PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063491

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063491

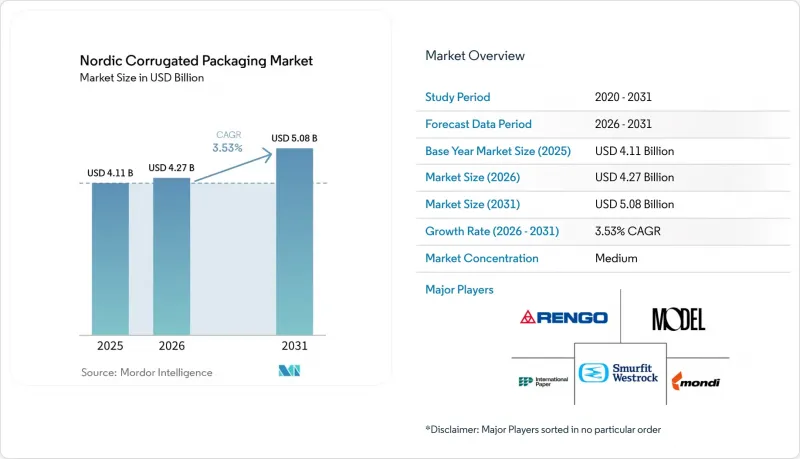

Nordic Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the nordic corrugated packaging market size is projected to expand from USD 4.11 billion in 2025 and USD 4.27 billion in 2026 to USD 5.08 billion by 2031, registering a CAGR of 3.53% between 2026 to 2031.

This report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, and More), Flute Type (A Flute, B Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single-Wall, and More), Printing Technology (Flexographic Printing, and More), End-User Industry (Processed Foods, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Nordic Corrugated Packaging Market Trends and Insights

Rising E-Commerce Logistics Acceleration

Online grocery and non-food penetration keeps growing, shifting demand from pallet-load master cartons toward smaller automation-ready boxes that drop straight into last-mile networks. Smurfit WestRock engineered a collapsible box with reinforced corners and single-hand lids for Denmark-based Nemlig, enabling flat inbound delivery and automated erection within existing crate lines. Sweden's household collection rates feed high-quality recycled liner back to Nordic corrugated packaging market converters, closing the fiber loop and lowering carbon intensity. Ranpak's Cut'it EVO line rationalized eight box types down to one at Swedish fulfillment hubs, trimming void fill and freight volume. The EU Packaging and Packaging Waste Regulation, coming into force in 2026, imposes recyclability thresholds that reinforce the switch to fiber-based shippers.

Regulatory Shift Toward Recyclable Packaging

EU rules ban selected single-use plastics by 2030 and embed recycled-content quotas, prompting retailers and brand owners to pivot toward fiber solutions that secure eco-modulation fee discounts. Stora Enso's EUR 1.1 billion (USD 1.24 billion) consumer board line in Oulu, Finland, produces kraftliners up to 33% lighter, slashing transport emissions while meeting direct food-contact rules. Nordic Swan Ecolabel criteria push converters to water-based inks that align with the Swiss Ordinance and Nestle safety lists. These combined levers keep the Nordic corrugated packaging market firmly on a sustainability trajectory.

Recycled Paper Price Volatility

Old corrugated container prices spiked in April 2025, squeezing converters on fixed-price supply contracts. Progroup's waste-to-energy assets mute the hit, but Nordic independents without mill ownership saw EBITDA erosion and deferred digital-press upgrades. Smurfit WestRock plc wrote off USD 73 million in accelerated depreciation linked to EMEA mill closures to rebalance capacity. Converters are now negotiating fiber cost pass-through clauses and exploring vertical-integration partnerships that tie box output more tightly to liner supply.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Processed Food and Beverage Exports

- Expansion of Nordic Seafood Exports Requiring Wet-Strength Grades

- Competition From Returnable Plastic Crates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled linerboard held 44.85% of the Nordic corrugated packaging market share in 2025 as municipal collection systems in Sweden and Denmark fed high-quality post-consumer fiber back into local mills. Virgin Kraftliner services premium pharmaceutical and electronics loads that cannot risk contaminants, but its role is comparatively smaller and price-sensitive. Semi-chemical fluting is projected to post a 4.82% CAGR through 2031 as seafood exporters order wet-strength grades that retain crush resistance after ice contact.

Nordic corrugated packaging market size gains in this segment will also benefit from lighter-weight kraftliners made at Stora Enso's Oulu line, which cut basis weight by one-third without sacrificing stiffness. Prices for imported virgin pulp remain vulnerable to currency swings, but American Industrial Partners' 2026 takeover of International Paper's Polish mills secures a regional softwood supply base. Klingele's mills in Germany, France, and Brazil funnel virgin and recycled liners into its three Nordic plants, shielding customers from spot-market volatility.

