isocyanate and silicone feedstock prices

- 4.3.2 Russia-Ukraine war driven logistics disruptions

- 4.3.3 Skill shortages in advanced application techniques

- 4.3.4 Lengthy EU chemical approval timelines (CLP/GHS)

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Buyer Power

- 4.7.2 Supplier Power

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Others

- 5.2 By Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Reactive

- 5.2.4 Hot-melt

- 5.2.5 Sealants (1K and 2K)

- 5.3 By Application

- 5.3.1 Flooring and Tiling

- 5.3.2 Roofing

- 5.3.3 Wall Panels and Facades

- 5.3.4 Insulation and Weatherproofing

- 5.3.5 Infrastructure Joints (bridges and tunnels)

- 5.4 By End-use Sector

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.4.4 Infrastructure

- 5.5 By Country

- 5.5.1 France

- 5.5.2 Germany

- 5.5.3 Italy

- 5.5.4 Russia

- 5.5.5 Spain

- 5.5.6 United Kingdom

- 5.5.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/(%)Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 BASF

- 6.4.4 Dow

- 6.4.5 fischer Group of Companies

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Hexion Inc.

- 6.4.9 Huntsman Corporation

- 6.4.10 ITW Performance Polymers

- 6.4.11 MAPEI S.p.A.

- 6.4.12 Momentive

- 6.4.13 PPG Industries Inc.

- 6.4.14 RPM International Inc.

- 6.4.15 Selena Group

- 6.4.16 Sika AG

- 6.4.17 Soudal Group

- 6.4.18 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Key Strategic Questions for Adhesive and Sealant CEOs