PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063307

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063307

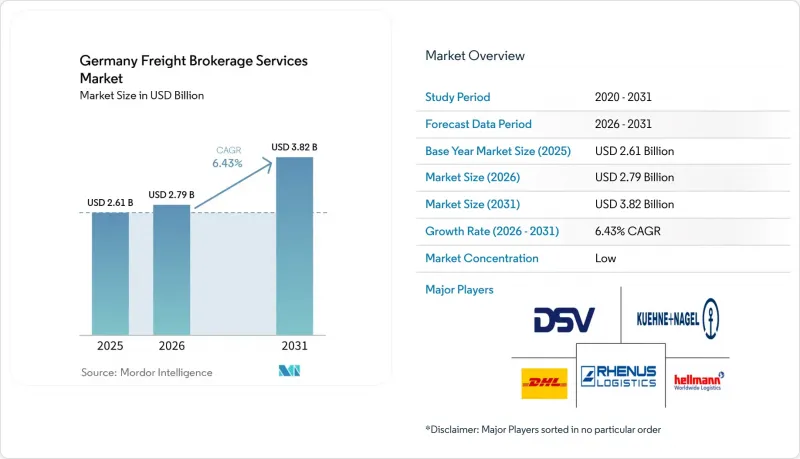

Germany Freight Brokerage Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the germany freight brokerage services market size is projected to be USD 2.61 billion in 2025, USD 2.79 billion in 2026, and reach USD 3.82 billion by 2031, growing at a CAGR of 6.43% from 2026 to 2031.

Demand expands because manufacturers diversify Eurasian trade routes, shippers chase real-time load visibility, and federal policy keeps toll exemptions for zero-emission trucks. This report is Segmented by Service (Full-Truckload, and More), Equipment/Trailer Type (Dry Van, Refrigerated Van, and More), Haul Length (Long-Haul, Regional, and Local), Business Model (Traditional, Asset-Based, and More), End-User Industry (Manufacturing & Automotive, and More), Customer Size (Large Enterprise, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Freight Brokerage Services Market Trends and Insights

Post-Red-Sea Diversion boosting Eurasian Rail-to-Road Trans-loading through Germany

Persistent piracy risk has pushed Asia-Europe ocean cargo toward Eurasian rail, lifting China-EU rail volume to 380,434 TEU in 2024, an 80.2% jump year on year. Duisburg and Hamburg act as gateways where inland terminals shift containers to trucks for final delivery, creating high-margin, time-sensitive loads for brokers. Empty-box repositioning also grows as westbound rail leaves fewer empties in Germany, compelling brokers to organize backhauls to North Sea ports. Unless Red Sea routes normalize, brokers can rely on this rail-driven uplift through at least 2027, embedding new revenue channels in Germany freight brokerage services market operations.

Electrified-Truck Subsidy Wave Unlocking New Capacity Corridors

Germany has allocated USD 1.74 billion for 1,410 high-power chargers along major autobahns, a move that lowers per-kilometer energy cost by 40% for battery trucks and widens lane options for brokers. Toll exemptions for zero-emission heavy vehicles now run to mid-2031, shrinking the total cost of ownership and encouraging mid-sized carriers to replace diesel tractors sooner. Brokers that ingest telematics data from electric fleets can reroute around scarce chargers, cut dwell time, and advertise low-carbon capacity to shippers seeking greener loads. Charging clusters on A3, A5, and A7 already shift volume from diesel lanes. The program therefore delivers both cost savings and new selling points that propel Germany freight brokerage services market growth.

EU Mobility Package IV Wage-Parity Audits Inflating Compliance Overhead

From January 2026, Germany will enforce a USD 15.1 hourly wage floor for posted drivers, erasing the historical 25% rate edge held by Eastern European carriers. Brokers now spend extra hours auditing payroll files and tachograph logs, or risk stiff penalties. Smart Tachograph 2 rules, hitting light vans in July 2026, widen the audit scope. Some small brokers are exiting cross-border lanes rather than funding compliance tools, which tightens capacity and raises spot prices but also crimps broker margins.

Other drivers and restraints analyzed in the detailed report include:

- AI-Based Dynamic Lane-Pricing Demanded by Top 500 German Shippers

- Corporate Scope-3 Emissions Audits Creating Premium for Tracked Loads

- Cyber-Attacks on Freight-Exchange APIs Increasing Insurance Premiums

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Full-truckload commanded 73.22% of Germany freight brokerage services market share in 2025, as automotive just-in-sequence shipments and bulk chemicals relied on dedicated trailers. Contract lanes give shippers predictable rates, and brokers earn steady margins from repeat volume. Network depth along A4, A6, and A9 supports same-day north-south runs, a critical feature for tier-one suppliers.

Less-than-truckload solutions are projected to grow at an 8.09% CAGR to 2031, supported by e-commerce parcel consolidation and small-batch industrial orders. IDS Logistik's tie-up with Spedition Kleine brings 800 daily deliveries into its Grevenbroich hub, a case that proves how dock-scheduling APIs can cut yard dwell by 70%. Brokers aggregating 2-10-pallet loads now leverage AI to optimize cube and reduce empty miles, lifting yield and enhancing the Germany freight brokerage services market size for LTL operators.

Dry-van trailers held 38.41% of equipment revenue in 2025 because they move consumer goods, packaged foods, and industrial parts with minimal special handling. Their ubiquity ensures the widest carrier pool, which keeps spot quotes competitive.

Refrigerated vans are forecast to expand at an 8.67% CAGR, fueled by cold-chain audits for vaccines and the spread of online grocery. Seasonal fruit runs from Spain and Italy boost Germany-bound reefer spot rates to double dry-van levels during winter peaks. Brokers that pre-book electric reefer units at grid-connected parking bays enjoy lower diesel surcharges and gain loyalty from carbon-conscious food retailers, increasing the size of the German freight brokerage services market captured in the temperature-controlled niche.

List of Companies Covered in this Report:

- DSV A/S (including DB Schenker)

- DHL Group

- Kuehne+Nagel

- Rhenus Logistics

- Hellmann Worldwide Logistics

- Dachser

- Sennder

- Transporeon

- C.H. Robinson

- Yusen Logistics (Part of NYK Line)

- GEODIS

- Rohlig Logistics

- Emo Trans

- Trucksters

- Fiege Logistics

- Cargoline

- System Alliance Europe

- Carmovia

- Ontruck

- SLYNX

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrified-Truck Subsidy Wave Unlocking New Capacity Corridors

- 4.2.2 AI-Based Dynamic Lane-Pricing Demanded by Top 500 German Shippers

- 4.2.3 Post-Red-Sea Diversion Boosting Eurasian Rail-to-Road Trans-loading through Germany

- 4.2.4 Corporate Scope-3 Emissions Audits Creating Premium for Tracked Loads

- 4.2.5 Shift from FOB to DDP Terms in Mittelstand Exports Raising Brokerage Need for Door-To-Door Control

- 4.2.6 Federal "ETA Transparency Mandate" Accelerating API Adoption

- 4.3 Market Restraints

- 4.3.1 EU Mobility Package IV Wage-Parity Audits Inflating Compliance Overhead

- 4.3.2 Cyber-Attacks on Freight-Exchange APIs Increasing Insurance Premiums

- 4.3.3 Logistic-Hub Zoning Freeze in Nordrhein-Westfalen Limiting Cross-Dock Expansion

- 4.3.4 Volatile OEM Production Cycles (EV and Semiconductor Swings) Driving Demand Unpredictability

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Service

- 5.1.1 Full-Truckload (FTL)

- 5.1.2 Less-than-Truckload (LTL)

- 5.1.3 Others

- 5.2 By Equipment / Trailer Type

- 5.2.1 Dry Van

- 5.2.2 Refrigerated Van

- 5.2.3 Flatbed / Step-Deck

- 5.2.4 Tanker (Bulk Liquid & Chemical)

- 5.2.5 Others

- 5.3 By Haul Length

- 5.3.1 Long-Haul (More than 500 miles)

- 5.3.2 Regional (100-500 miles)

- 5.3.3 Local (Less than 100 miles)

- 5.4 By Business Model

- 5.4.1 Traditional Freight Brokerage

- 5.4.2 Asset-Based Freight Brokerage

- 5.4.3 Agent Model Freight Brokerage

- 5.4.4 Digital Freight Brokerage

- 5.5 By End-User Industry

- 5.5.1 Manufacturing & Automotive

- 5.5.2 Construction & Infrastructure Projects

- 5.5.3 Oil, Gas, Mining & Chemicals

- 5.5.4 Agriculture & Food / Beverage

- 5.5.5 Retail, FMCG & Wholesale Distribution

- 5.5.6 Healthcare & Pharmaceuticals

- 5.5.7 E-commerce & 3PL Fulfilment

- 5.5.8 Other End-User Industry

- 5.6 By Customer Size

- 5.6.1 Large Enterprise Shippers (More than USD 100 M)

- 5.6.2 Mid-Market Shippers (USD 10-100 M)

- 5.6.3 Small Businesses (Less than USD 10 M)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DSV A/S (including DB Schenker)

- 6.4.2 DHL Group

- 6.4.3 Kuehne+Nagel

- 6.4.4 Rhenus Logistics

- 6.4.5 Hellmann Worldwide Logistics

- 6.4.6 Dachser

- 6.4.7 Sennder

- 6.4.8 Transporeon

- 6.4.9 C.H. Robinson

- 6.4.10 Yusen Logistics (Part of NYK Line)

- 6.4.11 GEODIS

- 6.4.12 Rohlig Logistics

- 6.4.13 Emo Trans

- 6.4.14 Trucksters

- 6.4.15 Fiege Logistics

- 6.4.16 Cargoline

- 6.4.17 System Alliance Europe

- 6.4.18 Carmovia

- 6.4.19 Ontruck

- 6.4.20 SLYNX

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment