PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063650

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063650

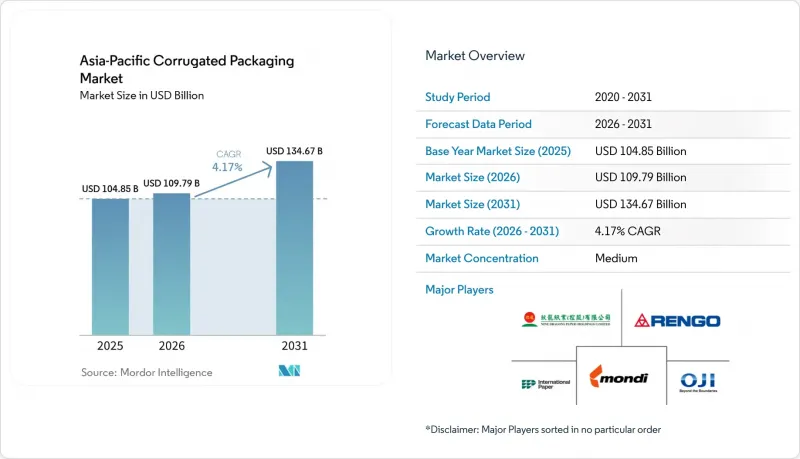

Asia-Pacific Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific corrugated packaging market size is expected to grow from USD 104.85 billion in 2025 to USD 109.79 billion in 2026 and is forecast to reach USD 134.67 billion by 2031 at 4.17% CAGR over 2026-2031.

This report is Segmented by Material (Virgin Kraft Linerboard, and More), Flute Type (A Flute, B Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single-Wall, Double-Wall, and More), Printing Technology (Flexographic Printing, and More), End-User Industry (Processed Foods, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Corrugated Packaging Market Trends and Insights

Growing Food and Beverage Consumption in Emerging Asian Economies

Rising urban incomes across China, India, and core ASEAN nations are boosting per capita purchases of packaged produce, processed foods, and beverages. Corrugated demand benefits directly because perishable exports require ventilated, moisture-resistant shippers that protect against temperature swings during multimodal transport. China's express-delivery network handled over 175 billion parcels in 2024, a surge that is translating into secondary demand for fruit and meal-kit shippers as e-grocers widen same-day coverage. Stringent food-contact rules, such as Indonesia's SNI 8218:2024 and Thailand's TIS standards, have raised compliance costs, prompting converters to migrate premium SKUs to virgin kraft. India's 2025 anti-subsidy probe on imported paperboards is already shifting supply chains toward domestic mills, tightening recovered-fiber markets, and incentivizing investment in high-basis-weight machines.

Shift Toward Sustainable and Recyclable Packaging Materials

Extended producer responsibility schemes in Japan and South Korea require brand owners to document recycled content and end-of-life pathways, a structure that is quickly influencing purchasing teams across the wider region. Recycled linerboard already held 54.12% share in 2025, yet food and pharma brands are paying premiums for virgin grades with certified chain-of-custody to meet global audit requirements. The University of Maine demonstrated that Trametes versicolor fungus-derived coatings can replace polyethylene liners while maintaining moisture resistance and improving repulpability. Multinationals such as Mondi are responding with EUR 1.2 billion (USD 1.3 billion) in mill upgrades that raise recovered-fiber utilization without sacrificing mechanical strength, positioning their kraft portfolio for a future in which carbon and recyclability scores sit alongside unit cost in sourcing decisions.

Volatility in Paperboard Raw Material Prices

Capacity closures totaling 2.5 million tons in North America and logistics snarls in the Panama Canal have whipsawed kraft linerboard spot prices, compressing converter margins. Integrated giants such as Nine Dragons and Lee and Man posted triple-digit profit jumps in 2025 because captive fiber insulated them from spikes, while small converters operating on spot contracts saw working-capital cycles stretch dangerously. India's anti-subsidy probe on Chinese and Indonesian boards is reshaping Asia-Pacific trade flows, yet new domestic mills will not come online until 2027, meaning price turbulence will persist in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of E-Commerce and Omni-Channel Retail

- Increasing Pharmaceutical Production and Healthcare Spending

- Competition from Flexible Packaging Formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled linerboard secured 54.12% of the Asia-Pacific corrugated packaging market share in 2025 as cost-sensitive e-commerce and industrial users optimize transportation budgets. Virgin Kraft is expanding at 5.62% CAGR, capturing high-margin niches where direct food contact and pharmaceutical purity standards dictate certified fiber chains. This divergence is sharpening supplier specialization; Indonesian mills are adding virgin capacity, while Chinese converters deepen recovered-fiber loops to insulate against import curbs.

Converters reliant on recycled grades must now invest in optical sorters and moisture-control systems to meet China's GB/T 6543-2025 squareness and compression mandates, which come into force in December 2025. Meanwhile, premium exporters of seafood and fresh produce are locking in multi-year virgin kraft contracts to secure moisture tolerance during trans-Pacific voyages, widening the price delta between commodity and specialty grades.

