PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063759

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063759

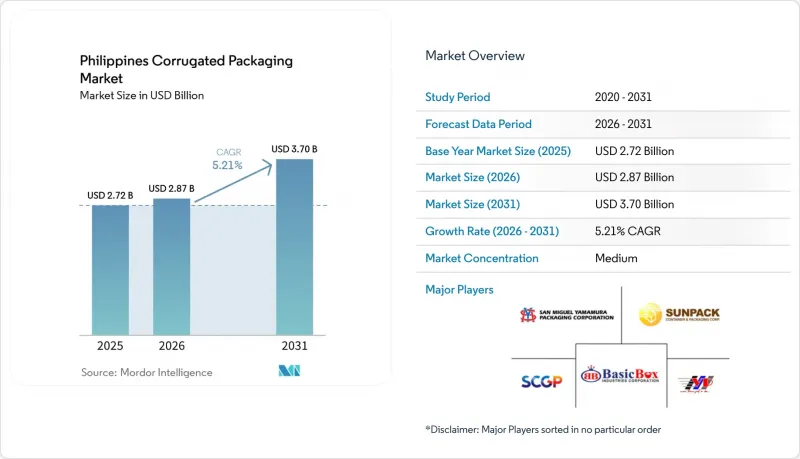

Philippines Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the philippines corrugated packaging market size is projected to expand from USD 2.72 billion in 2025 and USD 2.87 billion in 2026 to USD 3.7 billion by 2031, registering a CAGR of 5.21% between 2026 to 2031.

This report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, and More), Flute Type (A Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single-Wall, Double-Wall, and More), Printing Technology (Flexographic Printing, and More), End-User Industry (Processed Foods, and More). The Market Forecasts are Provided in Terms of Value (USD).

Philippines Corrugated Packaging Market Trends and Insights

E-Commerce Growth Accelerating Parcel Volumes

Same-day and next-day delivery commitments have transformed the distribution landscape, swapping palletized store replenishment for millions of single-item drop-offs. Flash-sale peaks on 11-11 and 12-12 force corrugators to stock seasonal blanks and adjust flute combinations that limit freight weight while preserving edge-crush strength. Multi-modal legs across road, sea, and air magnify humidity exposure, steering merchants toward lighter recycled-fiber liners that still pass stacking tests. Fulfillment centers are standardizing box footprints so automated sorters can scan, label, and manifest parcels with minimal human touch. These shifts collectively raise volumes for the Philippines' corrugated packaging market, especially in Metro Manila's parcel hubs.

Government Restrictions on Single-Use Plastics Favoring Paper-Based Alternatives

The Extended Producer Responsibility Act requires brand owners to recover 40% of their plastic packaging footprint in 2024, climbing to 80% by 2028, with fines up to USD 5 million for non-compliance. Simultaneously, the Department of Finance is pressing for a USD 100-per-kilogram excise tax on disposable plastic bags, potentially pushing retail bag prices up 94%. Local ordinances from Quezon City's civic complex ban on plastic disposables to nationwide sachet phase-outs compound the pressure. Brand owners now specify corrugated secondary packs and fiber-based takeout containers that score favorably on recyclability audits. These mandates are nudging procurement managers to lock in extra corrugated volumes, fortifying the growth arc of the Philippines corrugated packaging market.

Volatility in Domestic and Imported Recovered Paper Prices

Import OCC quotes swung from USD 160 per tonne for European 95/5 to USD 230 per tonne for U.S. DS-OCC in 2024 as U.S. and EU collection rates dipped and Indonesian inspection fees rose. Local converters suffer double exposure: higher landed costs on imported grades and erratic street-price jumps when informal-sector collectors thin out supply. Only 44% of barangays operate functional materials-recovery facilities, with Metro Manila's coverage at 20%, leaving mills vulnerable to cargo arrival lags and fiber quality downgrades. These shocks crimp gross margins and temper near-term investment appetite in the Philippines corrugated packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Shift Toward Sustainable and Recycled Fiber Packaging

- Expansion of Processed Food and Beverage Manufacturing Hubs

- Port Congestion and Shipping Delays Inflating Lead Times and Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled linerboard captured 56.12% of the Philippines corrugated packaging market in 2025, reflecting structural dependence on domestic OCC streams. The Philippines' corrugated packaging market for recycled fiber continues to grow as mills blend locally baled cartons with imported Class A OCC to offset the scarcity of virgin pulp. Semi-chemical fluting, forecast to grow at a 7.13% CAGR, is gaining favor among inter-island shippers seeking lighter grammages with similar stacking strength, a shift amplified by rising fuel surcharges. Virgin Kraft linerboard remains a niche for moisture-critical produce and pharmaceutical exports, where print gloss and wet-strength ratings justify the premium.

The corrugating medium benefits from United Pulp and Paper's new 870-TPD OCC line, which filters contaminants using PrimeRotor screens to stabilize runnability. Demand for performance coatings is inching up as the Department of Agriculture spends PHP 3 billion (USD 52.8 million) on 99 hybrid-energy cold storages. Triple-wall blanks with wax or bio-coated liners prevent condensation damage on long reefers, creating a profitable specialty pocket within the broader Philippines corrugated packaging market share landscape. Imported OCC volatility continues to push mills toward captive collection centers that lock in fiber at predictable costs, strengthening margins even as power tariffs rise.