B flute retained 38.41% share in 2025 by balancing cushioning with paper efficiency, fitting everyday e-commerce shippers and processed-food trays that enter automated erection lines. E flute, however, is forecast to grow at a 4.47% CAGR, as drug manufacturers favor its slim 1.5-millimeter profile, which accommodates more vials per pallet layer while still printing pharmacy barcodes crisply. Canon's corrPress iB17 outputs 1200-dpi water-based graphics on E flute at 8,000 m2 per hour, enabling Nordic converters to combine serialization and branding in a single inline pass.

A flute and double-wall hybrids still serve bulky electronics and glassware bound for regional fulfillment hubs, leveraging greater cushioning at modest material cost increases. Pharmaceutical 2-D matrix codes and temperature-sensitive inks require substrates with tight caliper control, a specification E flute effortlessly meets, further reinforcing its adoption curve. Packaging engineers now benchmark flute choice not only on edge-crush tests but also on optical scanning fidelity for traceability systems. Nordic converters thereby position E flute as the workhorse for high-value, data-rich shipments, narrowing B flute's long-time dominance.

List of Companies Covered in this Report:

- Smurfit WestRock plc

- International Paper Company

- Mondi plc

- Stora Enso Oyj

- VPK Packaging Group NV

- Klingele Paper and Packaging Group

- Progroup AG

- Rengo Co. Ltd.

- Model Holding AG

- Schumacher Packaging GmbH

- Trioworld Group

- Peterson Packaging AS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising E-commerce Logistics Acceleration

- 4.2.2 Growth in Processed Food and Beverage Exports

- 4.2.3 Regulatory Shift Toward Recyclable Packaging

- 4.2.4 Nearshoring-Led Electronics Output

- 4.2.5 Craft-Brewery Demand for Custom Boxes

- 4.2.6 Expansion of Nordic Sea-Food Exports Requiring Wet-Strength Grades

- 4.3 Market Restraints

- 4.3.1 Recycled Paper Price Volatility

- 4.3.2 Competition from Returnable Plastic Crates

- 4.3.3 Water-Scarcity Constraints on Nordic Mills

- 4.3.4 Dependence on Imported Virgin Fiber

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Virgin Kraft Linerboard

- 5.1.2 Recycled Linerboard

- 5.1.3 Corrugating Medium

- 5.1.4 Semi-Chemical Fluting

- 5.1.5 Other Materials

- 5.2 By Flute Type

- 5.2.1 A Flute

- 5.2.2 B Flute

- 5.2.3 C Flute

- 5.2.4 E Flute

- 5.2.5 F Flute

- 5.3 By Packaging Type

- 5.3.1 Regular Slotted Containers

- 5.3.2 Die-Cut Custom Boxes

- 5.3.3 Folding Cartons

- 5.3.4 Point-of-Purchase Displays

- 5.3.5 Pallet Boxes

- 5.3.6 Other Packaging Types

- 5.4 By Wall Type

- 5.4.1 Single-Wall

- 5.4.2 Double-Wall

- 5.4.3 Triple-Wall

- 5.4.4 Single Face

- 5.5 By Printing Technology

- 5.5.1 Flexographic Printing

- 5.5.2 Digital Inkjet Printing

- 5.5.3 Litho-Lamination

- 5.5.4 Screen Printing

- 5.5.5 Other Printing Technologies

- 5.6 By End-User Industry

- 5.6.1 Processed Foods

- 5.6.2 Fresh Food and Produce

- 5.6.3 Beverages

- 5.6.4 Electrical Products

- 5.6.5 Personal Care and Cosmetics

- 5.6.6 E-commerce Fulfillment Centers

- 5.6.7 Pharmaceuticals

- 5.6.8 Other End-User Industries

- 5.7 By Country

- 5.7.1 Sweden

- 5.7.2 Denmark

- 5.7.3 Norway

- 5.7.4 Finland

- 5.7.5 Iceland

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit WestRock plc

- 6.4.2 International Paper Company

- 6.4.3 Mondi plc

- 6.4.4 Stora Enso Oyj

- 6.4.5 VPK Packaging Group NV

- 6.4.6 Klingele Paper and Packaging Group

- 6.4.7 Progroup AG

- 6.4.8 Rengo Co. Ltd.

- 6.4.9 Model Holding AG

- 6.4.10 Schumacher Packaging GmbH

- 6.4.11 Trioworld Group

- 6.4.12 Peterson Packaging AS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment