PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063272

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063272

Asia-Pacific Government And Education Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

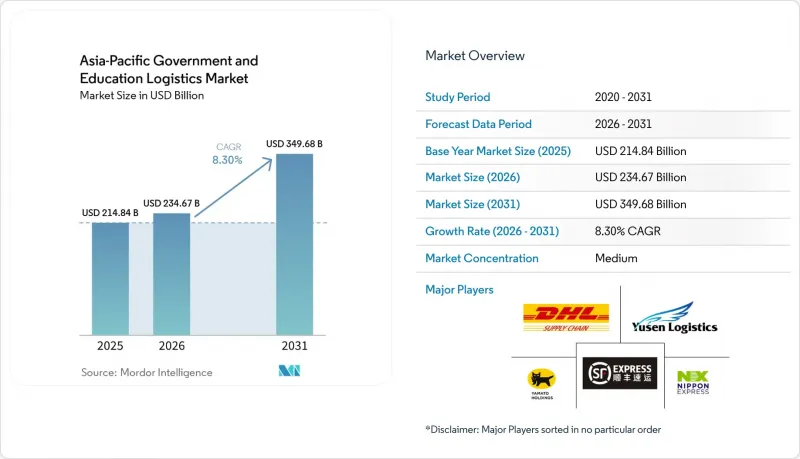

According to Mordor Intelligence, the asia-Pacific government and education logistics market size is expected to grow from USD 214.84 billion in 2025 to USD 234.67 billion in 2026 and is forecast to reach USD 349.68 billion by 2031 at an 8.30% CAGR over 2026-2031.

The growth path reflects rising defense self-sufficiency, large-scale digital-learning roll-outs, and public-private outsourcing frameworks that are redrawing supply-chain responsibilities across the region. This report is Segmented by Service Type (Transportation, Including Road, Rail, Air, Sea, and More), by End-User (Central/Federal Government, State and Local Government, and More), and by Geography (China, India, Japan, South Korea, Australia, Indonesia, Thailand, Vietnam, Malaysia, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Government And Education Logistics Market Trends and Insights

Large-Scale E-Governance & Smart-Infrastructure Stimulus Packages

National digital-government programs are injecting sustained logistics demand by funding hardware roll-outs, cloud-migration projects, and data-center construction. India's Digital India initiative allocated USD 30 billion to digital infrastructure, creating continuous freight flows to 250,000 offices and 1.5 million schools. Indonesia's USD 32 billion Nusantara smart-capital project similarly requires synchronized multi-agency freight coordination. Vietnam's Framework 4.0 mandates cloud-based services throughout ministries by 2027, amplifying the need for secure transportation of critical ICT equipment. Philippine ICT guidelines now score bidders on cybersecurity capacity, pushing third-party providers to certify ISO 27001 systems. Together, these programs provide multi-year visibility for providers but fragment tender cycles across national and provincial entities.

Escalating Regional Defense Procurement (AUKUS, QUAD) Fuelling Secure 3PL Demand

Defense modernization accelerates cargo streams that must meet stringent clearance and chain-of-custody standards. Australia's USD 368 billion AUKUS submarine program demands nuclear-propulsion component logistics that only vetted contractors can perform. The QUAD Supply Chain Resilience Initiative aligns security procedures across Australia, India, Japan, and the United States, creating designated corridors for dual-use items. Japan is lifting defense outlays to 2% of GDP by 2027, triggering new storage and transport needs for ammunition and high-value systems. South Korea's push for indigenous platforms adds reverse-logistics complexity. Providers with existing defense accreditations, therefore, capture premium pricing while newcomers face high entry barriers.

Aging Truck Driver Workforce & Widening Talent Gaps in APAC

Japan reports 47% of drivers above 50, with retirements accelerating capacity shortfalls. Australia recorded 26,000 vacancies in 2024, compounded by defense-security clearance hurdles. South Korea's wages jumped 18% year on year, while Thailand struggles to staff rural routes due to limited vocational schools. Providers respond with signing bonuses, simulators, and early autonomous trials, but regulatory lag slows full driverless deployment for government cargo.