C flute retained 53.78% share in 2025, balancing cushioning and compression strength for general shipping needs, but E flute is advancing at 5.23% CAGR as retailers pursue thinner profiles that slash cube utilization and freight emissions. DS Smith's 2026 investment in a Gopfert rotary die-cutter illustrates the race to deliver micro-flute accuracy at an industrial scale, as cosmetics, electronics, and personal-care brands demand litho-like print fidelity on corrugated substrates. F-flute, though smaller in volume, is gaining traction in luxury gift packs and subscription boxes, where tactile unboxing experiences must coexist with drop-test robustness.

The pivot toward micro-flutes obliges mills to supply smoother, high-stiffness linerboard that tolerates tighter caliper tolerances, again favoring integrated producers that can blend virgin and recovered fibers on the same machine. Converters must weigh the higher capital outlay for fine-flute corrugators against the logistical savings clients achieve via lighter, flatter boxes that fill truck decks more efficiently. As e-commerce algorithms optimize dimensional weight billing, brand owners will push box makers toward ever-thinner profiles, cementing E flute and F flute as the fastest-growing niches within the Asia-Pacific corrugated packaging market over the next five years.

List of Companies Covered in this Report:

- Nine Dragons Paper (Holdings) Limited

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Lee & Man Paper Manufacturing Ltd.

- International Paper Company

- Mondi plc

- Nippon Paper Industries Co., Ltd.

- Orora Limited

- Visy Industries Holdings Pty Ltd.

- Thai Containers Group Co., Ltd.

- Zhejiang Jingxing Paper Joint Stock Co., Ltd.

- YFY Inc.

- Smurfit WestRock plc

- Shenzhen Rongda Printing and Packaging Co., Ltd.

- Shenzhen BHL Paper Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Food and Beverage Consumption in Emerging Asian Economies

- 4.2.2 Shift Toward Sustainable and Recyclable Packaging Materials

- 4.2.3 Rapid Expansion of E-Commerce and Omni-Channel Retail

- 4.2.4 Increasing Pharmaceutical Production and Healthcare Spending

- 4.2.5 Government-Led Subsidies for High-Color Digital Carton Printing in Export Hubs

- 4.2.6 Adoption of Fungus-Based Barrier Coatings Replacing Plastic Liners

- 4.3 Market Restraints

- 4.3.1 Volatility in Paperboard Raw Material Prices

- 4.3.2 Competition from Flexible Packaging Formats

- 4.3.3 Tightening Regional Water-Use Regulations Increasing Mill Operating Costs

- 4.3.4 Shortage of Skilled Technicians for High-Speed Folding-Gluing Lines

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Kraft Linerboard

- 5.1.2 Recycled Linerboard

- 5.1.3 Corrugating Medium

- 5.1.4 Semi-Chemical Fluting

- 5.1.5 Other Materials

- 5.2 By Flute Type

- 5.2.1 A Flute

- 5.2.2 B Flute

- 5.2.3 C Flute

- 5.2.4 E Flute

- 5.2.5 F Flute

- 5.3 By Packaging Type

- 5.3.1 Regular Slotted Containers

- 5.3.2 Die-Cut Custom Boxes

- 5.3.3 Folding Cartons

- 5.3.4 Point-of-Purchase Displays

- 5.3.5 Pallet Boxes

- 5.3.6 Other Packaging Types

- 5.4 By Wall Type

- 5.4.1 Single-Wall

- 5.4.2 Double-Wall

- 5.4.3 Triple-Wall

- 5.4.4 Single Face

- 5.5 By Printing Technology

- 5.5.1 Flexographic Printing

- 5.5.2 Digital Inkjet Printing

- 5.5.3 Litho-Lamination

- 5.5.4 Screen Printing

- 5.5.5 Other Printing Technologies

- 5.6 By End-User Industry

- 5.6.1 Processed Foods

- 5.6.2 Fresh Food and Produce

- 5.6.3 Beverages

- 5.6.4 Electrical Products

- 5.6.5 Personal Care and Cosmetics

- 5.6.6 E-commerce Fulfillment Centers

- 5.6.7 Pharmaceuticals

- 5.6.8 Other End-User Industries

- 5.7 By Geography

- 5.7.1 China

- 5.7.2 India

- 5.7.3 Japan

- 5.7.4 South Korea

- 5.7.5 Australia and New Zealand

- 5.7.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Nine Dragons Paper (Holdings) Limited

- 6.4.2 Oji Holdings Corporation

- 6.4.3 Rengo Co., Ltd.

- 6.4.4 Lee & Man Paper Manufacturing Ltd.

- 6.4.5 International Paper Company

- 6.4.6 Mondi plc

- 6.4.7 Nippon Paper Industries Co., Ltd.

- 6.4.8 Orora Limited

- 6.4.9 Visy Industries Holdings Pty Ltd.

- 6.4.10 Thai Containers Group Co., Ltd.

- 6.4.11 Zhejiang Jingxing Paper Joint Stock Co., Ltd.

- 6.4.12 YFY Inc.

- 6.4.13 Smurfit WestRock plc

- 6.4.14 Shenzhen Rongda Printing and Packaging Co., Ltd.

- 6.4.15 Shenzhen BHL Paper Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment