PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063271

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063271

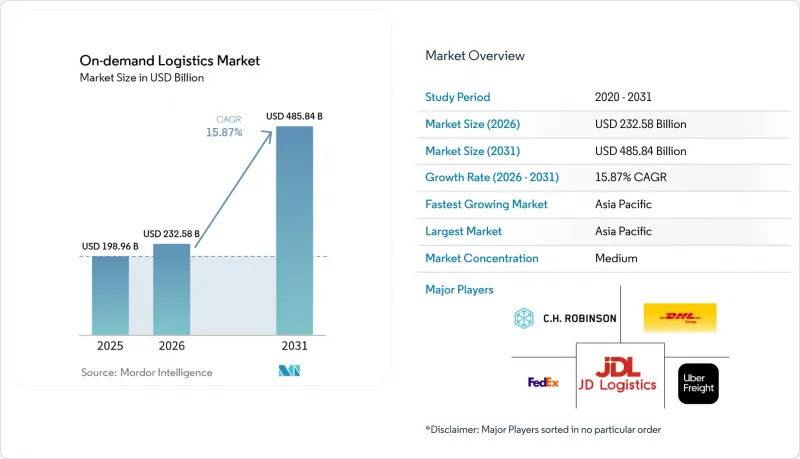

On-demand Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the on-demand logistics market size is projected to expand from USD 198.96 billion in 2025 and USD 232.58 billion in 2026 to USD 485.84 billion by 2031, registering a CAGR of 15.87% between 2026 and 2031.

Consumer expectations for near-instant delivery have turned what was once a premium perk into a baseline service requirement, accelerating platform investment in real-time routing, micro-fulfillment, and embedded payments. This report is Segmented by Service Type (On-Demand Transportation Services, On-Demand and More), by End-User Industry (E-Commerce and Retail, Consumer Packaged Goods, Food and Beverage, Healthcare and Pharma, and More), by Mode of Operation (B2C, B2B, C2C), Enterprise Size (Large Enterprises, Smes), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global On-demand Logistics Market Trends and Insights

Quick-Commerce Grocery Model Proliferation

Ten-minute grocery delivery reshapes urban retail by breaking the weekly shop into multiple micro-purchases, fulfilled from dark stores within a two-kilometer radius of dense neighborhoods. Getir's recent retreat from several European countries after USD 2 billion in losses illustrates how profitability hinges on order density. Yet, surviving players consolidate enough volume to achieve break-even at under 30 orders per rider shift. Indian platforms such as Blinkit and Zepto are scaling thousands of micro-fulfillment sites, pressuring legacy grocers to retrofit distribution centers for hourly inventory turns. Repurposed secondary retail real estate keeps fixed costs in check, and QR-code pick systems reduce dwell time to 15 seconds per SKU, raising labor productivity by 40%. For the On-demand logistics market, the quick-commerce race sustains premium pricing for bike-based last-mile capacity while locking in recurring demand from subscription-style grocery baskets.

SaaS Route-Optimization Uptake Among 3PLs

Cloud-native transportation software trims 15-20% of operating costs by balancing traffic data, driver hours, and vehicle capacity in real time. The subscription model removes heavy up-front licenses, enabling mid-size 3PLs to compete with global integrators. Continuous telemetry loops feed machine-learning engines that fine-tune delivery windows, steadily driving down empty miles across the On-demand logistics market. Compliance modules embed rules for hazmat, weight limits, and labor mandates, shielding operators from fines and litigation. Network effects emerge as anonymized route data improves algorithm accuracy for every new participant, expanding the addressable base for SaaS vendors.

Gig-Economy Worker Reclassification Cost Pressures

The United States Department of Labor's January 2026 six-factor test blurs the contractor-employee divide, potentially adding payroll taxes, health benefits, and workers' compensation costs that compress gross margins by up to 6 percentage points. Spain's Rider Law and similar EU statutes flip the burden of proof onto platforms, triggering local court battles over back pay. Operators hedge by trialing hybrid rosters where core demand is met with employees while peaks are subcontracted, though regulators question the permanence of such dual systems. Compliance complexity multiplies for platforms spanning 30+ jurisdictions, prompting higher legal and HR spend across the On-demand logistics market. Some providers respond with automation initiatives, such as delivery robots, lockers, and drones, to decouple capacity growth from headcount risk.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Cross-Border E-commerce Parcels

- Corporate ESG Mandates Favoring Green Slot Consolidation

- Geopolitical Air-Cargo Lane Disruptions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Value-added services carved 16.34% CAGR through 2031, demonstrating customer appetite for integrated warehousing, reverse logistics, and analytics that extend beyond simple drop-off. In contrast, on-demand transportation retained 61.54% On-demand logistics market share in 2025 due to its ubiquity in last-mile workflows. Providers leverage "store-and-ship" bundles, short-term storage paired with instant dispatch to lock in clients uneasy about separate suppliers for inventory and delivery. The On-demand logistics market size for fulfillment modules is projected to expand faster than line-haul because packaging, labeling, and returns each create additive fee layers. Reverse logistics, critical for apparel where return ratios hover near 25%, commands premium pricing given inspection and refurbishment requirements. Operators that master these adjacencies see customer churn fall by up to 40%, signaling that end-to-end visibility trumps the lowest per-mile rate in enterprise tender decisions.

Second-order impacts surface in network design: dark stores double as forward stock locations, trimming delivery radius and boosting same-hour hit rates. Data exhaust from pick-pack steps feeds demand forecasts that in turn cut stock-outs on D2C sites, forming a positive feedback loop. Cross-selling analytics dashboards accelerates wallet share, with some 3PLs reporting 25% of 2025 revenue from software subscriptions rather than physical movement. As the On-demand logistics market matures, differentiation shifts from pure speed to accuracy, sustainability reporting, and friction-free returns, all of which sit squarely inside the value-added playbook.

E-commerce and retail captured 26.03% of the On-demand logistics market in 2025, yet healthcare logistics is poised to be the fastest riser at 19.80% CAGR through 2031. Temperature-controlled services gain urgency as global biologics pipelines swell; DHL earmarked EUR 2 billion (USD 2.35 billion) for GDP-certified hubs and active-container fleets by 2030. Tight regulatory windows 2-8 °C within +-1 °C require redundant monitoring, pushing per-shipment revenue 3-5 times higher than fashion parcels. In emerging markets, cold-chain penetration currently under 15% represents a blue-ocean growth lever for the On-demand logistics industry. Aging demographics in Japan, the EU, and the United States raise chronic-care drug volumes, locking in secular demand insulated from consumer-spending swings.

Parallel to pharma, food and beverage rely on similar thermal protocols, enabling asset reutilization across verticals and smoothing capacity utilization curves. Industrial users pivot toward emergency parts delivery to curtail factory downtime, adopting premium same-day courier loops once reserved for retail. This convergence flattens seasonality, giving network planners steadier asset turns and healthier free cash flow. Within the On-demand logistics market, sector diversity therefore acts as a hedge, buffering cyclical dips in discretionary e-commerce with inelastic medical shipments.

Geography Analysis

Asia Pacific generated 42.91% of the On-demand logistics market share in 2025 and is forecast to post an 18.28% CAGR to 2031, lifted by urban density and mobile-first retail ecosystems. China's live-commerce turnover hit RMB 4.9 trillion (USD 699.84 billion) in 2023, with embedded one-click checkout translating into sub-60-minute delivery in tier-1 cities. Southeast Asia's super-apps, led by Grab, bundle ride-hailing, payments, and parcel dispatch, creating multi-service engagement loops that lock in 42 million monthly active users. Japan confronts a driver shortage that threatens 278,000 vacancies by 2028, prompting policy support for drones and autonomous sidewalk robots. These innovations, once proven, are exported to developing neighbors, reinforcing Asia Pacific's status as the lead market for rapid-delivery playbooks.

North America, despite platform maturity, still exhibits white space in rural zones; Amazon's USD 4 billion 2025-2026 program to serve 4,000 smaller towns shows latent upside when hub-and-spoke models extend beyond metropolitan rings. Sustainability dominates European strategy. EU alternative-fuel rules accelerate electric-van procurement and hydrogen corridor construction, enabling carriers to cut Scope 3 emissions and charge green premiums. Latin America rides a nearshoring boom as manufacturers hedge China exposure by adding Mexican capacity; MercadoLibre's USD 2.5 billion logistics spend exemplifies how regional champions integrate warehousing and last mile under one pane of glass.

In the Middle East and Africa, infrastructure gaps spur leapfrogging mobile wallets and pickup lockers offset limited home addressing systems. Yet geopolitical conflict along major air corridors injects cost volatility, compelling operators to pre-position stock in Gulf free-zones to sidestep airspace closures. Collectively, regional diversification cushions the On-demand logistics market against localized shocks, ensuring global providers can re-route volume to whichever lanes remain fluid.

- Uber Technologies (Including Uber Freight)

- DHL Group

- FedEx

- JD Logistics

- C.H. Robinson Worldwide

- Delhivery

- J.B. Hunt 360

- XPO, Inc.

- Grab Holdings, Ltd.

- Gojek (GoSend)

- Flowspace

- Flexe

- Lalamove

- Sennder

- Shadowfax

- United Parcel Service of America, Inc. (UPS)

- Glovo

- Bringg

- Shiprocket

- Cargomatic

- GoShare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Quick-Commerce Grocery Model Proliferation

- 4.2.2 Saas Route-Optimization Uptake Among 3PLs

- 4.2.3 Surge In Cross-Border E-Commerce Parcels

- 4.2.4 Corporate ESG Mandates Favoring Green Slot Consolidation

- 4.2.5 Creator-Commerce Live-Shopping Fulfillment Needs

- 4.2.6 Real-Time Payment Rails Enabling Instant Courier Payouts

- 4.3 Market Restraints

- 4.3.1 Gig-Economy Worker Reclassification Cost Pressures

- 4.3.2 Geopolitical Air-Cargo Lane Disruptions

- 4.3.3 Lithium-Battery Safety Limits on E-Bike Fleet Density

- 4.3.4 Algorithmic Price-Setting Litigation Exposure

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

- 4.5 Value / Supply-Chain Analysis

- 4.6 Technological Innovations in the Industry

- 4.7 Government Regulations and Policies

- 4.8 Impact of Geopolitical Events on the Market

5 Market Size and Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 On-demand Transportation Services

- 5.1.1.1 Road Freight

- 5.1.1.2 Air Freight

- 5.1.1.3 Rail Freight

- 5.1.1.4 Sea and Inland Waterways

- 5.1.2 On demand Warehousing and Fulfillment Services

- 5.1.2.1 On demand Storage

- 5.1.2.2 Order Fulfillment and Distribution

- 5.1.2.3 Other Warehousing and Fulfillment Services

- 5.1.3 Value-Added Services

- 5.1.1 On-demand Transportation Services

- 5.2 By End-User Industry

- 5.2.1 E-commerce and Retail

- 5.2.2 Consumer Packaged Goods

- 5.2.3 Food and Beverage (incl. Cold-chain)

- 5.2.4 Healthcare and Pharma

- 5.2.5 Industrial and Manufacturing

- 5.2.6 Others

- 5.3 By Mode of Operation

- 5.3.1 B2C (Business-to-Consumer)

- 5.3.2 B2B (Business-to-Business)

- 5.3.3 C2C (Consumer-to-Consumer)

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-sized Enterprises (SMEs)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Southeast Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 Europe

- 5.5.4.1 United Kingdom

- 5.5.4.2 Germany

- 5.5.4.3 France

- 5.5.4.4 Spain

- 5.5.4.5 Italy

- 5.5.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.4.8 Rest of Europe

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Uber Technologies (Including Uber Freight)

- 6.4.2 DHL Group

- 6.4.3 FedEx

- 6.4.4 JD Logistics

- 6.4.5 C.H. Robinson Worldwide

- 6.4.6 Delhivery

- 6.4.7 J.B. Hunt 360

- 6.4.8 XPO, Inc.

- 6.4.9 Grab Holdings, Ltd.

- 6.4.10 Gojek (GoSend)

- 6.4.11 Flowspace

- 6.4.12 Flexe

- 6.4.13 Lalamove

- 6.4.14 Sennder

- 6.4.15 Shadowfax

- 6.4.16 United Parcel Service of America, Inc. (UPS)

- 6.4.17 Glovo

- 6.4.18 Bringg

- 6.4.19 Shiprocket

- 6.4.20 Cargomatic

- 6.4.21 GoShare

7 Market Opportunities and Future Outlook