Other drivers and restraints analyzed in the detailed report include:

- Public-Private Partnership Outsourcing Wave Across Ministries & Universities

- Climate-Resilient Redundant Warehousing Mandates After 2023 Flood Disruptions

- Volatile Bunker Fuel Surcharges Stressing Fixed-Budget Education Shipments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Value-added services secured a 9.30% CAGR through 2031, well above the broader Asia-Pacific government and education logistics market share for the transportation sector. In 2025, transportation preserved 59.89% share, underlining the scale of basic freight demand. Yet commoditization, driver shortages, and stricter carbon caps curb rate upside, pushing operators to bundle customs, blockchain stamping, and ESG dashboards. Rail corridors, especially India's dedicated freight routes, trim textbook lead-times by 30-40% and reduce diesel exposure. Air freight remains a niche for official documents and emergency relief, commanding premiums that offset low tonnage. Sea and inland waterways stay critical for archipelagic deliveries, though fuel risk shifts toward long-term charterers. Warehousing gains from climate-resilient upgrades, with elevated racks and dual-power systems now baseline specifications across Thailand and Vietnam.

Micro-fulfillment hubs multiply on campuses, requiring small-footprint automation and API links to student portals. Consequently, providers integrating these components into one invoice realize higher margins and deepen client lock-in. Market leaders differentiate through ISO 27001 data centers, zero-knowledge encryption modules, and on-site customs desks. Lagging freight forwarders that lack cybersecurity credentials risk relegation to subcontract status, losing pricing power and strategic influence.

List of Companies Covered in this Report:

- DHL Supply Chain & Global Forwarding

- Nippon Express Holdings

- Yamato Holdings

- Yusen Logistics

- SF Express (Group) Co., Ltd.

- DSV

- Kuehne + Nagel

- CEVA Logistics

- CJ Logistics

- Kerry Logistics Network

- Sinotrans Limited

- Toll Group

- Sagawa Express

- Gati Ltd

- Allcargo Logistics

- Linfox

- AIT Worldwide Logistics

- Rhenus Logistics

- JD Logistics

- Kintetsu World Express

- Delhivery

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Large-Scale e-Governance & Smart-Infrastructure Stimulus Packages

- 4.2.2 Escalating Regional Defence Procurement (AUKUS, QUAD) Fuelling Secure 3PL Demand

- 4.2.3 Public-Private Partnership (PPP) Outsourcing Wave Across Ministries & Universities

- 4.2.4 Climate-Resilient Redundant Warehousing Mandates after 2023 Flood Disruptions

- 4.2.5 Blockchain Authentication of Educational Content to Curb Counterfeit Textbooks

- 4.2.6 Micro-Fulfilment Hubs on University Campuses for On-Demand Learning Kits

- 4.3 Market Restraints

- 4.3.1 Ageing Truck Driver Workforce & Widening Talent Gaps in APAC

- 4.3.2 Volatile Bunker Fuel Surcharges Stressing Fixed-Budget Education Shipments

- 4.3.3 Mandatory Zero-Knowledge Encryption for Defence Cargo Limiting Data Visibility

- 4.3.4 ESG Tier-1 Audit Requirements Adding Compliance Costs for SME Contractors

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

- 4.5 Value / Supply-Chain Analysis

- 4.6 Technological Innovations in the Industry

- 4.7 Government Regulations and Policies

- 4.8 Impact of Geopolitical Events on the Market

5 Market Size and Growth Forecasts (Value, USD Billion)

- 5.1 By Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Air

- 5.1.1.4 Sea and Inland Waterway

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-Added Services

- 5.1.1 Transportation

- 5.2 By End-User

- 5.2.1 Central/Federal Government

- 5.2.2 State and Local Government

- 5.2.3 Defense Agencies

- 5.2.4 Public Education (K-12)

- 5.2.5 Higher Education Institutions

- 5.2.6 Others

- 5.3 By Country

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 Australia

- 5.3.6 Indonesia

- 5.3.7 Thailand

- 5.3.8 Vietnam

- 5.3.9 Malaysia

- 5.3.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Supply Chain & Global Forwarding

- 6.4.2 Nippon Express Holdings

- 6.4.3 Yamato Holdings

- 6.4.4 Yusen Logistics

- 6.4.5 SF Express (Group) Co., Ltd.

- 6.4.6 DSV

- 6.4.7 Kuehne + Nagel

- 6.4.8 CEVA Logistics

- 6.4.9 CJ Logistics

- 6.4.10 Kerry Logistics Network

- 6.4.11 Sinotrans Limited

- 6.4.12 Toll Group

- 6.4.13 Sagawa Express

- 6.4.14 Gati Ltd

- 6.4.15 Allcargo Logistics

- 6.4.16 Linfox

- 6.4.17 AIT Worldwide Logistics

- 6.4.18 Rhenus Logistics

- 6.4.19 JD Logistics

- 6.4.20 Kintetsu World Express

- 6.4.21 Delhivery

7 Market Opportunities and Future Outlook