PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063358

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063358

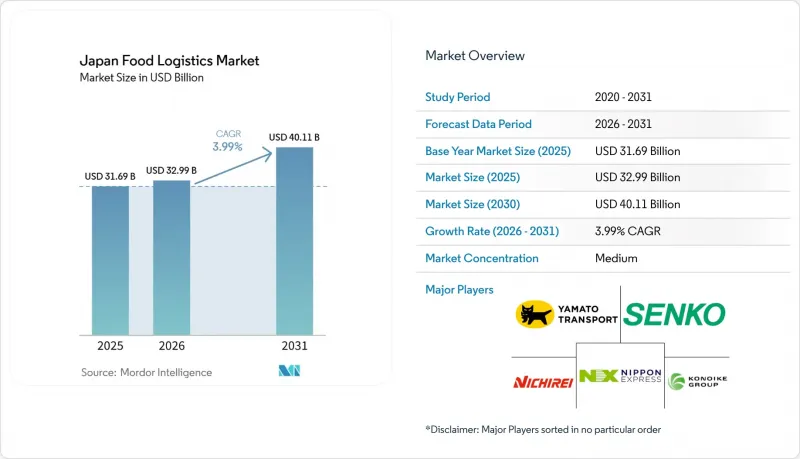

Japan Food Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the japan food logistics market size is projected to be USD 31.69 billion in 2025, USD 32.99 billion in 2026, and reach USD 40.11 billion by 2031, growing at a CAGR of 3.99% from 2026 to 2031.

A measured headline growth rate conceals big structural change. This report is Segmented by Services (Transportation (Road, Rail, Sea and Inland Water, Air), Warehousing and Storage, Value-Added Services), by Temperature-Control Type (Cold Chain (Ambient, Chilled, Frozen), Non-Cold Chain), by End-Product Category (Meat/Seafood/Poultry, Dairy Products, Horticulture, Processed Foods, Pet Food, Others). The Market Forecasts are Provided in Terms of Value (USD).

Japan Food Logistics Market Trends and Insights

Surge in Pharmaceutical Cold-Chain Cross-Utilization

Hybrid networks now shift refrigerated trucks from morning drug deliveries to afternoon fresh-food runs, aligning 2-8 °C requirements across both cargo types and lifting food volumes to 15-22% of pharmaceutical fleet capacity. Higher specification control trims waste, extends shelf life, and supports premium pricing for imports such as Norwegian salmon and Australian chilled beef. Operators capture new revenue without major capital outlay, so hybrid services should keep widening until dedicated food-only fleets lose cost competitiveness.

Corporate Scope-3 Emission Audits Prompting Supplier Consolidation

Nestle Japan, Unilever, and peer producers have cut carrier counts from 15-20 to as few as five strategic partners, achieving 12-18% carbon-intensity improvement per ton-kilometer. Carriers offering real-time CO2 dashboards, electric trucks, and LNG tractors win multi-year contracts that guarantee baseline volumes and co-fund decarbonization pilots. The trend erects entry barriers for small regional haulers lacking measurement capacity and accelerates roll-up activity as larger 3PLs buy route density.

Escalating Insurance Premiums Covering Temperature Excursions

Premiums for cold-chain cargo jumped 35-50% between 2024 and 2025, with underwriters insisting on continuous IoT monitoring and documented contingency plans. Claims now average USD 180,000 per incident, prompting small fleets either to absorb margin-sapping policy costs or risk operating uninsured. Large 3PLs respond with predictive maintenance and dual-compressor trailers that satisfy insurer checklists and wave through at lower rates.

Other drivers and restraints analyzed in the detailed report include:

- Ageing Population Driving High-Frequency Small-Lot Chilled Runs

- National Food-Security Stock Freezer Initiatives

- Constrained Grid Connections for High-Power Refrigeration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation retained 45.72% of the Japan food logistics market share in 2025, anchored by the country's intricate road network that supports the daily replenishment of thousands of convenience stores. Yet value-added services are the clear pace-setter, growing at 6.55% CAGR as manufacturers push postponement to the edge of consumption and outsource blast freezing, labeling, and kitting to logistics specialists. The Japan food logistics market size tied to warehousing also rises as automated multi-temperature DCs blend storage with light processing, enabling next-day ecommerce grocery fulfillment in megacities.

Rail freight's renaissance on the Hokkaido-Honshu corridor now shaves 15-25% off unit cost versus trucking for bulk frozen cargo, while sea transport covers inter-island lanes and bulk imports. Air remains a boutique channel for premium perishables such as uni and Pacific bluefin tuna, where shelf-life economics justify charter rates. Together, multimodal options give shippers flexibility to match speed, cost, and carbon objectives without compromising cold-chain integrity.

List of Companies Covered in this Report:

- Yamato Transport Co., Ltd.

- Nippon Express Holdings Inc.

- Nichirei Logistics Group Inc.

- Konoike Transport Co., Ltd.

- Senko Co., Ltd.

- Mitsubishi Logistics Corporation

- NYK Line (Including Yusen Logistics Co., Ltd.)

- Itochu Logistics Corp.

- Suzuyo Logistics Japan

- Sankyu Inc.

- Kintetsu World Express

- DHL Group

- CMA CGM Group (Including CEVA Logistics)

- JWD InfoLogistics

- SEKO Logistics

- SF Express (Kex-SF)

- GEODIS

- C&F Logistics Holdings Co., Ltd.

- Sagawa Express Co., Ltd.

- Toll Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Pharmaceutical Cold-Chain Cross-Utilization

- 4.2.2 Corporate Scope-3 Emission Audits Prompting Supplier Consolidation

- 4.2.3 Ageing Population Driving High-Frequency Small-Lot Chilled Runs

- 4.2.4 National Food-Security Stock Freezer Initiatives

- 4.2.5 Port Digitalization Slashing Reefer Dwell Times

- 4.2.6 Urban Tax Breaks for Automated Vertical Cold-Storage Sites

- 4.3 Market Restraints

- 4.3.1 Escalating Insurance Premiums Covering Temperature Excursions

- 4.3.2 Constrained Grid Connections for High-Power Refrigeration

- 4.3.3 Night-Time Delivery Noise Ordinance Constraints

- 4.3.4 Delayed Certification Pipeline for HFC-Free Cooling Systems

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Services

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Sea and Inland Water

- 5.1.1.4 Air

- 5.1.2 Warehousing and Storage

- 5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

- 5.1.1 Transportation

- 5.2 By Temperature-Control Type

- 5.2.1 Cold Chain

- 5.2.1.1 Ambient (15-25 °C)

- 5.2.1.2 Chilled (2-8 °C)

- 5.2.1.3 Frozen (Less than 0 °C)

- 5.2.2 Non Cold Chain

- 5.2.1 Cold Chain

- 5.3 By End-Product Category

- 5.3.1 Meat, Seafood, and Poultry

- 5.3.2 Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.)

- 5.3.3 Horticulture (Fresh Fruits and Vegetables)

- 5.3.4 Processed Food Products

- 5.3.5 Pet Food

- 5.3.6 Others (Spreads, Seasoning, Dressing, Specialty and Functional Foods, etc.)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, Recent Developments)

- 6.4.1 Yamato Transport Co., Ltd.

- 6.4.2 Nippon Express Holdings Inc.

- 6.4.3 Nichirei Logistics Group Inc.

- 6.4.4 Konoike Transport Co., Ltd.

- 6.4.5 Senko Co., Ltd.

- 6.4.6 Mitsubishi Logistics Corporation

- 6.4.7 NYK Line (Including Yusen Logistics Co., Ltd.)

- 6.4.8 Itochu Logistics Corp.

- 6.4.9 Suzuyo Logistics Japan

- 6.4.10 Sankyu Inc.

- 6.4.11 Kintetsu World Express

- 6.4.12 DHL Group

- 6.4.13 CMA CGM Group (Including CEVA Logistics)

- 6.4.14 JWD InfoLogistics

- 6.4.15 SEKO Logistics

- 6.4.16 SF Express (Kex-SF)

- 6.4.17 GEODIS

- 6.4.18 C&F Logistics Holdings Co., Ltd.

- 6.4.19 Sagawa Express Co., Ltd.

- 6.4.20 Toll Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment