PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063303

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063303

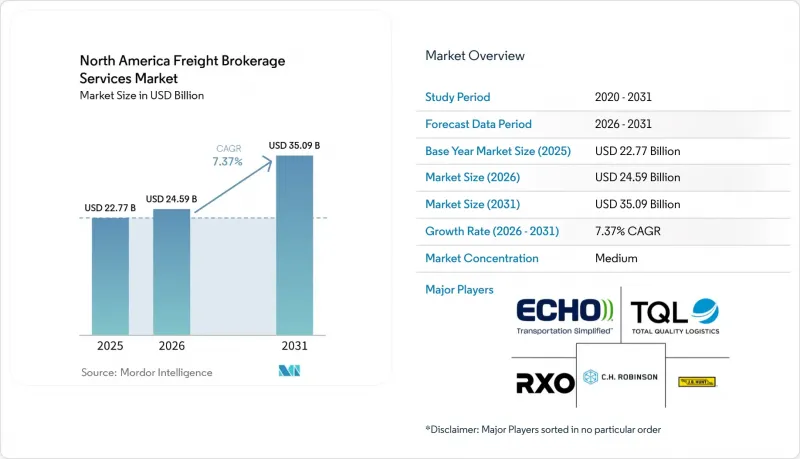

North America Freight Brokerage Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america freight brokerage services market size is projected to expand from USD 22.77 billion in 2025 and USD 24.59 billion in 2026 to USD 35.09 billion by 2031, registering a 7.37% CAGR between 2026 and 2031.

This report is Segmented by Service (Full-Truckload, and More), by Equipment/Trailer Type (Dry Van, and More), by Haul Length (Long-Haul, and More), by Business Model (Traditional, and More), by End-User Industry (Manufacturing, and More), by Customer Size (Large Enterprise, and More), and by Country (United States, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America Freight Brokerage Services Market Trends and Insights

AI-Driven Lane-Level Dynamic Pricing Accelerates Broker Win-Rates

Machine learning now prices individual lanes using live capacity signals and competitive quotes. C.H. Robinson's AI agents processed over 3 million shipment tasks in 2025, trimming quote-to-accept cycles to minutes and widening margin capture on volatile corridors. Sophisticated models digest historical tender outcomes, weather, and dwell-time metrics to forecast service risk, raising shipper confidence during bid events. Large intermediaries with deep data logs sharpen algorithms faster than smaller rivals, tilting share toward incumbents that reinvest savings into carrier loyalty programs. The dynamic pricing edge is most pronounced on Laredo and Nogales cross-border lanes, where real-time wait times swing spot rates all day. Smaller brokers counter by niching into flatbed or hazmat niches where algorithmic rate history is sparse.

USMCA-Enabled Cross-Border E-Commerce Shipments Spur Expedited Brokerage Demand

De minimis thresholds under USMCA simplify small-parcel customs, unleashing direct-to-consumer flows from Mexican facilities into US households. Brokers blend parcel carriers with LTL consolidators to clear customs in bulk, then inject parcels into domestic hubs, shaving days off transit. Bilingual operations teams manage certificates of origin that still accompany mixed-case pallets, protecting shippers from audits. Competitive edges arise for brokers certified under CTPAT and FAST programs that fast-track northbound vehicles. Growth potential is magnified by electronics and apparel sellers that now promise seventy-two-hour cross-border delivery windows.

Large Shippers' Direct Digital Carrier Platforms Disintermediate Traditional Brokers

Fortune 500 retailers deploy API hubs that pull live rates from contract carriers, bypassing intermediaries for predictable lanes. IntelliTrans now connects mill shippers with 2,800 carriers in real time, reserving broker use only for cross-border or oversized freight. Brokers respond by packaging exception management, detention shields, and guaranteed capacity bundles that software alone cannot match. Margin loss is acute on head-haul lanes in the Southeast, where carrier density is highest. Smaller brokers risk being locked out of enterprise routing guides if they cannot feed rates via standardized APIs.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Scope-3 Mandates Fuel Broker-Led Carbon-Optimized Routing

- Early Commercialization of Autonomous-Truck Capacity Pools via Broker Networks

- State-Level Co-Employment & Liability Statutes Inflate Legal Exposure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Less-than-truckload revenue is advancing at a 9.66% CAGR, lifted by USD 850 billion in e-commerce returns that now span LTL and parcel blends. Consolidators leverage pool points near Chicago and Dallas, where high parcel density lowers cost per return. Full truckload still anchors 71.05% of the North America freight brokerage services market share in 2025, yet automated carrier apps are eroding routine lane volumes, squeezing brokerage margins.

Digital brokers embed both modes in one dashboard, enabling merchants to toggle between pallet and parcel at late cut-off without re-tendering. Service differentiation pivots on claims handling, as apparel and electronics returns demand speedy refurbishment. Brokers that integrate point-of-sale refund triggers with freight scheduling deepen retailer loyalty and raise switching costs within the North America freight brokerage services market.

Refrigerated capacity is climbing at a 9.97% CAGR as pharma and meal-kit shippers seek sub-two-degree compliance from pickup to doorstep. Dry van leads with 43.78% of the North America freight brokerage services market size in 2025, yet spot-rate volatility remains high because of chassis shortages at West Coast ports.

Autonomous trials favor reefers that run overnight when traffic is low, boosting asset utilization. Brokers deploy telematics hubs that capture temperature spikes and push proactive alerts, reducing OS&D claims. Tanker and flatbed niches hold stable revenue but add complexity through hazmat and over-dimensional permits, insulating niche brokers from algorithmic commoditization across the North America freight brokerage services market.

List of Companies Covered in this Report:

- C.H. Robinson Worldwide

- Total Quality Logistics (TQL)

- Echo Global Logistics, Inc.

- RXO

- J.B. Hunt Transport Services, Inc.

- Hub Group, Inc.

- Landstar System

- Schneider Logistics

- WWEX Group

- Arrive Logistics

- Mode Transportation

- BlueGrace Logistics

- Nolan Transportation Group

- Sunset Transportation

- Werner Enterprises

- Trinity Logistics

- Ascent Global Logistics

- Integrity Express Logistics

- Redwood Logistics

- PLS Logistics Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Driven Lane-Level Dynamic Pricing Accelerates Broker Win-Rates

- 4.2.2 USMCA -Enabled Cross-Border E-Commerce Shipments Spur Expedited Brokerage Demand

- 4.2.3 Corporate Scope-3 Mandates Fuel Adoption of Broker-Led Carbon-Optimized Routing

- 4.2.4 Early Commercialization of Autonomous-Truck Capacity Pools via Broker Networks

- 4.2.5 Integrated LTL-Parcel Consolidation Models Expand Broker Share of Returns Logistics

- 4.2.6 Real-Time Compliance Analytics from ELD/Telematics Unlock Detention-Free SLAs

- 4.3 Market Restraints

- 4.3.1 Large Shippers' Direct Digital Carrier Platforms Disintermediate Traditional Brokers

- 4.3.2 State-Level Co-Employment and Liability Statutes (e.g., AB5) Inflate Legal Exposure

- 4.3.3 Load-Board Data Oligopoly Limits Analytics Access for Small and Mid-Sized Brokers

- 4.3.4 Rising Cybersecurity and Data-Privacy Compliance Costs (CISA/NIST Frameworks)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers (Carriers)

- 4.7.3 Bargaining Power of Buyers (Shippers)

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Service

- 5.1.1 Full-Truckload (FTL)

- 5.1.2 Less-than-Truckload (LTL)

- 5.1.3 Others

- 5.2 By Equipment / Trailer Type

- 5.2.1 Dry Van

- 5.2.2 Refrigerated Van

- 5.2.3 Flatbed / Step-Deck

- 5.2.4 Tanker (Bulk Liquid and Chemical)

- 5.2.5 Others

- 5.3 By Haul Length

- 5.3.1 Long-Haul (More than 500 miles)

- 5.3.2 Regional (100-500 miles)

- 5.3.3 Local (Less than 100 miles)

- 5.4 By Business Model

- 5.4.1 Traditional Freight Brokerage

- 5.4.2 Asset-Based Freight Brokerage

- 5.4.3 Agent Model Freight Brokerage

- 5.4.4 Digital Freight Brokerage

- 5.5 By End-User Industry

- 5.5.1 Manufacturing and Automotive

- 5.5.2 Construction and Infrastructure Projects

- 5.5.3 Oil, Gas, Mining and Chemicals

- 5.5.4 Agriculture and Food / Beverage

- 5.5.5 Retail, FMCG and Wholesale Distribution

- 5.5.6 Healthcare and Pharmaceuticals

- 5.5.7 E-commerce and 3PL Fulfilment

- 5.5.8 Other End-User Industry

- 5.6 By Customer Size

- 5.6.1 Large Enterprise Shippers (More than USD 100 M)

- 5.6.2 Mid-Market Shippers (USD 10-100 M)

- 5.6.3 Small Businesses (Less than USD 10 M)

- 5.7 By Geography

- 5.7.1 United States

- 5.7.2 Canada

- 5.7.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves and M&A

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 C.H. Robinson Worldwide

- 6.4.2 Total Quality Logistics (TQL)

- 6.4.3 Echo Global Logistics, Inc.

- 6.4.4 RXO

- 6.4.5 J.B. Hunt Transport Services, Inc.

- 6.4.6 Hub Group, Inc.

- 6.4.7 Landstar System

- 6.4.8 Schneider Logistics

- 6.4.9 WWEX Group

- 6.4.10 Arrive Logistics

- 6.4.11 Mode Transportation

- 6.4.12 BlueGrace Logistics

- 6.4.13 Nolan Transportation Group

- 6.4.14 Sunset Transportation

- 6.4.15 Werner Enterprises

- 6.4.16 Trinity Logistics

- 6.4.17 Ascent Global Logistics

- 6.4.18 Integrity Express Logistics

- 6.4.19 Redwood Logistics

- 6.4.20 PLS Logistics Services

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment