PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061749

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061749

China Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

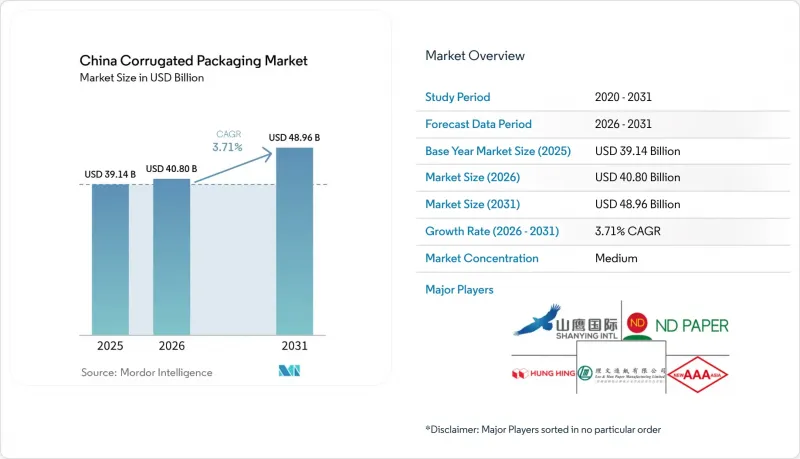

According to Mordor Intelligence, the china corrugated packaging market size is projected to be USD 39.14 billion in 2025, USD 40.80 billion in 2026, and reach USD 48.96 billion by 2031, growing at a CAGR of 3.71% from 2026 to 2031.

This report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, and More), Flute Type (A Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single, Double, and More), Printing Technology (Flexographic, and More), and End-User Industry (Processed Foods, and More). The Market Forecasts are Provided in Terms of Value (USD).

China Corrugated Packaging Market Trends and Insights

Expanding E-Commerce Fulfillment Demand

China processed 175 billion parcels in 2024, and corrugated boxes accounted for roughly 68% of that volume, cementing the channel as the single largest off-taker in the China corrugated packaging market. Fulfillment centers are shifting from regular slotted containers to right-sized, die-cut boxes that reduce void fill, enabling automated lines to complete a pack cycle in under 30 seconds. JD Logistics eliminated more than 1 billion secondary cartons in 2024, forcing converters to compete on lead time, digital customization, and design precision rather than tonnage. Cross-border sellers in the Hainan Free Trade Port and the Greater Bay Area demand micro flute formats that comply with International Air Transport Association dimensional-weight rules, sustaining unit growth even as average board weight declines. Livestream shopping, a channel that generated CNY 4.9 trillion (USD 0.68 trillion) in gross merchandise value during 2025, has turned packaging into on-screen advertising, prompting brands to pay 40%-60% premiums for litho-laminated, camera-ready shippers.

Rising Environmental Regulations Favoring Recyclable Packaging

The Ministry of Ecology and Environment raised the recycled-content threshold for new corrugated boxes to 85% by 2027, up from a 70% baseline, anchoring recycled linerboard's 63.21% share in 2025. Import quotas that cut recovered-paper inflows to 4.2 million tonnes in 2025 tightened domestic scrap markets, lifting prices 12% year on year. Provincial extended-producer-responsibility pilots shift collection costs to brand owners, accelerating lightweighting and alternative-fiber trials in Zhejiang and Jiangsu. In pharmaceuticals, the new T/CNPPA 3029-2025 standard specifies low moisture-vapor transmission, carving a regulatory moat for virgin kraft grades in cold-chain cartons. Large mills capitalize on scale to absorb wastewater and VOC-control capex, while regional converters face margin erosion of 8%-12% under the 14th Five-Year Plan.

Volatility in Recovered Paper Import Policies

Imports slid to 4.2 million tonnes in 2025 under a 0.3% contamination cap, exposing mills to spot-market spikes and lengthening customs clearance from 7 to 18 days. Domestic OCC prices rose 12%, squeezing converters without captive pulping and prompting some buyers to shift to flexible pouches despite recyclability trade-offs. Coastal mills that historically favored long-fiber American scrap are reallocating capital to virgin pulp, illustrated by Nine Dragons' USD 4.8 billion Beihai complex with 1.1 million tonnes of chemical pulp. Municipal collection remains fragmented, with 35% of urban corrugated waste still co-mingled, adding de-inking costs and weakening small-mill competitiveness.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Fresh Produce and Food Delivery Services

- Urbanization Driving Consumer Goods Consumption

- Competition from Flexible Plastic Packaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled linerboard accounted for 63.21% of the China corrugated packaging market in 2025, reflecting the mandated 85% recycled content requirement for express parcels by 2027. Integrated mills capture feedstock advantages through nationwide OCC collection networks, anchoring their cost leadership. Virgin Kraft linerboard is forecast to expand at 4.77% CAGR, outperforming overall growth as fresh-produce exporters and luxury e-commerce brands demand higher ring-crush strength, tear resistance, and cleaner print surfaces. Nine Dragons' Beihai mill and Lee and Man's specialty-kraft upgrades target this premium. Corrugating medium producers are testing semi-chemical pulps from bamboo and straw to hedge softwood risks, though moisture sensitivity still confines such grades to low-humidity logistics corridors.