B flute secured 41.37% market share in 2025 thanks to its balance of crush resistance, print surface, and compatibility with automatic case packers. Converters run continuous-knife setups that switch from B to C to E flute without major downtime, allowing rapid response to seasonal beverage trays or electronics shrink-wrap replacements. F flute, one-third the caliper of B, is projected for 6.89% CAGR as cosmetics and smart-watch sellers opt for slimmer parcels that fit courier pouches and reduce dimensional weight surcharges.

The Philippines corrugated packaging market size for F flute remains modest today yet offers higher unit margins because of multi-pass digital graphics. C flute maintains a foothold in heavy canned-goods packs, but brand owners eye upstream savings from thinner profiles. E flute doubles as a rigid alternative to folding cartons for pizza and apparel mailers, while A flute's usage is confined to bulk agro-exports requiring superior cushioning. Thin-profile adoption aligns with port modernization that reduces voyage time, easing moisture-ingress risks and enabling merchants to shift toward lighter makeup.

List of Companies Covered in this Report:

- SCG Packaging Public Company Limited

- San Miguel Yamamura Packaging Corp.

- Liberty Corrugated Boxes Mfg. Corp.

- Valenzuela Packaging Container Corp.

- Quality Corrugated Box Manufacturing Corp.

- Sunpack Container and Packaging Corp.

- Prime Worldwide Paper Packaging Corp.

- Steniel Graham Packaging Philippines Corp.

- Malinta Corrugated Boxes Manufacturing Corp.

- Basic Box Industries Corp.

- Papercon Philippines Inc.

- Central Corrugated Box Corp.

- Duraboard Packaging Corp.

- Three Dimensional Packaging Corp.

- Boxworld Co Inc.

- Basic Box Industries Corp.

- RM Box Center

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Growth Accelerating Parcel Volumes

- 4.2.2 Rapid Shift Toward Sustainable and Recycled Fiber Packaging

- 4.2.3 Expansion of Processed Food and Beverage Manufacturing Hubs

- 4.2.4 Government Restrictions on Single-Use Plastics Favoring Paper-Based Alternatives

- 4.2.5 Modernization of Inter-Island Logistics Networks Demanding Durable Lightweight Boxes

- 4.2.6 Adoption of Digital Printing Enabling Short-Run Customization for SMEs

- 4.3 Market Restraints

- 4.3.1 Volatility in Domestic and Imported Recovered Paper Prices

- 4.3.2 Substitution Threat From Flexible Plastics and Reusable Plastic Crates

- 4.3.3 Port Congestion and Shipping Delays Inflating Lead Times and Costs

- 4.3.4 Escalating Electricity Tariffs Increasing Corrugator Operating Expenses

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Virgin Kraft Linerboard

- 5.1.2 Recycled Linerboard

- 5.1.3 Corrugating Medium

- 5.1.4 Semi-Chemical Fluting

- 5.1.5 Other Materials

- 5.2 By Flute Type

- 5.2.1 A Flute

- 5.2.2 B Flute

- 5.2.3 C Flute

- 5.2.4 E Flute

- 5.2.5 F Flute

- 5.3 By Packaging Type

- 5.3.1 Regular Slotted Containers

- 5.3.2 Die-Cut Custom Boxes

- 5.3.3 Folding Cartons

- 5.3.4 Point-of-Purchase Displays

- 5.3.5 Pallet Boxes

- 5.3.6 Other Packaging Types

- 5.4 By Wall Type

- 5.4.1 Single-Wall

- 5.4.2 Double-Wall

- 5.4.3 Triple-Wall

- 5.4.4 Single Face

- 5.5 By Printing Technology

- 5.5.1 Flexographic Printing

- 5.5.2 Digital Inkjet Printing

- 5.5.3 Litho-Lamination

- 5.5.4 Screen Printing

- 5.5.5 Other Printing Technologies

- 5.6 By End-User Industry

- 5.6.1 Processed Foods

- 5.6.2 Fresh Food and Produce

- 5.6.3 Beverages

- 5.6.4 Electrical Products

- 5.6.5 Personal Care and Cosmetics

- 5.6.6 E-commerce Fulfillment Centers

- 5.6.7 Pharmaceuticals

- 5.6.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SCG Packaging Public Company Limited

- 6.4.2 San Miguel Yamamura Packaging Corp.

- 6.4.3 Liberty Corrugated Boxes Mfg. Corp.

- 6.4.4 Valenzuela Packaging Container Corp.

- 6.4.5 Quality Corrugated Box Manufacturing Corp.

- 6.4.6 Sunpack Container and Packaging Corp.

- 6.4.7 Prime Worldwide Paper Packaging Corp.

- 6.4.8 Steniel Graham Packaging Philippines Corp.

- 6.4.9 Malinta Corrugated Boxes Manufacturing Corp.

- 6.4.10 Basic Box Industries Corp.

- 6.4.11 Papercon Philippines Inc.

- 6.4.12 Central Corrugated Box Corp.

- 6.4.13 Duraboard Packaging Corp.

- 6.4.14 Three Dimensional Packaging Corp.

- 6.4.15 Boxworld Co Inc.

- 6.4.16 Basic Box Industries Corp.

- 6.4.17 RM Box Center

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment