PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062023

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062023

Asia-Pacific Food Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

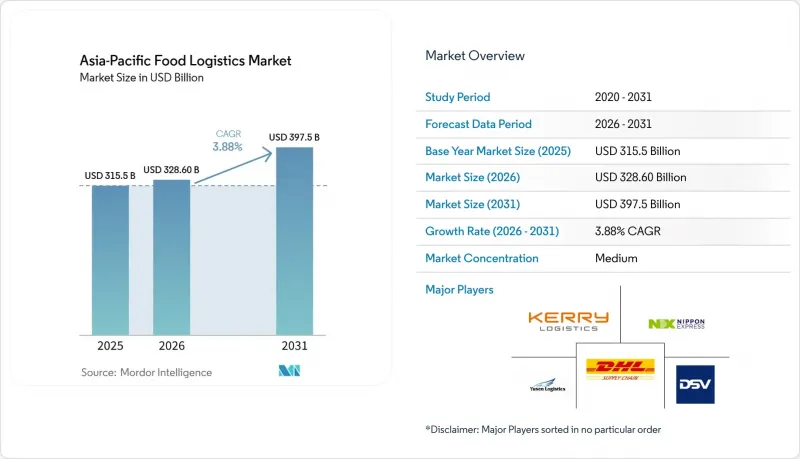

According to Mordor Intelligence, the asia-Pacific food logistics market size is expected to increase from USD 315.5 billion in 2025 to USD 328.60 billion in 2026 and reach USD 397.5 billion by 2031, growing at a CAGR of 3.88% over 2026-2031.

This report is Segmented by Services (Transportation, Warehousing, and Value-Added Services), by Temperature-Control Type (Cold Chain, Non Cold Chain), by End-Product Category (Meat & Seafood, Dairy, Fruits & Vegetables, Food and Beverages, and Others), and by Geography (China, Japan, India, South Korea, Australia, Southeast Asia, and Rest of Asia-Pacific). Market Forecasts are Provided in Value (USD).

Asia-Pacific Food Logistics Market Trends and Insights

Foreign Investment and Logistics Modernization

Vietnam's national roadmap elevates logistics to a foundational economic sector and prioritizes cold storage for agricultural outputs, with a long-term focus on green logistics that uses clean energy to support the agri-food value chain. Singapore's Food Services Industry Digital Plan provides adoption tracks for AI-enabled document reconciliation and logistics control towers that help SMEs manage temperature-controlled flows with higher visibility and security, while aligning skills and cybersecurity needs for the sector. China's cross-ministry plan targets 80% digitalization for business management and 75% digital control over key processes in large food enterprises by 2027, backed by demonstration projects and typical application scenarios that cascade into logistics operations. These national programs set a consistent direction for investment in temperature telemetry, secure data exchanges, and warehouse automation across the Asia-Pacific food logistics market. The push to modernize also narrows capability gaps between advanced hubs and emerging corridors where smaller operators face financing constraints. As uptake increases, service expectations now include auditable cold chain records and integrated exception handling that reinforce buyer confidence in temperature-sensitive movements across borders.

E-commerce and Quick Commerce Boom

Rapid adoption of online grocery and meal platforms is compressing delivery windows and placing a premium on short-radius cold distribution. In Singapore, e-commerce is projected to double between 2023 and 2030, and the cold chain perishables market is expected to double by 2034, reinforcing the need for robust chilled and frozen capacity in importer hubs with significant re-export activity. Digital control towers and automated ordering are improving coordination between procurement, production, and distribution to support reliability at narrow delivery intervals across the Asia-Pacific food logistics market. Cross-border e-commerce growth also benefits from rising air cargo capacity and expanded cool-chain capability at regional gateways through 2028, helping time-sensitive food products reach consumers with higher service levels. Quick commerce models are changing network design as operators pre-position chilled and frozen inventory in micro-fulfillment centers to meet three-kilometer delivery radii in dense urban areas. These shifts reward integrated providers that can orchestrate temperature, visibility, and last-mile handoffs in one service layer across the Asia-Pacific food logistics market.

Fragmented Cold Chain Infrastructure

India's cold chain supports only a small portion of the fresh produce needs, and roughly three-quarters of the bulk storage capacity is concentrated in single-commodity potato facilities that cannot flex for diversified horticulture. Sparse assets at the farmgate, such as pre-cooling units and packhouses, increase thermal stress before produce enters formal networks and raise the risk of losses during peak seasons. Many older facilities rely on inefficient systems and poor insulation, which heighten energy intensity in power-constrained regions and limit the ability to maintain precise temperature controls. In Thailand, agricultural freight remains dominated by road, while rail and inland water transport options are underused, which keeps logistics costs elevated relative to international benchmarks and increases exposure to temperature excursions on longer routes. The lack of integrated networks and uneven capacity distribution forces exporters to stitch together multiple providers across the first mile, line-haul, storage, and border processes. These handoffs increase both dwell time and temperature risk, which limits quality outcomes in the Asia-Pacific food logistics market.

Other drivers and restraints analyzed in the detailed report include:

- Cold Chain Infrastructure Development

- Organized Retail and Modern Trade Growth

- High Capital and Operating Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation commanded 61.34% of the Asia-Pacific food logistics market share in 2025, and value-added services and other logistics solutions are projected to expand at 5.41% CAGR through 2031 for the Asia-Pacific food logistics market size. Road carries the majority of agricultural loads in Thailand, where rail is underused despite per-ton-kilometer advantages, which sustains reliance on flexible last-mile assets for frequent, small-batch replenishment. India's dedicated Reefer Express service connecting ICD Kanpur and Mundra Port was launched in March 2026 to provide a rail corridor with tighter temperature controls and fuel savings on long domestic legs with reliable export handoffs. Warehousing footprints are growing to support omnichannel fulfillment, including temperature-controlled space in regional hubs that can scale multi-category flows for regional and cross-border distribution. Value-added solutions now bundle pre-cooling, portioning, labeling, and automated document checks to reduce handoffs and increase visibility, which aligns with buyer expectations for integrated cold chain orchestration in the Asia-Pacific food logistics market. Certifications such as ISO 9001 and ISO 22000 are becoming common prerequisites for multinational buyers, which push providers to formalize quality procedures and maintain robust documentation across all service lines.

Air freight supports high-value perishables that require rapid international connections, and network upgrades like DHL's expanded Airfreight Cold Chain Network connect more than 30 GDP-compliant hubs with additional routes targeted in Asia. Regional air cargo volumes are projected to rise through 2028, which supports shorter cycles for cross-border shipments of fresh and chilled products. Maritime routes remain central for bulk commodity movements, and Hong Kong's inbound food and beverage volumes in early 2025 confirm stable demand for seaborne distribution. Cross-border trucking is improving under the ASEAN Customs Transit System, and Kuehne+Nagel has added prime movers and containers in Thailand to meet e-commerce and high-tech demand while lowering cost and dwell time at borders. Digital control towers promoted in Singapore enable real-time management of routes and temperature performance, which reduces exception handling and strengthens compliance readiness for shippers across the Asia-Pacific food logistics market.

List of Companies Covered in this Report:

- DHL Group

- Nippon Express Holdings

- Kerry Logistics Network

- Yusen Logistics (Part of NYK Line)

- DSV

- Toll Group

- SF Express

- AIT Worldwide Logistics

- CEVA Logistics

- Kuehne + Nagel

- Kintetsu World Express

- Geodis

- Hellmann Worldwide Logistics

- JWD InfoLogistics

- SEKO Logistics

- Sagawa Express

- Crane Worldwide Logistics

- CWT PTE. LIMITED

- Nichirei Logistics Group

- CJ Rokin Logistic

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Foreign Investment and Logistics Modernization

- 4.2.2 E-commerce and Quick Commerce Boom

- 4.2.3 Cold Chain Infrastructure Development

- 4.2.4 Organized Retail and Modern Trade Growth

- 4.2.5 Cross-Border Food Trade Expansion

- 4.2.6 Food Safety and Quality Standards

- 4.3 Market Restraints

- 4.3.1 Fragmented Cold Chain Infrastructure

- 4.3.2 High Capital and Operating Costs

- 4.3.3 Regulatory Complexity and Inconsistency

- 4.3.4 Infrastructure and Connectivity Challenges

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Hybrid Distribution Models Addressing Diversity

- 4.9 Government-Led Cold Chain Corridors Emerging

5 Market Size & Growth Forecasts

- 5.1 By Services

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Water

- 5.1.1.4 Air

- 5.1.2 Warehousing

- 5.1.3 Value-Added Services and Others

- 5.1.1 Transportation

- 5.2 By Temperature-Control Type

- 5.2.1 Cold Chain

- 5.2.1.1 Ambient (15-25 °C)

- 5.2.1.2 Chilled (2-8 °C)

- 5.2.1.3 Frozen (Less than 0 °C)

- 5.2.2 Non Cold Chain

- 5.2.1 Cold Chain

- 5.3 By End-Product Category

- 5.3.1 Meat & Seafood

- 5.3.2 Dairy & Frozen Desserts

- 5.3.3 Fruits & Vegetables

- 5.3.4 Food and Beverages

- 5.3.5 Others

- 5.4 By Country (Value, USD)

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 South Korea

- 5.4.5 Australia

- 5.4.6 Indonesia

- 5.4.7 Malaysia

- 5.4.8 Philippines

- 5.4.9 Singapore

- 5.4.10 Thailand

- 5.4.11 Vietnam

- 5.4.12 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Nippon Express Holdings

- 6.4.3 Kerry Logistics Network

- 6.4.4 Yusen Logistics (Part of NYK Line)

- 6.4.5 DSV

- 6.4.6 Toll Group

- 6.4.7 SF Express

- 6.4.8 AIT Worldwide Logistics

- 6.4.9 CEVA Logistics

- 6.4.10 Kuehne + Nagel

- 6.4.11 Kintetsu World Express

- 6.4.12 Geodis

- 6.4.13 Hellmann Worldwide Logistics

- 6.4.14 JWD InfoLogistics

- 6.4.15 SEKO Logistics

- 6.4.16 Sagawa Express

- 6.4.17 Crane Worldwide Logistics

- 6.4.18 CWT PTE. LIMITED

- 6.4.19 Nichirei Logistics Group

- 6.4.20 CJ Rokin Logistic

7 Market Opportunities & Future Outlook