Bio-based barrier coatings and starch adhesives are scaling up in pilot runs to achieve recyclability without wax, signaling that the China corrugated packaging market will bifurcate into high-volume recycled-content and smaller, high-margin virgin niches. In parallel, food-contact and pharmaceutical mandates under T/CNPPA 3029-2025 steer critical temperature-controlled applications toward virgin fiber, guaranteeing a price umbrella that offsets higher raw-material costs. The converter strategy, therefore, splits commodity players chase recycled linerboard efficiency, while value-added specialists court brand owners with premium kraft and functional coatings.

B flute held 34.15% of the China corrugated packaging market share in 2025 because of its cushioning-to-cost balance in general merchandise. However, the F flute is accelerating at 4.15% CAGR through 2031 as cross-border sellers optimize for dimensional weight and cosmetics brands seek offset-level graphics. The flute's 0.75-1.0 mm caliper allows direct lithographic printing, eliminating litho-lamination steps and lowering inventory bulk, which is vital in automated warehouses with height constraints.

E flute remains the compromise format for retail-ready displays, offering rigidity with acceptable board economy. A flute persists for fragile ceramics and heavy industrial parts owing to its 5 mm thickness, though its share erodes under lightweighting mandates. Corrugator OEMs now ship quick-change cassette systems that let factories swap flute profiles in under 15 minutes, democratizing micro flute access for small and medium enterprises and enhancing adoption momentum.

List of Companies Covered in this Report:

- Shanying International Holdings Co. Ltd.

- Nine Dragons Paper (Holdings) Limited

- Lee & Man Paper Manufacturing Ltd.

- Hung Hing Printing Group Limited

- New Asia Packaging Co. Ltd.

- HengFeng Packaging Materials Co. Ltd.

- Shanghai DE Printed Box

- Belpax

- Baoding Yueyang Packaging

- ZZ Group International Holdings Limited

- Jingxing Paper

- Minfeng Special Paper Co. Ltd.

- Yutian Hs Packaging Co. Ltd.

- Dongguan Jianxin

- Rizhao Forest Packaging

- Sinopack Industries Ltd.

- International Paper (China) Co. Ltd.

- Smurfit Westrock plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Overview of the Global Corrugated Packaging Market

- 4.6 Investment Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Expanding E-Commerce Fulfillment Demand

- 5.1.2 Rising Environmental Regulations Favoring Recyclable Packaging

- 5.1.3 Growth in Fresh Produce and Food Delivery Services

- 5.1.4 Urbanization Driving Consumer Goods Consumption

- 5.1.5 Provincial Incentives for Lightweight Packaging Innovation

- 5.1.6 Adoption of Digital Print-On-Demand Corrugated Boxes by SMEs

- 5.2 Market Restraints

- 5.2.1 Volatility in Recovered Paper Import Policies

- 5.2.2 Competition from Flexible Plastic Packaging

- 5.2.3 Bottlenecks in Last-Mile Logistics Pallet Standardization

- 5.2.4 Emerging Bioplastic Corrugated Alternatives from Startups

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Material

- 6.1.1 Virgin Kraft Linerboard

- 6.1.2 Recycled Linerboard

- 6.1.3 Corrugating Medium

- 6.1.4 Semi-Chemical Fluting

- 6.1.5 Other Materials

- 6.2 By Flute Type

- 6.2.1 A Flute

- 6.2.2 B Flute

- 6.2.3 C Flute

- 6.2.4 E Flute

- 6.2.5 F Flute

- 6.3 By Packaging Type

- 6.3.1 Regular Slotted Containers

- 6.3.2 Die-Cut Custom Boxes

- 6.3.3 Folding Cartons

- 6.3.4 Point-of-Purchase Displays

- 6.3.5 Pallet Boxes

- 6.3.6 Other Packaging Types

- 6.4 By Wall Type

- 6.4.1 Single-Wall

- 6.4.2 Double-Wall

- 6.4.3 Triple-Wall

- 6.4.4 Single Face

- 6.5 By Printing Technology

- 6.5.1 Flexographic Printing

- 6.5.2 Digital Inkjet Printing

- 6.5.3 Litho-Lamination

- 6.5.4 Screen Printing

- 6.5.5 Other Printing Technologies

- 6.6 By End-User Industry

- 6.6.1 Processed Foods

- 6.6.2 Fresh Food and Produce

- 6.6.3 Beverages

- 6.6.4 Paper Products

- 6.6.5 Electrical Products

- 6.6.6 Personal Care and Cosmetics

- 6.6.7 E-commerce Fulfillment Centers

- 6.6.8 Pharmaceuticals

- 6.6.9 Other End-User Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles

- 7.4.1 Shanying International Holdings Co. Ltd.

- 7.4.2 Nine Dragons Paper (Holdings) Limited

- 7.4.3 Lee & Man Paper Manufacturing Ltd.

- 7.4.4 Hung Hing Printing Group Limited

- 7.4.5 New Asia Packaging Co. Ltd.

- 7.4.6 HengFeng Packaging Materials Co. Ltd.

- 7.4.7 Shanghai DE Printed Box

- 7.4.8 Belpax

- 7.4.9 Baoding Yueyang Packaging

- 7.4.10 ZZ Group International Holdings Limited

- 7.4.11 Jingxing Paper

- 7.4.12 Minfeng Special Paper Co. Ltd.

- 7.4.13 Yutian Hs Packaging Co. Ltd.

- 7.4.14 Dongguan Jianxin

- 7.4.15 Rizhao Forest Packaging

- 7.4.16 Sinopack Industries Ltd.

- 7.4.17 International Paper (China) Co. Ltd.

- 7.4.18 Smurfit Westrock plc

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-Space and Unmet-Need Assessment