PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063357

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063357

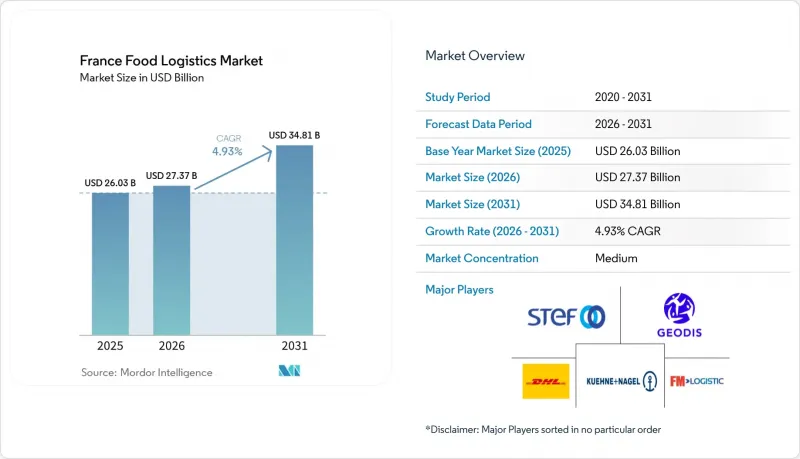

France Food Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the france food logistics market size is expected to increase from USD 26.03 billion in 2025 to USD 27.37 billion in 2026 and reach USD 34.81 billion by 2031, growing at a CAGR of 4.93% over 2026-2031.

Strong demand for certified-organic products, stricter HACCP and ISO 22000 audits, and on-farm cold-storage modernization funded under the Common Agricultural Policy are reshaping facility standards and route design. This report is Segmented by Services (Transportation, Warehousing and Storage, Value-Added Services), by Temperature-Control Type (Cold Chain, Non Cold Chain), and by End-Product Category (Meat/Seafood/Poultry, Dairy Products, Horticulture, Processed Food, Pet Food, and Others). The Market Forecasts are Provided in Terms of Value (USD).

France Food Logistics Market Trends and Insights

Surge in Certified-Organic Food Volumes Requiring Dedicated Cold Logistics

Logistics providers are segmenting warehouses to eliminate cross-contamination and deploying dual-temperature vehicles with Ecocert-approved sanitation regimes, raising fixed costs but unlocking premium contractual yields. Organic dairy lines move faster than conventional SKUs, forcing more frequent route turns, while premium price points 30-50% above conventional support investment in blockchain lot traceability. Niche carriers specializing in organics are capturing business from national retailers who want suppliers that already satisfy audit checklists. Consequently, demand for certified capacity is outstripping supply in high-growth regions such as Occitanie, reinforcing upward pressure on dedicated cold-chain rates.

Tightening HACCP / ISO 22000 Audits Raising Demand for Compliant 3PL Warehouses

Carrefour, Auchan, and other majors now restrict tenders to ISO 22000-accredited depots, compressing the addressable market for non-certified operators. Certification requires documented critical-control protocols and continuous employee training that smaller fleets struggle to finance, accelerating consolidation within the France food logistics market. High-end infant-formula and functional-food shippers are importing GDP standards from pharma, spurring investment in redundant refrigeration and remote-temperature telemetry. As a result, compliant 3PLs can command 8-12% rate premiums, offsetting certification expenses and improving margin resilience.

Scarcity of Natural-Refrigerant Equipment Delaying Fleet & Warehouse Upgrades

Transport units suitable for -25 °C frozen lanes come from only three global OEMs, adding 35-45% to purchase prices. French carriers face a dilemma: pay burgeoning HFC refill costs up 180% since 2022 or wait for back-ordered natural-refrigerant gear and risk service gaps. The talent deficit compounds the bottleneck; an extra 2,500 certified technicians are required by 2027 to install and maintain natural systems. As large 3PLs pre-book factory slots, smaller fleets are left to operate aging kit, tempering modernization across the France food logistics market.

Other drivers and restraints analyzed in the detailed report include:

- Seafood Nearshoring to Brittany & Normandy Boosting Domestic Reefer Mileage

- Common Agricultural Policy Grants Driving On-Farm Cold-Storage Modernization

- Escalating Insurance Premiums Linked to Temperature-Excursion Liability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation retained a 46.24% grip on France food logistics market share in 2025, yet its growth is muted by driver shortages and volatile diesel prices, whereas value-added services are climbing at 7.49% CAGR. This shift shows that shippers prefer single-invoice partners who can handle blast freezing, kitting, and lot-traceability under one food-safety umbrella. The France food logistics market size attached to co-packing lines is rising as retailers launch ready-meal bundles that require synchronized portioning and cold assembly. Robotics adoption inside value-added facilities improves accuracy to +-0.5 °C in blast-freeze cycles, reducing cell damage in high-moisture SKUs and strengthening contractual KPIs.

Spot trucking rates fell 8-12% in 2024-2025, forcing pure haulers to explore intermodal offerings or cede share to integrated 3PLs. Rail's subsidy-backed advance adds resilience, yet scheduling rigidity still caps its share below 8% of cold volumes. Several 3PLs are therefore bundling road-rail packages that guarantee next-day Paris arrival while cutting CO2 per pallet by 70%. Across the France food logistics industry, service diversification is the main hedge against input-price swings and capacity overhangs.

List of Companies Covered in this Report:

- STEF

- GEODIS

- DHL Group

- Kuehne + Nagel

- Denjean Logistique

- Groupe Olano

- XPO

- FM Logistic

- DSV (Incl. DB Schenker)

- Dachser

- Transgourmet France

- Ceva Logistics (CMA CGM)

- Constellation Cold Logistics

- Rhenus Logistics

- Lacroix Logistics

- Delanchy Group

- Le Roy Logistique

- DGS Transports

- Yusen Logistics

- AIT Worldwide Logistics, Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Certified-Organic Food Volumes Requiring Dedicated Cold Logistics

- 4.2.2 Tightening HACCP / ISO 22000 Audits Raising Demand for Compliant 3PL Warehouses

- 4.2.3 Seafood Nearshoring to Brittany & Normandy Boosting Domestic Reefer Mileage

- 4.2.4 Common Agricultural Policy (CAP) Grants Driving On-Farm Cold-Storage Modernization

- 4.2.5 Reopening of Perpignan-Rungis Refrigerated Rail Corridor Expanding Multimodal Options

- 4.2.6 Renewable-Energy Ammonia Refrigeration Hubs Lowering Rural Distribution Costs

- 4.3 Market Restraints

- 4.3.1 Scarcity of Natural-Refrigerant Equipment Delaying Fleet & Warehouse Upgrades

- 4.3.2 Municipal Axle-Weight Limits on Secondary Roads Constraining High-Capacity Reefers

- 4.3.3 Escalating Insurance Premiums Linked to Temperature-Excursion Liability

- 4.3.4 Data Fragmentation Among SMEs Hindering End-To-End Cold-Chain Visibility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Services

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Sea and Inland Water

- 5.1.1.4 Air

- 5.1.2 Warehousing and Storage

- 5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

- 5.1.1 Transportation

- 5.2 By Temperature-Control Type

- 5.2.1 Cold Chain

- 5.2.1.1 Ambient (15-25 °C)

- 5.2.1.2 Chilled (2-8 °C)

- 5.2.1.3 Frozen (Less than 0 °C)

- 5.2.2 Non Cold Chain

- 5.2.1 Cold Chain

- 5.3 By End-Product Category

- 5.3.1 Meat, Seafood, and Poultry

- 5.3.2 Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.)

- 5.3.3 Horticulture (Fresh Fruits & Vegetables)

- 5.3.4 Processed Food Products

- 5.3.5 Pet Food

- 5.3.6 Others (Spreads, Seasoning, dressing, Specialty & Functional Foods, etc.)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 STEF

- 6.4.2 GEODIS

- 6.4.3 DHL Group

- 6.4.4 Kuehne + Nagel

- 6.4.5 Denjean Logistique

- 6.4.6 Groupe Olano

- 6.4.7 XPO

- 6.4.8 FM Logistic

- 6.4.9 DSV (Incl. DB Schenker)

- 6.4.10 Dachser

- 6.4.11 Transgourmet France

- 6.4.12 Ceva Logistics (CMA CGM)

- 6.4.13 Constellation Cold Logistics

- 6.4.14 Rhenus Logistics

- 6.4.15 Lacroix Logistics

- 6.4.16 Delanchy Group

- 6.4.17 Le Roy Logistique

- 6.4.18 DGS Transports

- 6.4.19 Yusen Logistics

- 6.4.20 AIT Worldwide Logistics, Inc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment